Book Review: Rise and Fall of the Great Powers

post by dmanningcoe (TheRealSlimHippo) · 2021-10-13T16:22:11.838Z · LW · GW · 3 commentsContents

Introduction Domestic stability vs. investment Military vs. investment Domestic stability vs. Military spending The Prussian counterexample Application to contemporary economies China, India, Japan US Conclusion None 3 comments

Introduction

Paul Kennedy's 1986 masterpiece "Rise and Fall of the Great Powers" (I'll abbreviate as RF) is, first, a dataset. It is the most comprehensive compendium of case studies from 1500-1980 available to the casual reader (that I have come across) of the fate of nations over 50-100 year periods. Second, although he never explicitly states it, I read Kennedy's book as one of the best expositions of the view that a nations internal economic and political arrangements are the most important thing to get right.

There are three ways to read the book. They become more interesting as they become more epistemically risky. The first is simply the thesis that - "productive balances determine the outcome of [conventional] military conflicts". With a few notable exceptions Kennedy makes a powerful case for this. The virtue of RF is it compiles difficult to find data that make this point powerfully. Even this weak conclusion is not trivial. Although most people prima facie accept this claim, often they don't carry it through to the logical conclusion that economic backwardness eventually imperils a nations existence - a point that is essential to understand Stalin's Soviet Union. The second is to view it as a bunch of data which we can use to test theories that attempt "grand history" - (i.e Zeihan in Disunited Nations or Acemoglu and Robinson in Why Nations Fail). The most interesting (and most risky) way to interpret the book is as a framework think about whether a nation (great or not) succeeds or fails. I'll review RF mostly under this reading.

Towards the end, Kennedy finally states this view explicitly:

"since the varied demands of defense spending/military security, social/consumer needs, and investment for growth involve a triangular competition for resources, there is no absolutely perfect solution to this tension."

Let me make this slightly more explicit as the claim that if we want to know about a nation's future we should analyze the trade-offs between:

- Military superiority to competitor nations in the present,

- Making sacrifices in the present for economic growth in the future (i.e investment),

- Maintaining stability at home.

An appropriate reaction at this point is "Whoever would have thought otherwise? Who would have thought that investment was not important for a nations future?". The content of this framework is first that there are tradeoffs between these objectives and second, that analyzing these trade-offs gives you insight into how a nation will evolve (as opposed to say focusing on a nations geography as in Disunited Nations).

This is probably best illustrated with an example. There are basically two types of ideas on what determines a nations long term future:

- The geographic thesis: Success is primarily determined by how suited a nations geography is to the technology of the time (i.e having oil deposits is useless before 1850).

- The internal thesis: Success is primarily determined by whether a nation has the right internal structure -(i.e institutions, culture, governance, trust etc...).

These lead to vastly different grand strategies. It follows from the first that, insofar as it's able, a nation's first priority should be to seize the geographical regions that will unlock its potential. It follows from the second that the requisite blood and treasure to acquire territory are (usually) much better kept at home. On the second view, it seems nonsensical that, say, China would want to annex Taiwan. Why spend the money building a strong enough military to take or intimidate the island, when you could use it to invest in AI in Shenzhen? On the first view however, this would protect the flow of resources China needs to continue to develop - the economic growth will then take care of itself.

The framework in RF suggests that the right answer to whether this helps or hinders Russia will depend on the extent to which the resource cost (diplomatic, military and political) will impact the other two components. We can then see the geographic and internal theses as special cases: the geographic thesis sees the last two objectives as largely fixed, whilst the internal thesis sees them as largely movable. Kennedy's framework would be falsified if these components were not in conflict (if military buildup accelerates economic growth, say - as is sometimes claimed for US investment in R&D in the 1960s), or if different factors need to be considered.

There are too many historical cases to give an overview of them in a reasonable length of time - for that, you'll have to read it! I'll review RF by going through what I consider to be the most illustrative historical example of each type of conflict that arise between the objectives, then point out what this framework struggles to explain, and finally speculate (wildly) by applying it some contemporary economies.

Domestic stability vs. investment

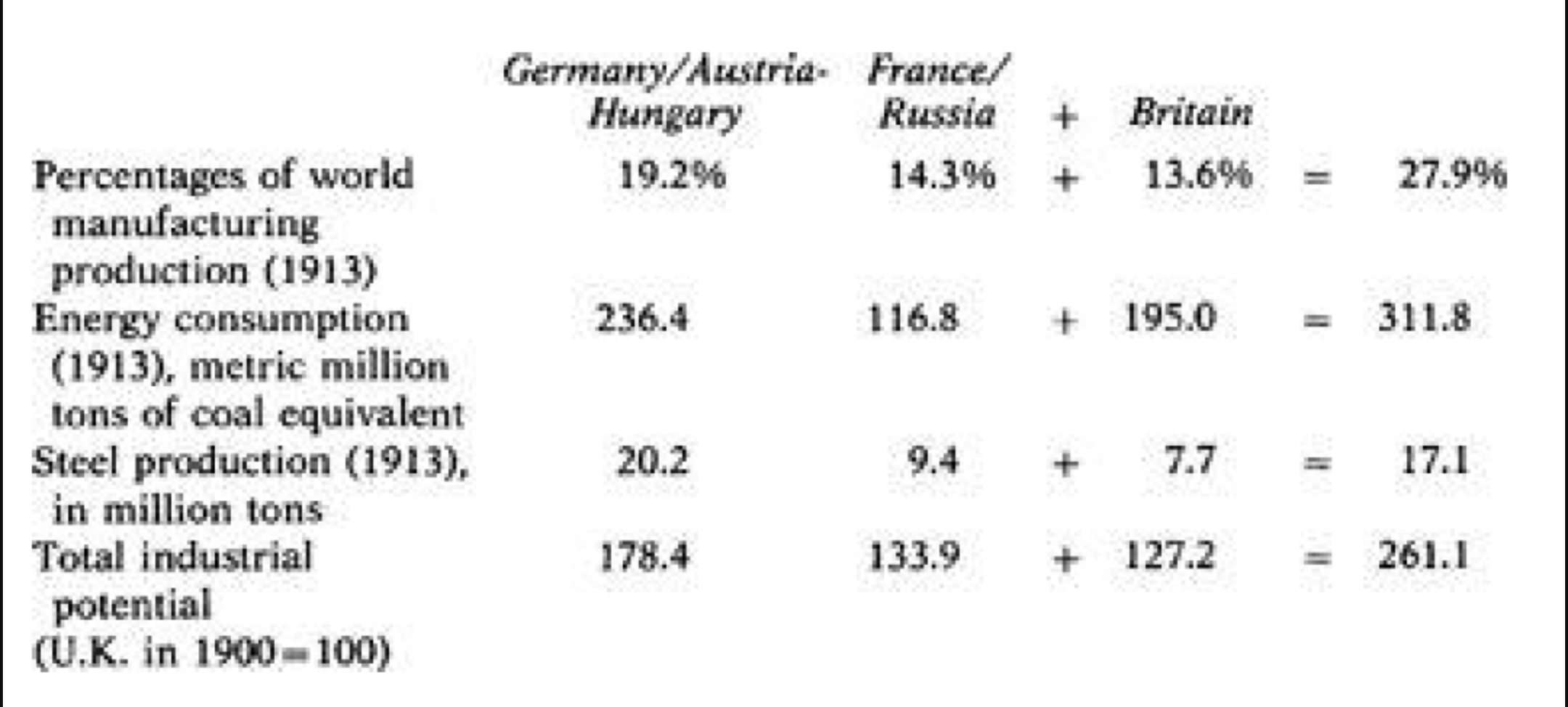

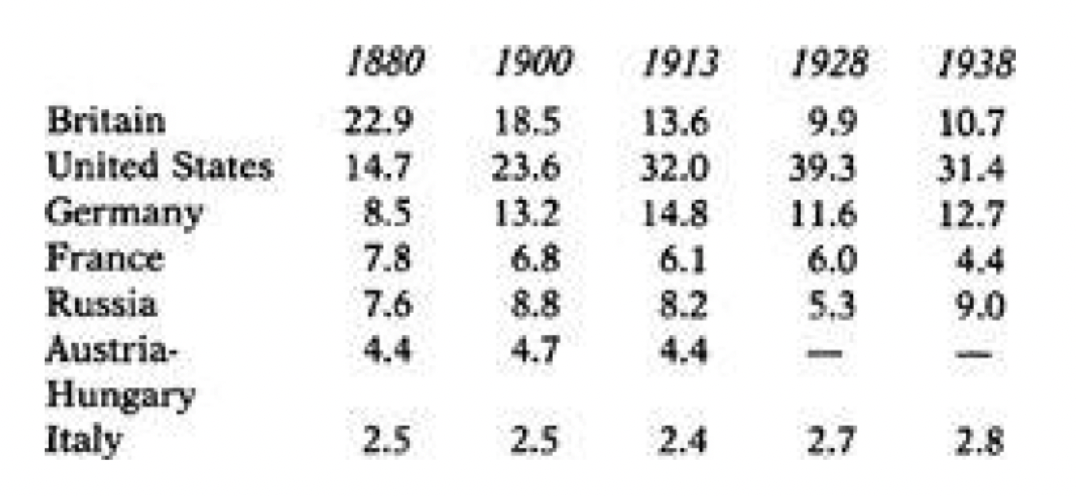

Stalin's Soviet Union in the interwar period 1929-1941 is the paradigm of sacrificing domestic stability in order to force economic growth. To properly understand the context of this trade-off we first have to appreciate the weakest form of Kennedy's thesis - that "Productive balances determine outcome of [conventional] military conflicts". To see this, let us look at the total manufacturing GDP (the part of GDP relevant for producing weapons) for each side in WW1:

Source: KENNEDY, P. M. (1987). The rise and fall of the great powers: economic change and military conflict from 1500 to 2000.

Since the manufacturing GDPs are roughly equal we would expect a stalemate with a slight advantage for the Entente - which indeed is precisely what happened. Once the USA joins the allies the story is completely different - and indeed once US soldiers had landed in meaningful numbers in 1918, the war came to a quick conclusion.

Source: KENNEDY, P. M. (1987). The rise and fall of the great powers: economic change and military conflict from 1500 to 2000.

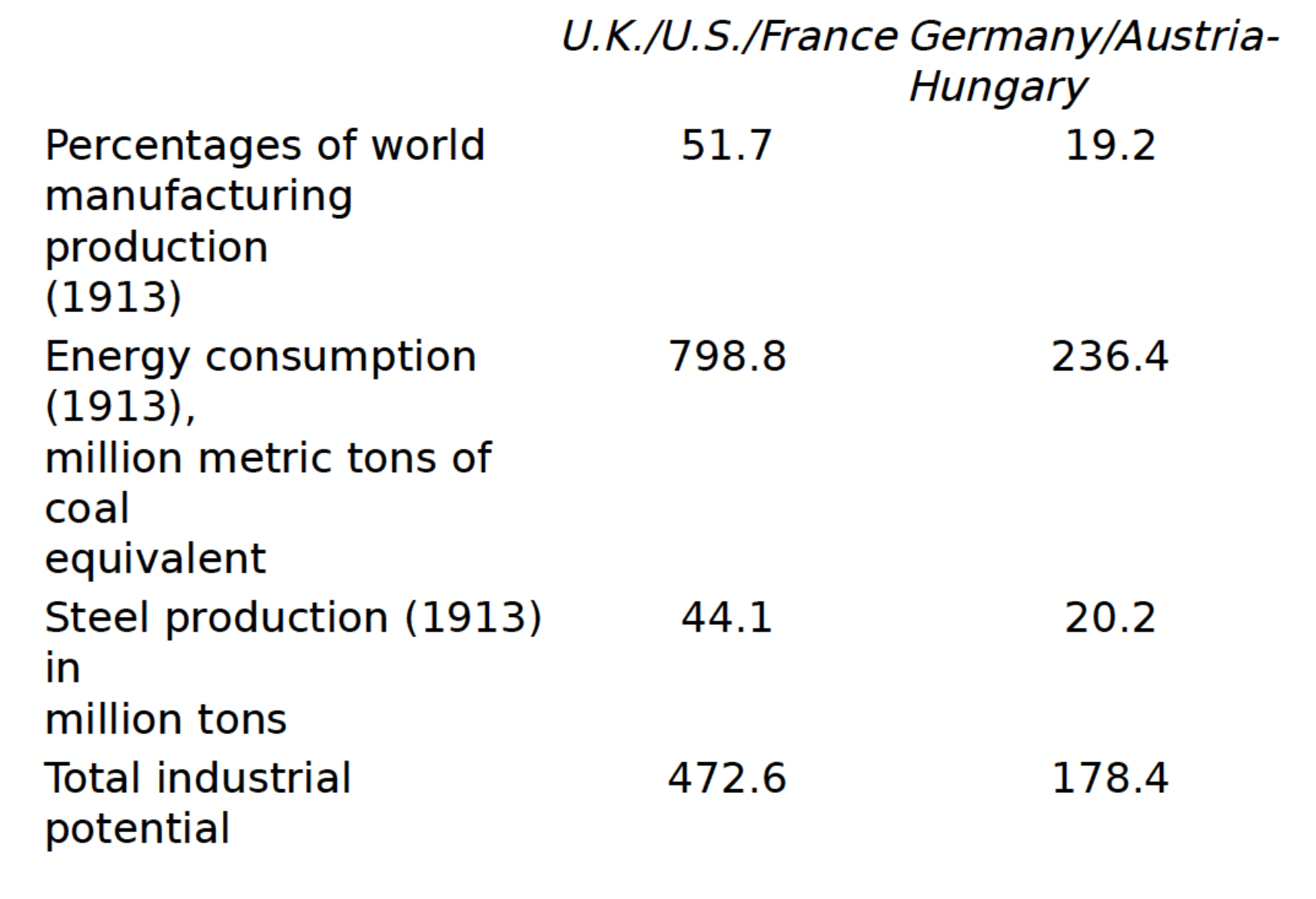

Kennedy marshal's similar data for the Crimean War. Once Britain and France had an overwhelming advantage in the "productive balances" against Russia, they translated this into military gains in the Crimean War for 1853.

Source: KENNEDY, P. M. (1987). The rise and fall of the great powers: economic change and military conflict from 1500 to 2000.

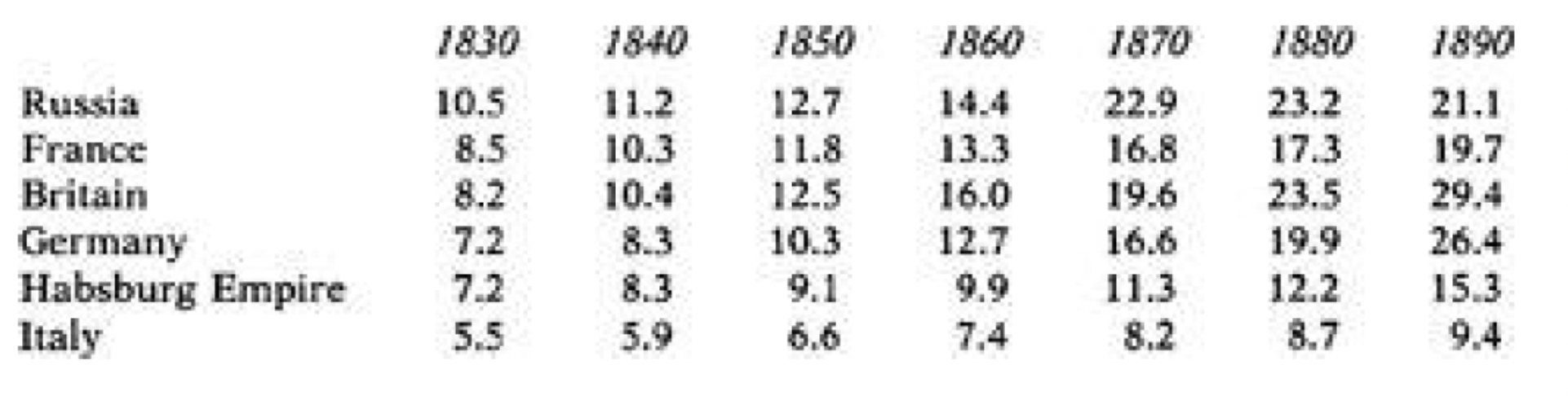

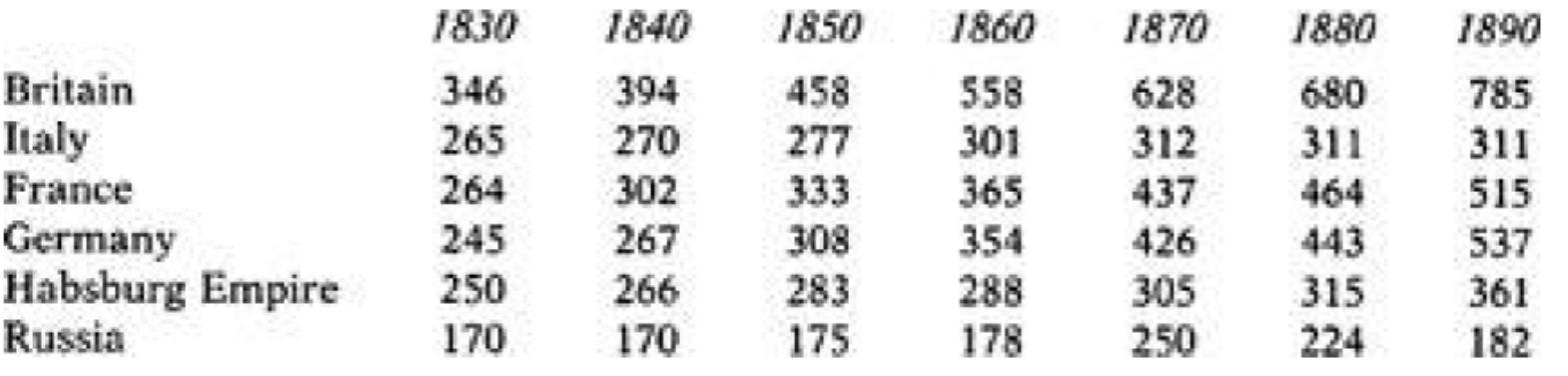

The period between the world wars then, was a hazardous time for a nation. The 1800s had confirmed that the western powers were merciless in using their economic advantage to impose brutal colonial regimes where they could. Since wars between the European powers were restrained by their high stakes, the European powers looked to make military gains against less developed nations. But what nations were left? The first world war and then the revolution had left Russia devastated. The resulting "productive balances" for the 1927 Soviet Union were grim:

| 1913 | 1920 | 1921 | 1922 | 1923 | 1924 | 1925 | 1926 | 1927 | |

| USSR | 4% | 1% | 1% | 1% | 1% | 2% | 2% | 3% | 4% |

| Germany | 15% | 9% | 13% | 12% | 8% | 11% | 11% | 10% | 13% |

| U.K. | 14% | 14% | 10% | 11% | 11% | 11% | 10% | 9% | 10% |

| France | 6% | 5% | 5% | 6% | 6% | 7% | 6% | 7% | 6% |

| Japan | 1% | 2% | 2% | 2% | 2% | 2% | 2% | 2% | 2% |

| US | 40% | 53% | 49% | 51% | 54% | 48% | 49% | 50% | 46% |

Stalin saw the danger: "We are fifty or a hundred years behind the advanced countries. We must make up this gap in ten years. Either we do it or they will crush us.". Hitler concluded that Russia would become "Germany's India" after a "war of annihilation". Economic development was no longer about being marginally ahead but now about survival at all. The stakes could not have been higher. It follows that of the three competing objectives, in Stalin's view, the only two available, were military power and economic development. The sacrifices for future economic growth would have to come at the cost of living standards. Since the Soviet union was at that point largely a subsistence economy, this would mean driving the population to the brink of starvation in order to fund the factories. This brutal story is told in the statistics by the increase in investment at the expense of consumption following the introduction of the 1929 five year plan:

Source: Was Stalin Necessary for Russia's Economic Development?, Cheremukhin, Anton and Golosov, Mikhail and Guriev, Sergei and Tsyvinski, Aleh (2013)

No population could have been expected to suffer such privations without serious discontent. To maintain domestic stability and insure uninterrupted reallocation of resources into heavy industry Stalin created one of the most brutal regimes in history. The median historian estimate is that two million civilians were murdered. The Soviet Union became the first major power in history to achieve breakneck growth of around 10% a year (from an artificially low base), with even more impressive increases in manufacturing:

| 1927 | 1928 | 1929 | 1930 | 1931 | 1932 | 1933 | 1934 | 1935 | 1936 | 1937 | 1938 | |

| USSR | 4% | 4% | 5% | 7% | 10% | 13% | 13% | 14% | 15% | 16% | 17% | 20% |

| Germany | 13% | 12% | 11% | 11% | 10% | 9% | 9% | 11% | 11% | 10% | 10% | 12% |

| U.K. | 10% | 9% | 10% | 10% | 11% | 10% | 11% | 10% | 10% | 9% | 9% | 0% |

| France | 6% | 7% | 7% | 8% | 8% | 9% | 9% | 8% | 7% | 6% | 6% | 7% |

| Japan | 2% | 3% | 3% | 3% | 3% | 3% | 4% | 4% | 4% | 3% | 3% | 4% |

| US | 46% | 46% | 47% | 43% | 40% | 35% | 37% | 36% | 37% | 39% | 38% | 31% |

Just as in WW1, the slight industrial advantage enjoyed by the allies gave them a slight military advantage. Thus, when France was fighting alone in 1940, it was quickly defeated. The Soviet Union came within a hair of annihilation in 1941, but was able to turn the tide, largely alone, by 1943. The fate of the axes was sealed once the US entered the war in a meaningful way in 1944. As Churchill proclaimed "the rest is just the application of overwhelming force".

It is hard to overstate the example of the Soviet Union Five Year Plan's had on the developing world. As the world order was reshaped after WW2, newly independent countries saw the Soviet Union economic model as the only one that had developed the means to resist the former colonial powers. Moreover, it had done so against the backdrop of the most severe financial crisis of the 20th century. Brutal thought the cost had been (and the full cost was not then widely known) the Soviet Union had succeeded in achieving rapid growth and thereby providing the material means to resist colonization. Many countries planning their economic system ex nihilo thus concluded that to ensure their survival they too would have to suffer the same privations the Soviet's had. Hence India's Nehru, China's Mao, and Egypt's Nasser would all institute central planning for their economies.

Even Paul Samuelson, one of the founding fathers of modern economics, was taken in. In his 1960 textbook he predicted that the Soviet Union would overtake the USA by 1980. The reason was simple - as an extractive totalitarian regime, the Soviet Union could make larger short term sacrifices (i.e drive consumption lower) for long term benefits (to support a higher investment rate). Eventually therefore, the Soviet's would become dominant.

Stalin's gambit, however, had a sting in the tail. To understand this, let's introduce a useful tautology: define the "rate of return" as:

This is a very crude way of quantifying the "quality" of investment - a higher value means that each unit of investment produces a larger increase in economic output. We can imagine the "rate of return" as capturing the ability of an economy to develop new technologies, convert them into more efficient production, quality of administration, waste etc... . The regime Stalin had created was efficient at increasing the amount of investment, but once the low hanging fruit was gone the rate of return collapsed:

This occurred for all the well documented problems with central planning that were exposed in the soviet union post 1960's: excessive bureaucracy, tremendous waste (Kennedy repeats the well known but nonetheless striking statistic that 4% of agricultural land in the soviet union was private yet produced 25% of output), low rates of innovation etc... . The USSR was thus in a bind - it had forced investment at the price of creating a brutal internal security regime to preserve domestic stability. As the rate of return collapsed post 1960, the soviet union increasingly had to hope that it could use it's point in time military superiority to translate into economic gain. The cold war thus saw its final flash points in the 1980's, before Gorbachev gambled unsuccessfully on resolving the core imbalance: "Acceleration of the country’s socio-economic development is the key to all our problems; immediate and long-term, economic and social, political and ideological, internal and external."

Source: Calculated from Joint Committee Report on Soviet economic growth 1980 and 1990

Before commenting briefly on the next trade-off, it's worth pausing to see whether first, others scholar agree that the soviet industrialization had to come at the expense of domestic consumption, and second if we can find other examples of this trade-off. I think the most we can conclude is that this question is criminally understudied. This strikes me as the central question for coming up with an assessment of Stalin's policies and yet after 1800 pages of Stephen Kotkin's authoritative biography, all we get is a reference to a 2013 paper that illustrates a growth decomposition method. It claims that Stalin's policies were unnecessary by simulating a 'Japan style' path for the Soviet Union in 1929 (Beyond the scope of this review but I don't find their analysis conclusive - the problem is that the external environment's were entirely different. To substantiate this requires at least a slightly detailed discussion of the diplomatic options available to the USSR.) What I think is at least clear is that Kennedy's framework gets us the right qualitative answer - growth was boosted at the expense of consumption.

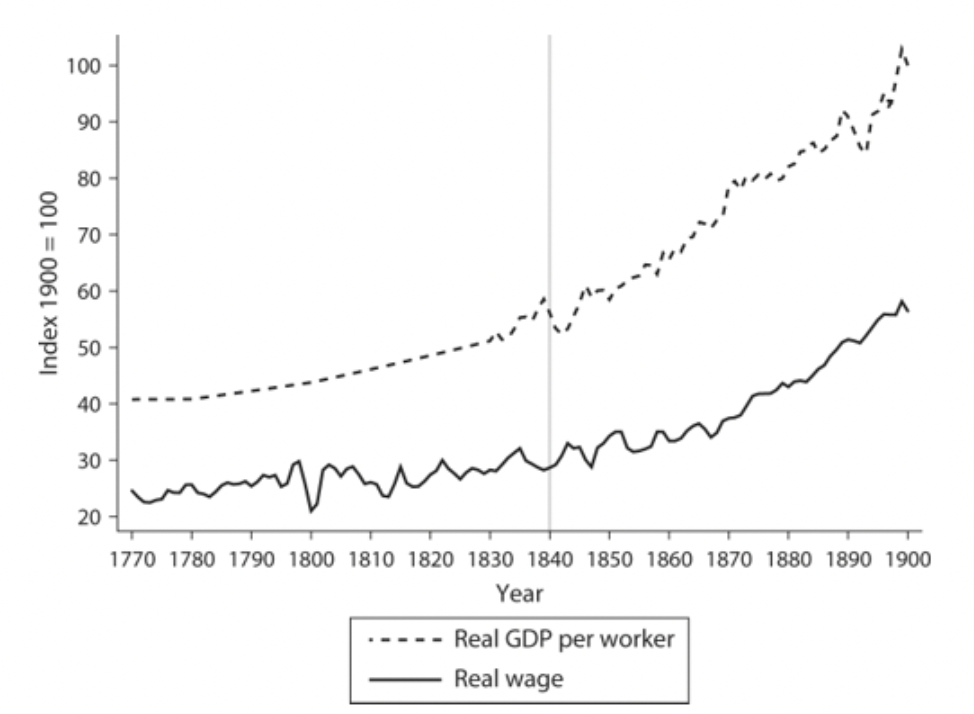

On the second, the most illustrative example is the initial industrialization phase for the western European economies. They, too, went through a similar pattern of driving down living standards to fund the investment necessary for the industrial revolution (which featured prominently in the Soviet's thinking about the right economic model). Carl Frey recounts this "Engels pause" phenomenon excellently in The Technology Trap:

Source: FREY, C. B. (2019). The technology trap: capital, labor, and power in the age of automation

Even though the real wage rate is stagnant, hours worked increased and nutrition suffered causing life expectancy to be ten years lower in industrial regions than the rest of the country.

(Aside: looking at industrializing nations (say in Devine's History of Scotland) in detail one often finds accounts of workers eagerly moving to the cities despite being aware of the lower life expectancy and harder working conditions, so its not entirely convincing that industrial life was worse until 1870.)

Military vs. investment

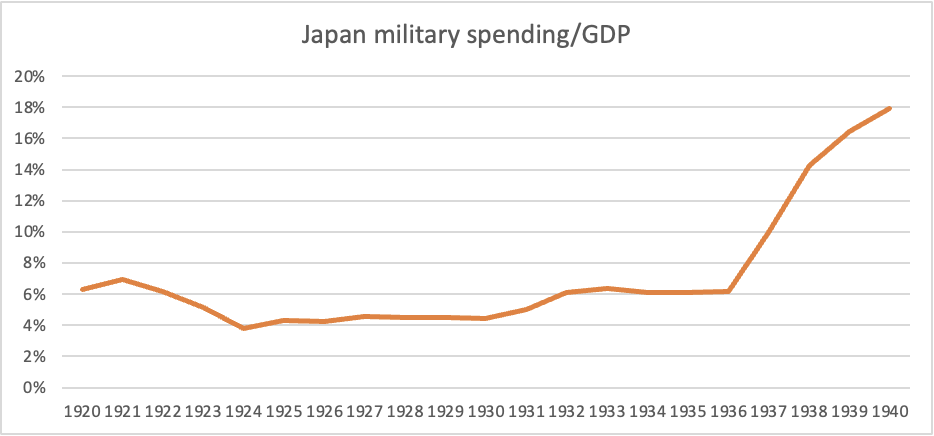

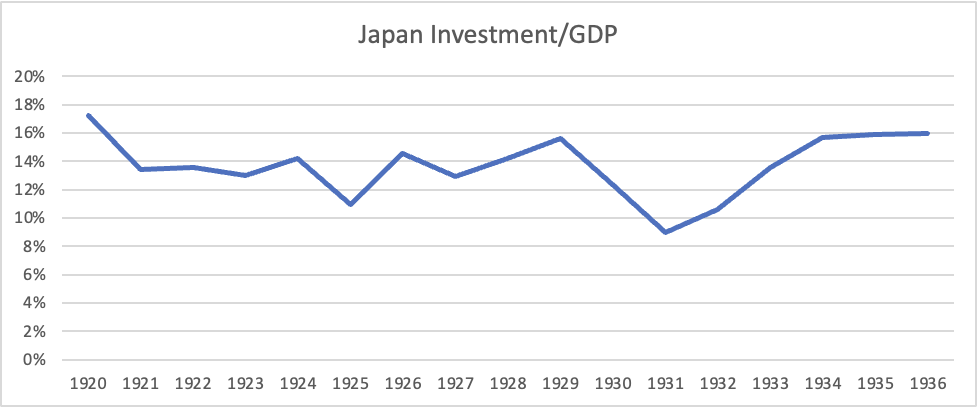

The contrast between pre- and post-WW2 Japan is the clearest example of the conflict between investing in economic growth and spending on the military.

Between 1914 and 1938, Japan favored military expansion at the expense of economic growth. Japan devoted around 5% of its GDP to the military (about twice the rate of the UK) leaving only 15% for investment:

Source: Calculated from Interwar U.S. and Japanese National Product and Defense Expenditure, William D. O'Neil (2003)

Source: Calculated from Interwar U.S. and Japanese National Product and Defense Expenditure, William D. O'Neil (2003) and

Long-term Movement of Capital Formation - The Japanese Case, Koichi Emi

Worse, the rate of return was terrible since the best talent went to the military. The result was that Japanese GDP per capita barely moved - from $920 in today's dollars in 1913 to $960 in 1938.

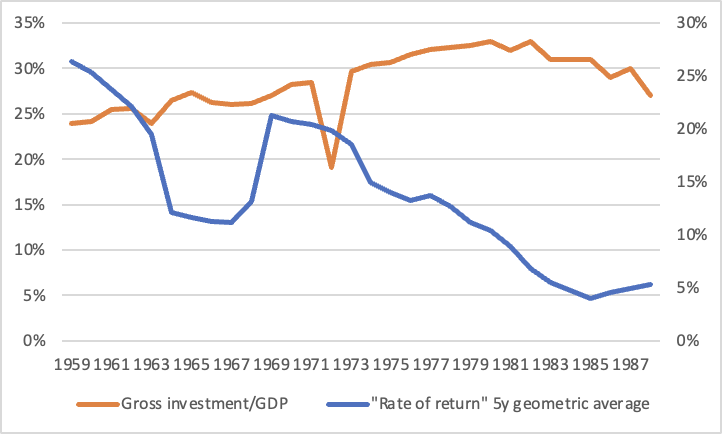

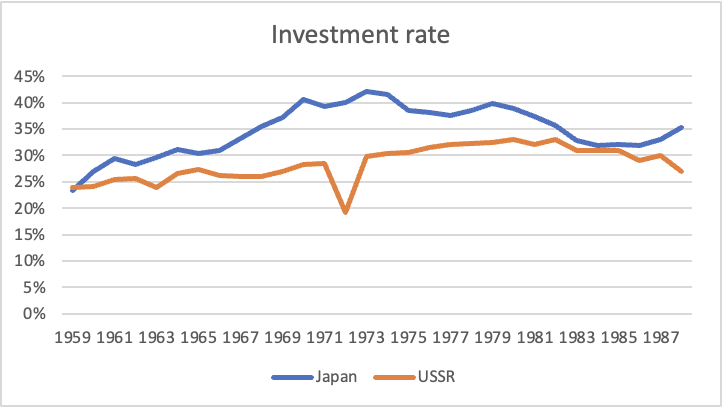

Between the Americans leaving in 1950 and 1973 Japanese GDP per capita exploded - from $3000 to $18000. From the perspective of the economic statistics, the proximate explanation is simply this - freed from the requirement to spend 6-10% of GDP on its military, Japan could devote this resource to investment. When combined with a population willing to save large portions of their income to fund the country's development, this set of a virtuous cycle of investment growing incomes which in turn increased the capital available for further growth.

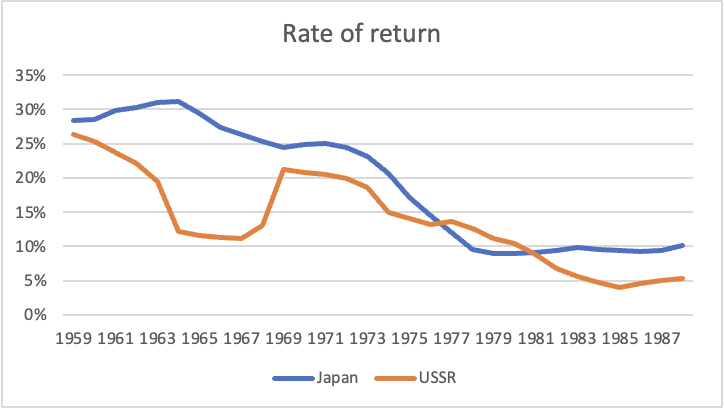

Growing income also reduced the fertility rate (more on this in the penultimate section). Since children are the largest expense of a household this supercharged the growth in savings available for investment. This allowed Japan to have an investment rate higher even than the Soviet Union - totalitarianism is no match for demography! The real magic, though, lay in the rate of return. Japan managed to sustain a much higher rate of return than the Soviets, and intriguingly, the rate of returned increased with increasing investment up to 165:

Source: Calculated from Joint Committee Report 1986 and 1990 and World Bank

Source: Calculated from Joint Committee Report 1986 and 1990 and World Bank

Kennedy's framework analyzes this as Japan having sacrificed military spending and domestic consumption to concentrate on future economic growth via investment. Kennedy points out that this was only possible because of Japan's unique circumstances: "sheltering under the US military umbrella" removed the usual penalty for falling behind competitor nations militarily, and an unusually high level of social cohesion post WW2 meant the population were willing (once properly incentivized through tax policy) to defer large portions of current consumption. The lesson is simple: if a nation can avoid being penalized by competitors for having a weak military, has the right demographics, and a population willing to sacrifice current consumption - then spectacular economic growth can be achieved, laying the foundations for long term success. In terms of the framework, we can trade-off objectives 1 and 3 with 2.

Domestic stability vs. Military spending

Surprisingly, I found it difficult to cleanly categorize any of the cases reviewed as this conflict. The cleanest candidate is probably the French revolution. The American war of Independence initiated yet-another war between England and France that would exhaust the French treasury. Kennedy doesn't go into detail here and merely nods in this direction: "the sheer cost of the 1778-1783 war... interacted with the growing political discontents, economic distress, and social malaise to discredit the ancien regime." The decline of the Ottoman Empire, too, is a good candidate to be analysed this way since it may have been excessive spending on the military that thwarted on Ottoman industrial revolution. Finally we have the decline of Russia's relative economic power after 1815, but that is probably better considered as a conflict between military spending and investment.

The Prussian counterexample

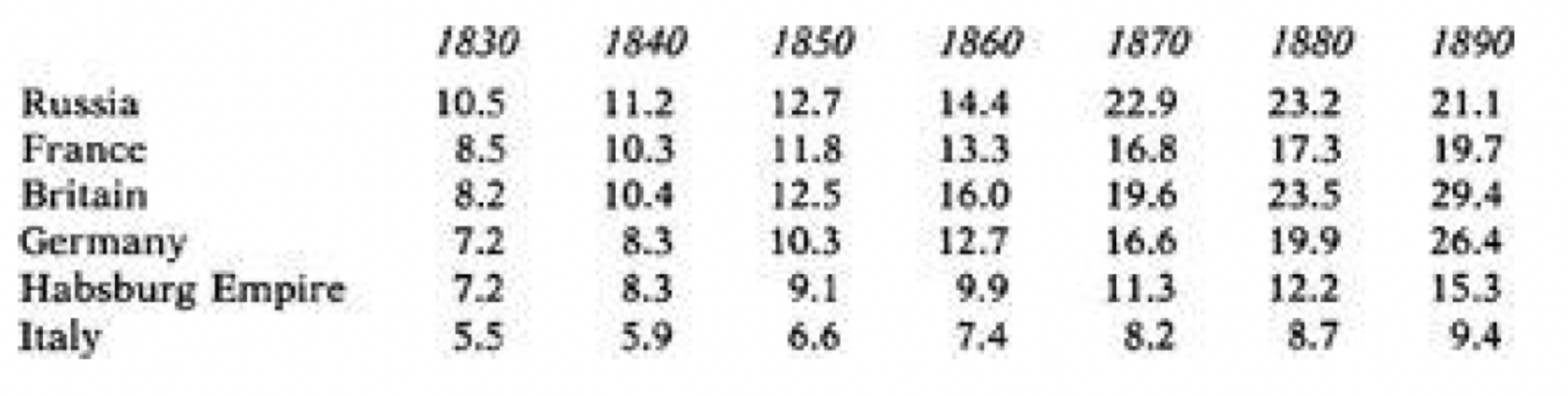

The most striking counterexample in Kennedy's work is 1700-1871 Prussia. Prussia appears to be the archetype of a power that succeeds in securing economic growth through military spending. At the start of Kennedy's period, Prussia is just one princedom amongst the three hundred or so German states. Through marriage and judicious military intervention, Prussia would grow into a moderate power by 1700. But it was significantly poorer than Britain or France, and had no easily defensible borders:

Source: CLARK, C. M. (2006). Iron kingdom: the rise and downfall of Prussia, 1600-1947. Cambridge, Mass, Belknap Press of Harvard University Press.

Source: CLARK, C. M. (2006). Iron kingdom: the rise and downfall of Prussia, 1600-1947. Cambridge, Mass, Belknap Press of Harvard University Press.

Prussia's remarkable ascent during the next 170 years was built on its military. Voltaire famously quipped that " “Where some states possess an army, the Prussian Army possesses a state.” 80% of the government budget (and since the economy was largely subsistence this was most of the surplus) went on the army, the largest of any of the major European powers.

Source: What to do states do? Politics and economic history, Philip Hoffman, Journal of economic history

In 1860-71, Prussia translated the military advantage into economic gains, winning a war against Austria and then decisively against France to unify Germany. This, at least initially, fits badly with the weak form of Kennedy's thesis. The same type of analysis of the "productive balances" as in WW1 would suggest a stalemate in the war with France:

Source: KENNEDY, P. M. (1987). The rise and fall of the great powers: economic change and military conflict from 1500 to 2000.

Source: KENNEDY, P. M. (1987). The rise and fall of the great powers: economic change and military conflict from 1500 to 2000.

Kennedy suggests that this is the exception that proves the rule, since a more detailed look into the numbers would show that Prussia had more production where it mattered: "Germany had more miles of railway lines, better arranged for military purposes. Its gross national product and its iron and steel production were just then overtaking the French totals. Its coal production was two and a half times as great, and its consumption from modern energy sources was 50 percent larger". I think without further work this explanation of the 1700-1871 story is unconvincing (given that the per capita and total manufacturing levels were roughly equal) and so Prussia during this time should be considered a counterexample even to the weakest form of Kennedy's thesis.

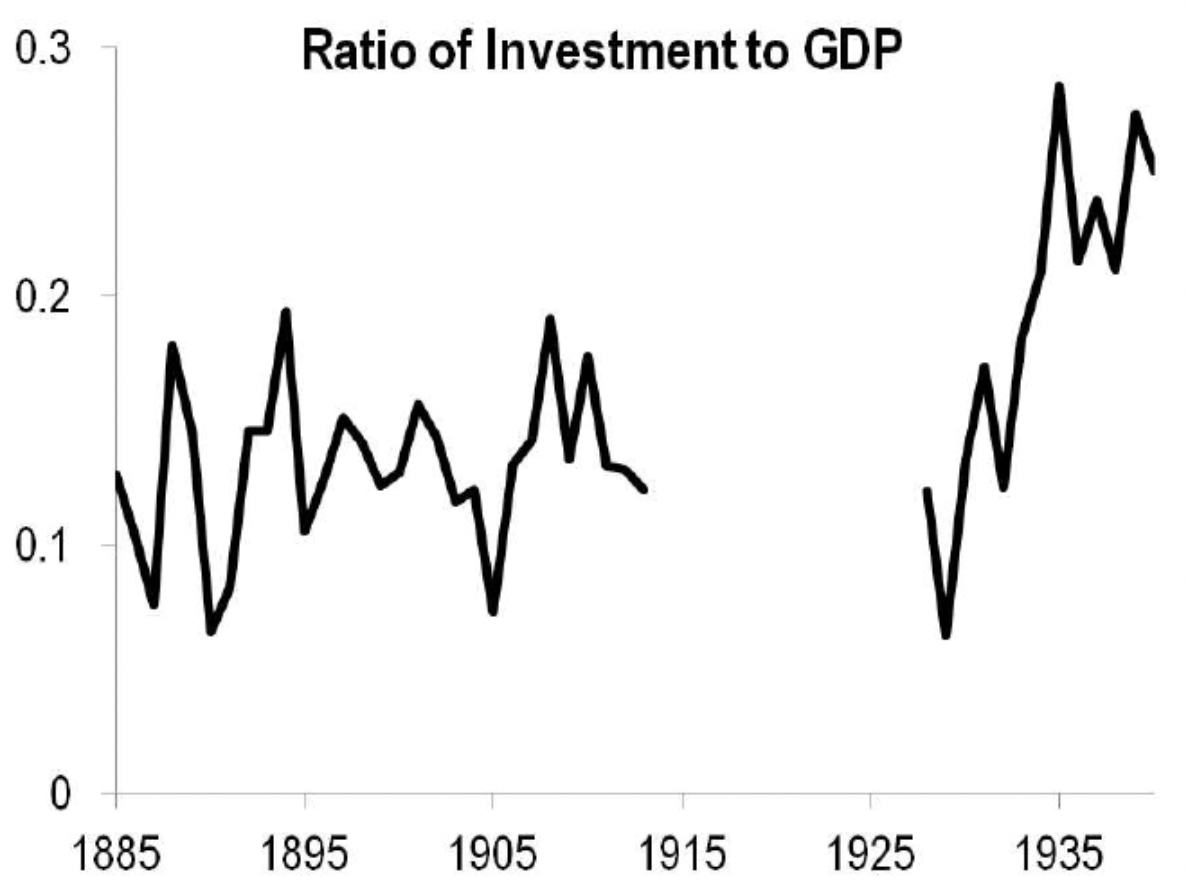

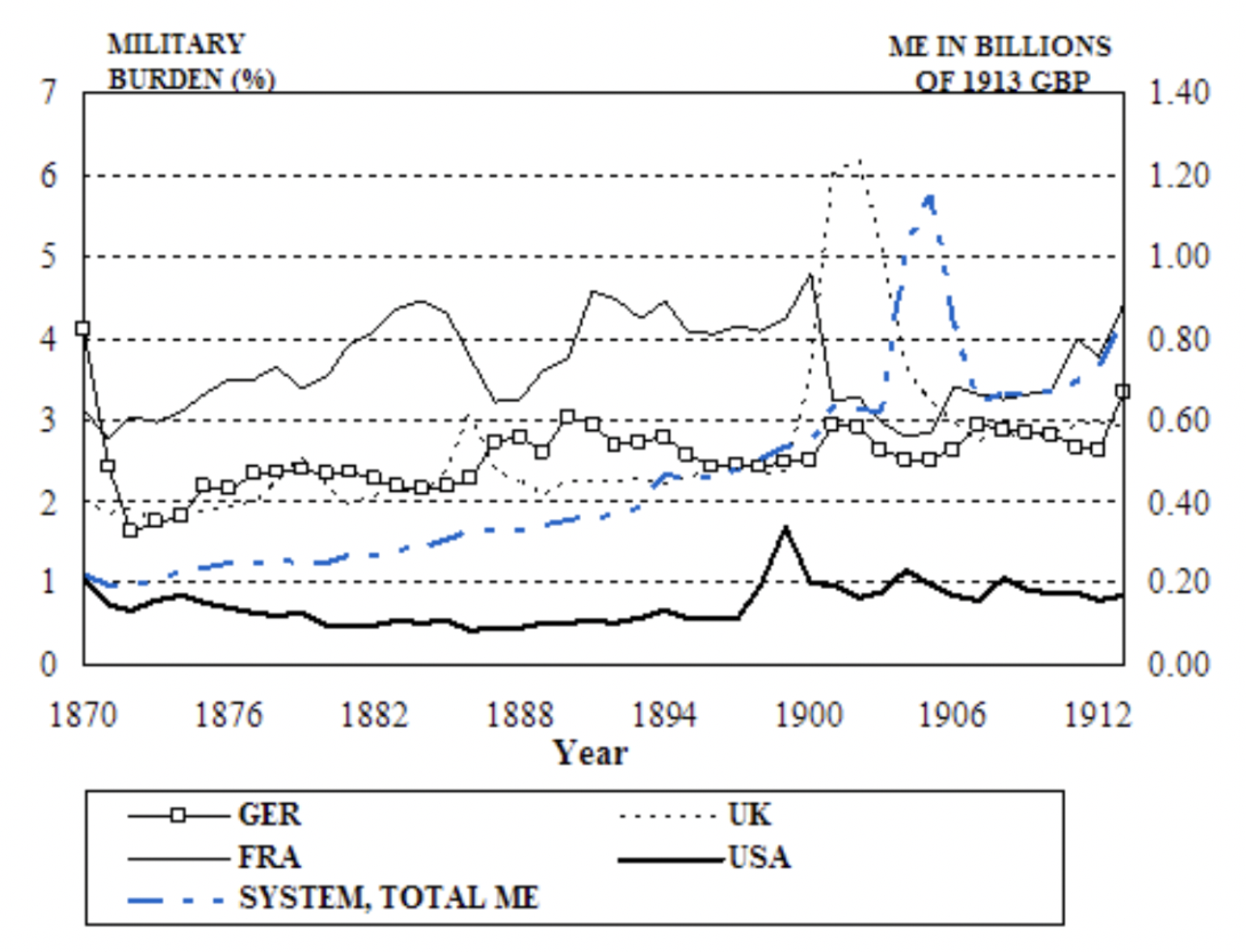

More interesting, contrary to the usual story of a militaristic imperial Prussia/Germany post 1871, the most remarkable period of Prussian/German growth occured after the 1871 unification. After the war, Prussia/Germany's military spending fell dramatically. France became the largest spender among the western powers. Low and behold, it fell dramatically behind Germany economically in the next fifty years. The military spending-economic growth trade-off seems to have been operating:

Source: KENNEDY, P. M. (1987). The rise and fall of the great powers: economic change and military conflict from 1500 to 2000.

Source: EH.net, quoting Jari Eloranta, “Struggle for Leadership? Military Spending Behavior of the Great Powers, 1870-1913

Application to contemporary economies

If by some miracle you're still with me at this point, hopefully you think there's something useful in Kennedy's framework. What would it say about contemporary economies? I think two of the most interesting predictions would be:

- India will grow faster than China in the next twenty years.

- US growth will slow.

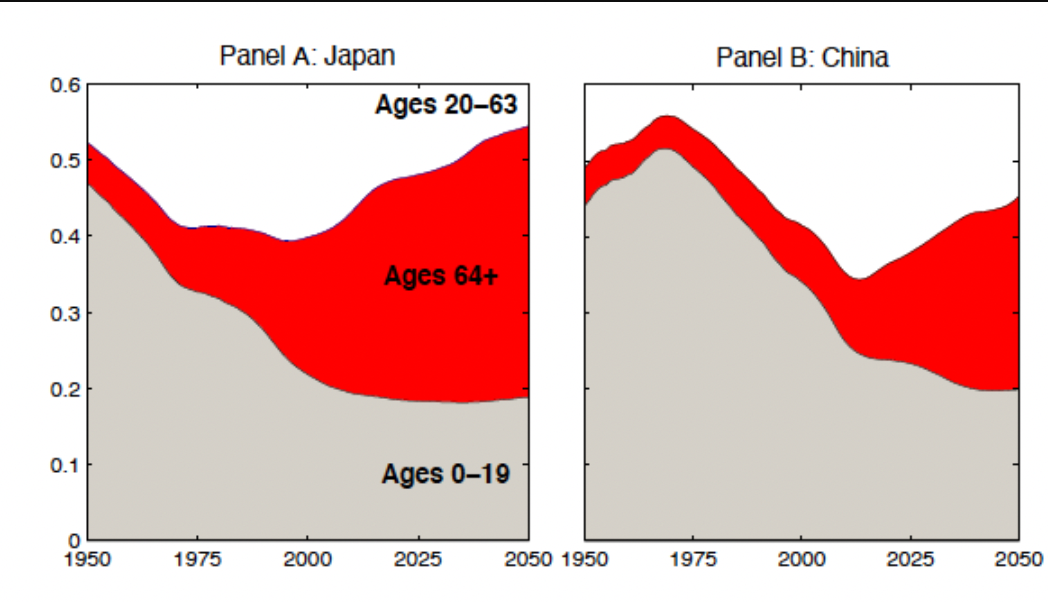

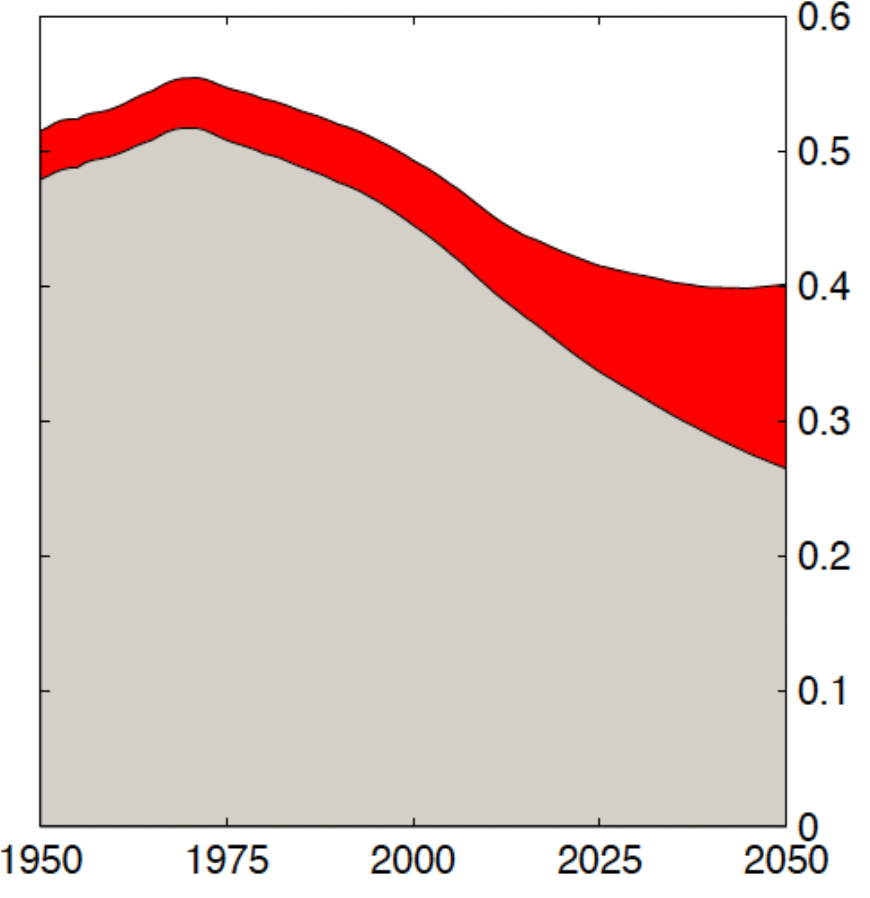

China, India, Japan

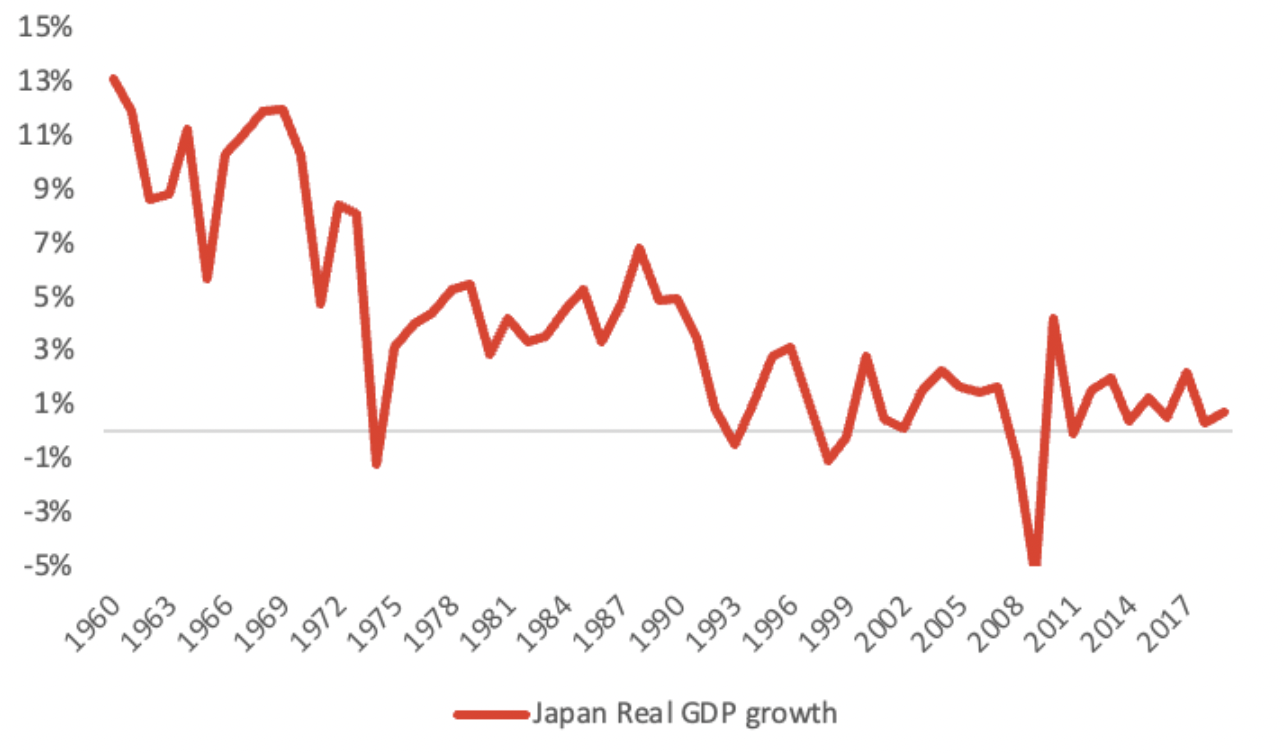

At the end of his book, Kennedy offers some predictions on Japan, America, and Europe up to the year 2000. He gets Japan badly wrong: "Just how powerful, economically, will Japan be in the early twenty-first century? Barring large-scale war, or ecological disaster, or a return to a 1930s-style world slump and protectionism, the consensus answer seems to be: much more powerful.". Although the proximate cause of Japan's problems are the 1989 financial crisis and its aftermath, the deeper cause is that the trade-off of the 1950-70's between domestic consumption and investment went into reverse. This is the hangover of falling fertility rates. Once the population ages and moves into retirement the savings surplus becomes a deficit as retirees consume their savings Since these savings were financing growth the investment rate had to come down and with it, growth:

Source: Calculated from World Bank

Source: Calculated from World Bank

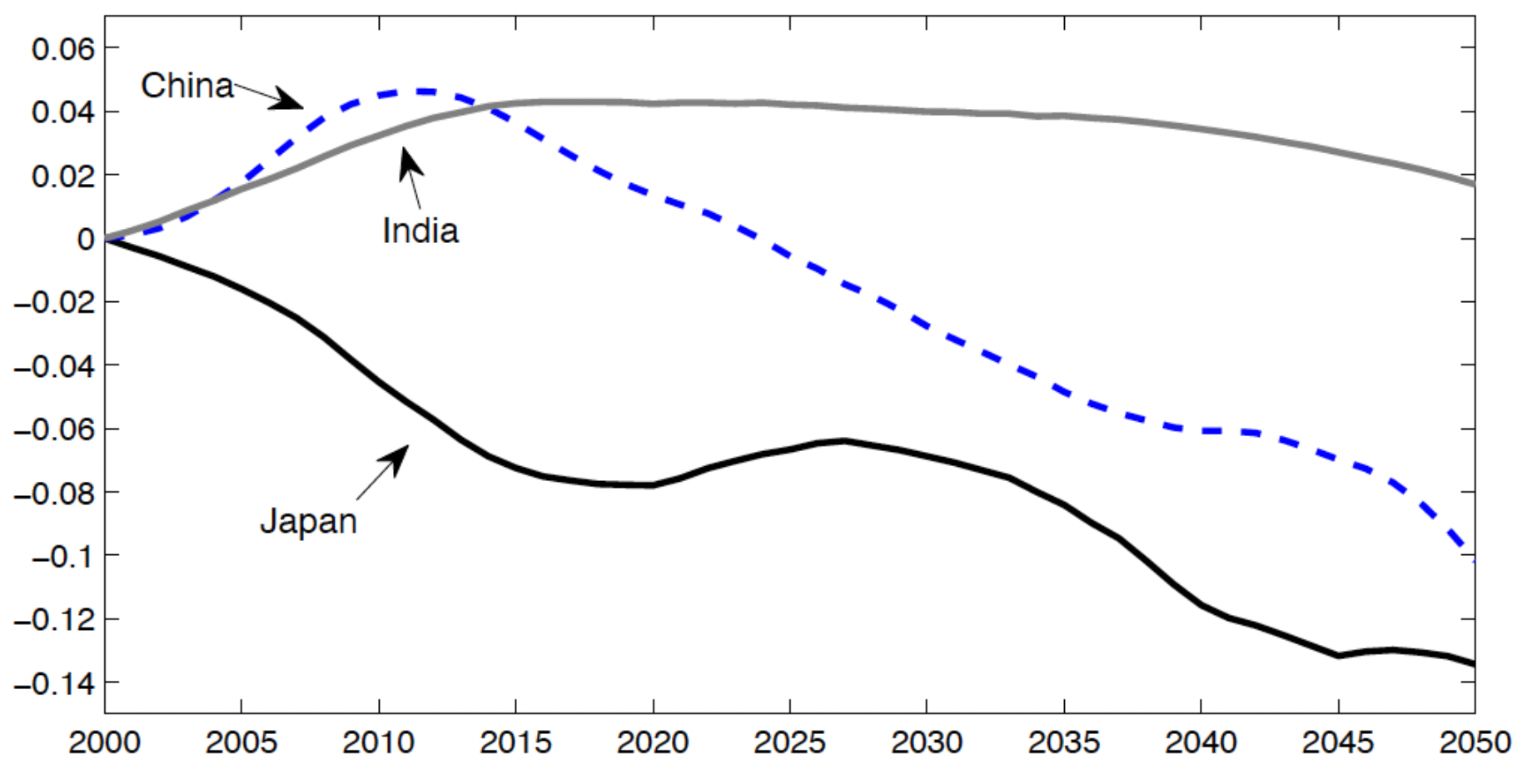

China is now in this predicament. The one child policy created a massive surplus of investment capital that could be used to finance the extraordinary growth of 1990-2015, but we are right on the cusp of the hangover (i.e Japan in 1970):

Source: Demographics and aggregate household savings in Japan, China, and India, Curtis, Lugauer and Mark (2017)

Source: Demographics and aggregate household savings in Japan, China, and India, Curtis, Lugauer and Mark (2017)

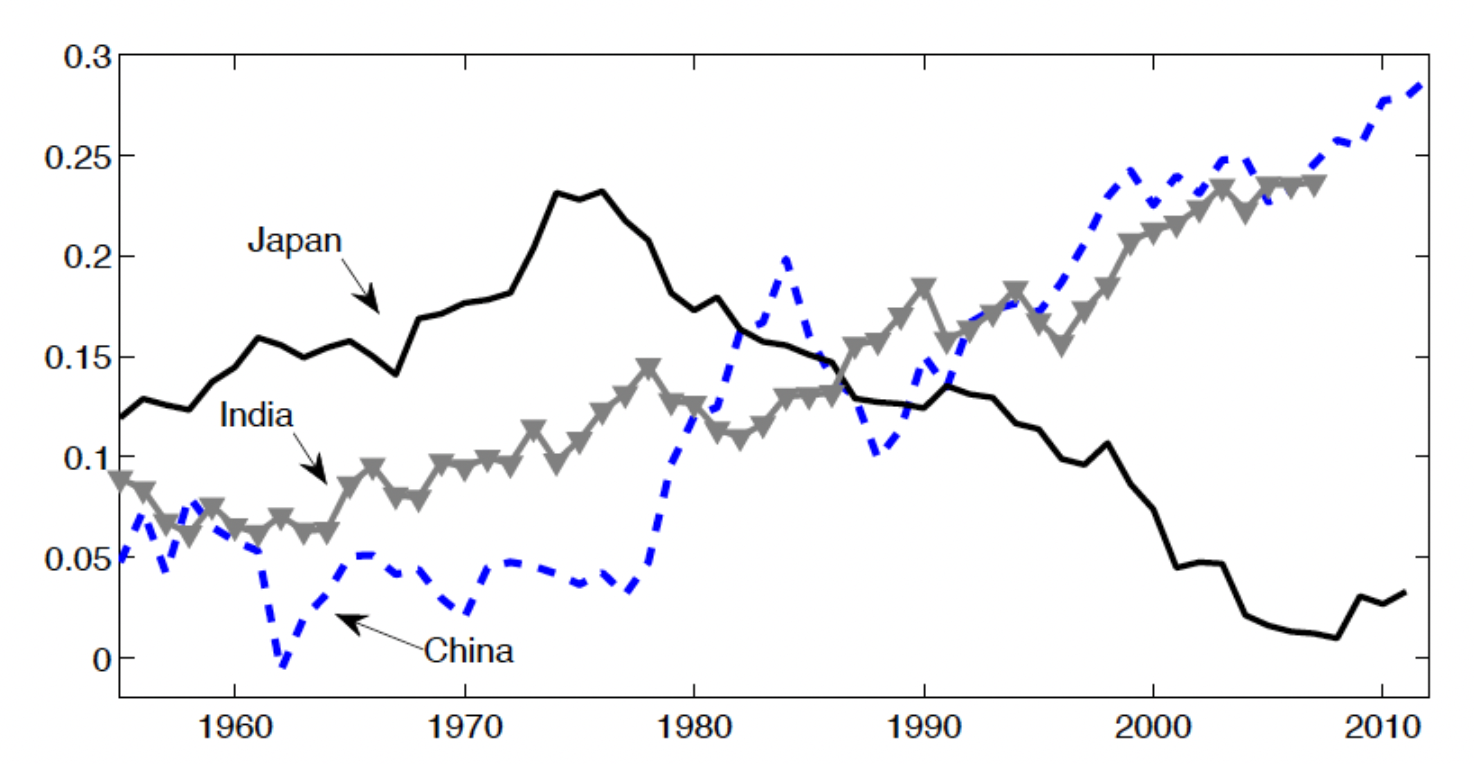

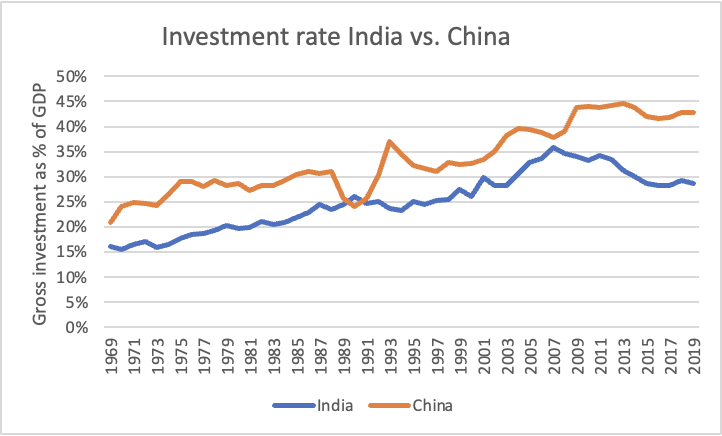

India never had a one child policy, nor is its population as urban as China's (fascinating aside on whether China's example was behind its sterilization flirtation). India's increase in savings and consequent rise in investment capital is hence much more gradual:

Source: Calculated from World Bank

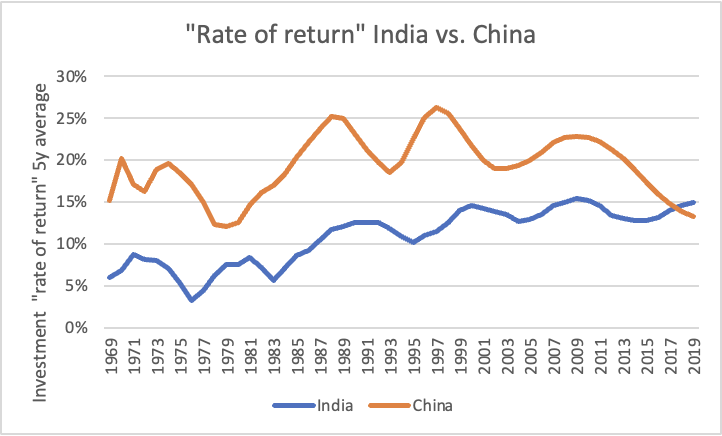

So we would expect India's growth to lag China's - until now. India's savings rates should increase for the next twenty years, while China's must decline

Source: Demographics and aggregate household savings in Japan, China, and India, Curtis, Lugauer and Mark (2017)

Barring a collapse in the rate of return then, India should grow significantly faster than China for the next twenty years.

Barring a collapse in the rate of return then, India should grow significantly faster than China for the next twenty years.

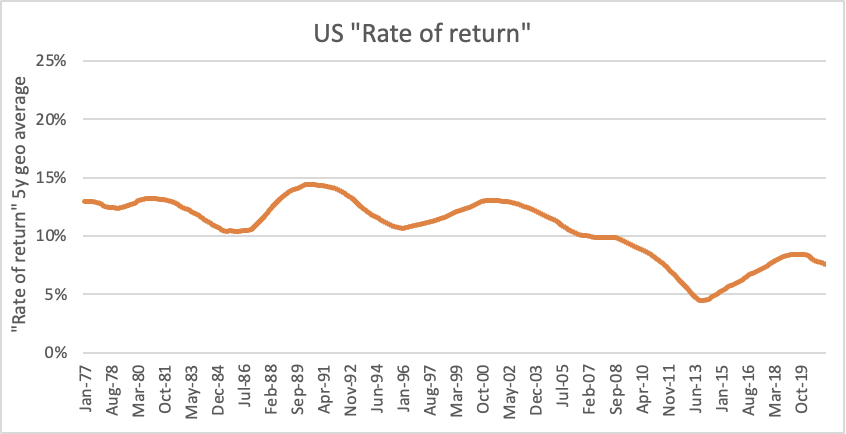

US

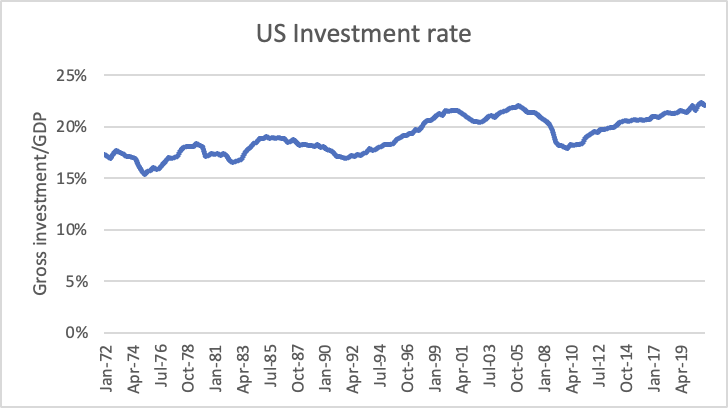

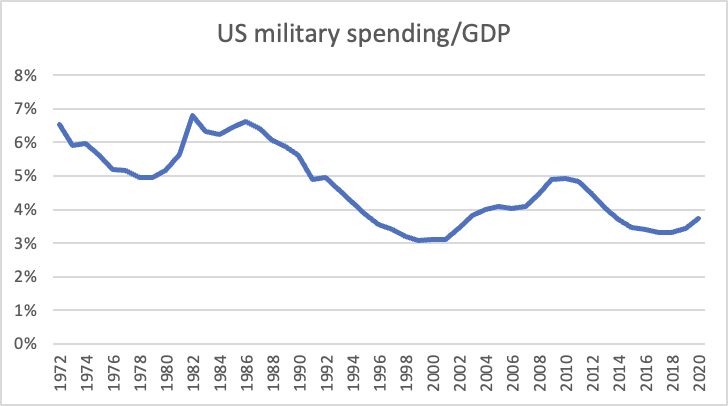

Since the start of the Cold War, the US has had two overriding objectives: to grow faster than the USSR and maintain military superiority or at least parity. Kennedy's framework would suggest that this should come at the expense of domestic stability. I think this is indeed the case, but the mechanism is via wealth redistribution and hence more subtle. From 1970-1991 the US allocated roughly 5% of GDP to the military, whilst the investment rate stayed constant at around 20% (Note also the reallocation into investment after the fall of the soviet union!):

Source: World Bank

Source: World Bank

Whilst the investment rate has stayed constant, the rate of return has come down:

Source: Calculated from FRED

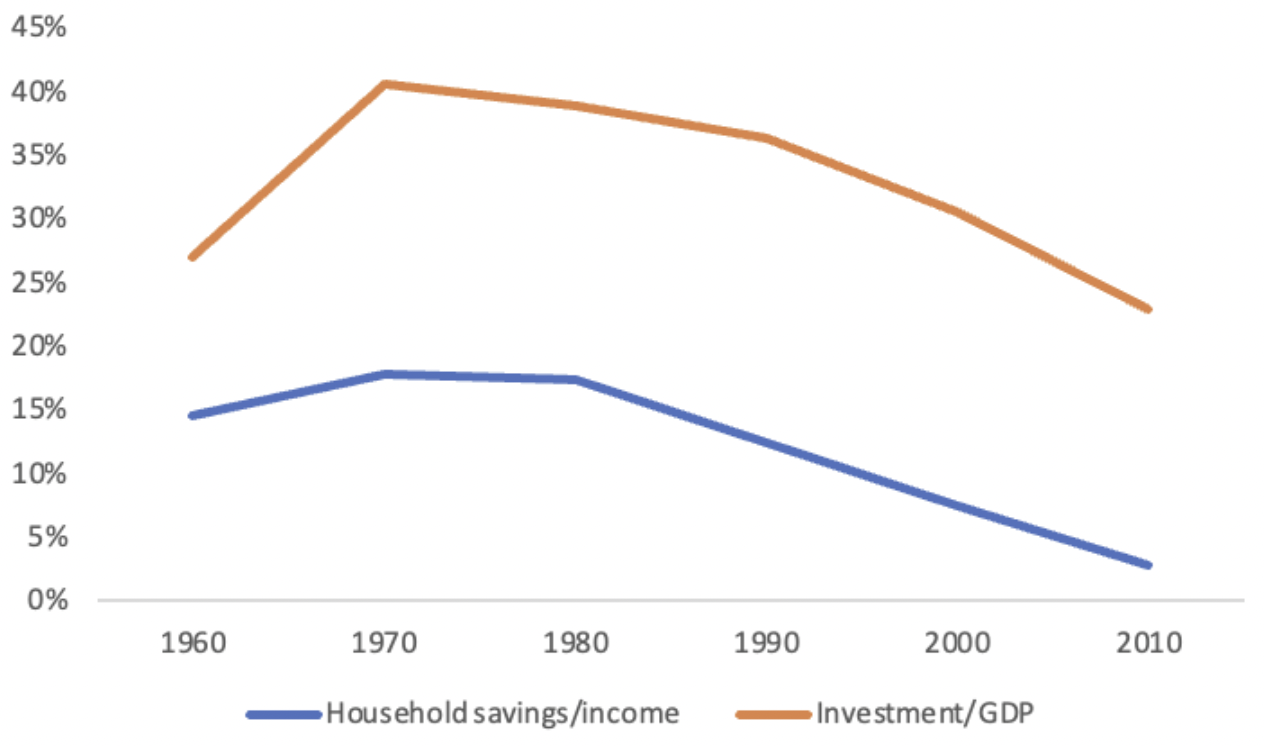

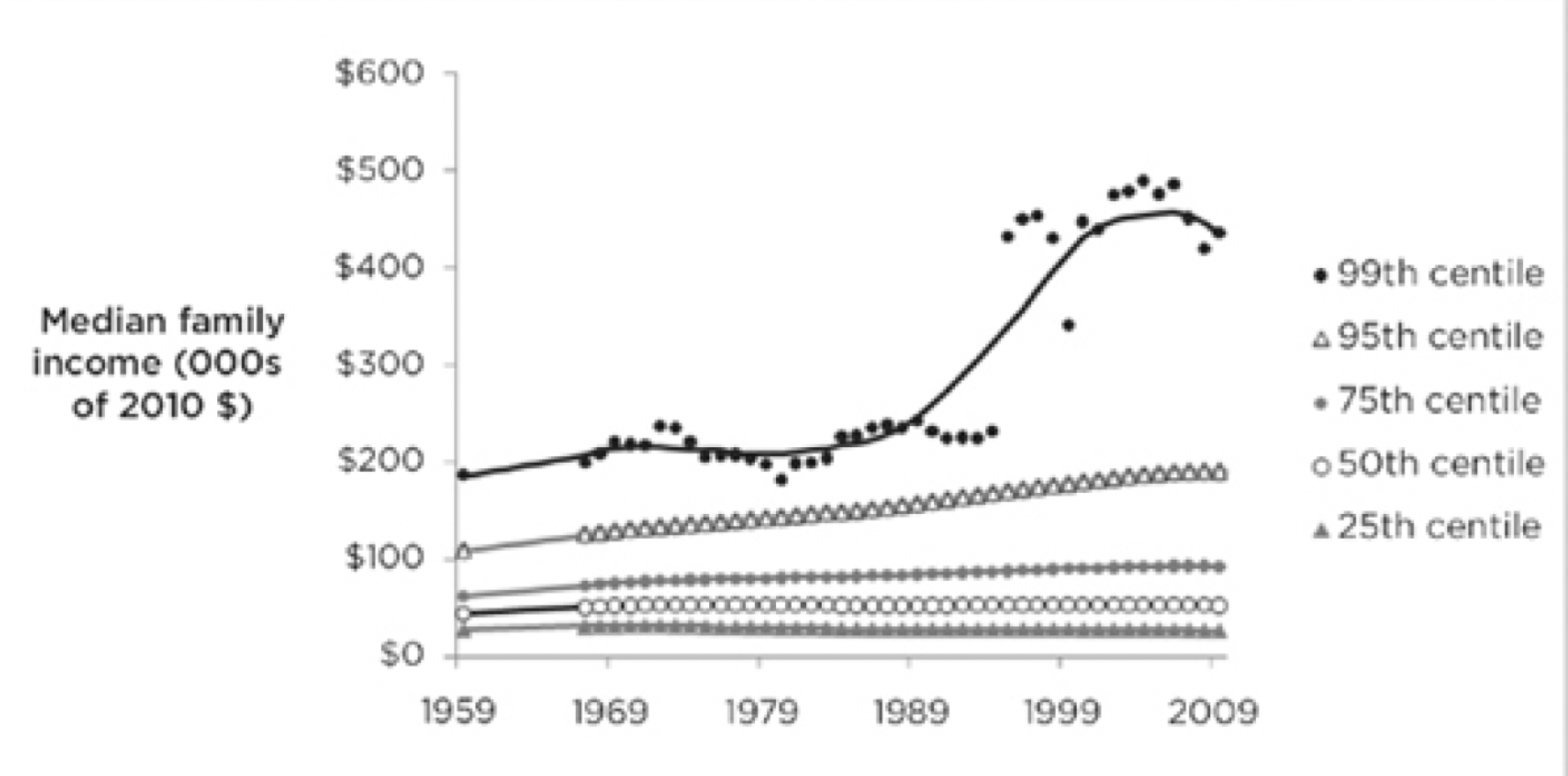

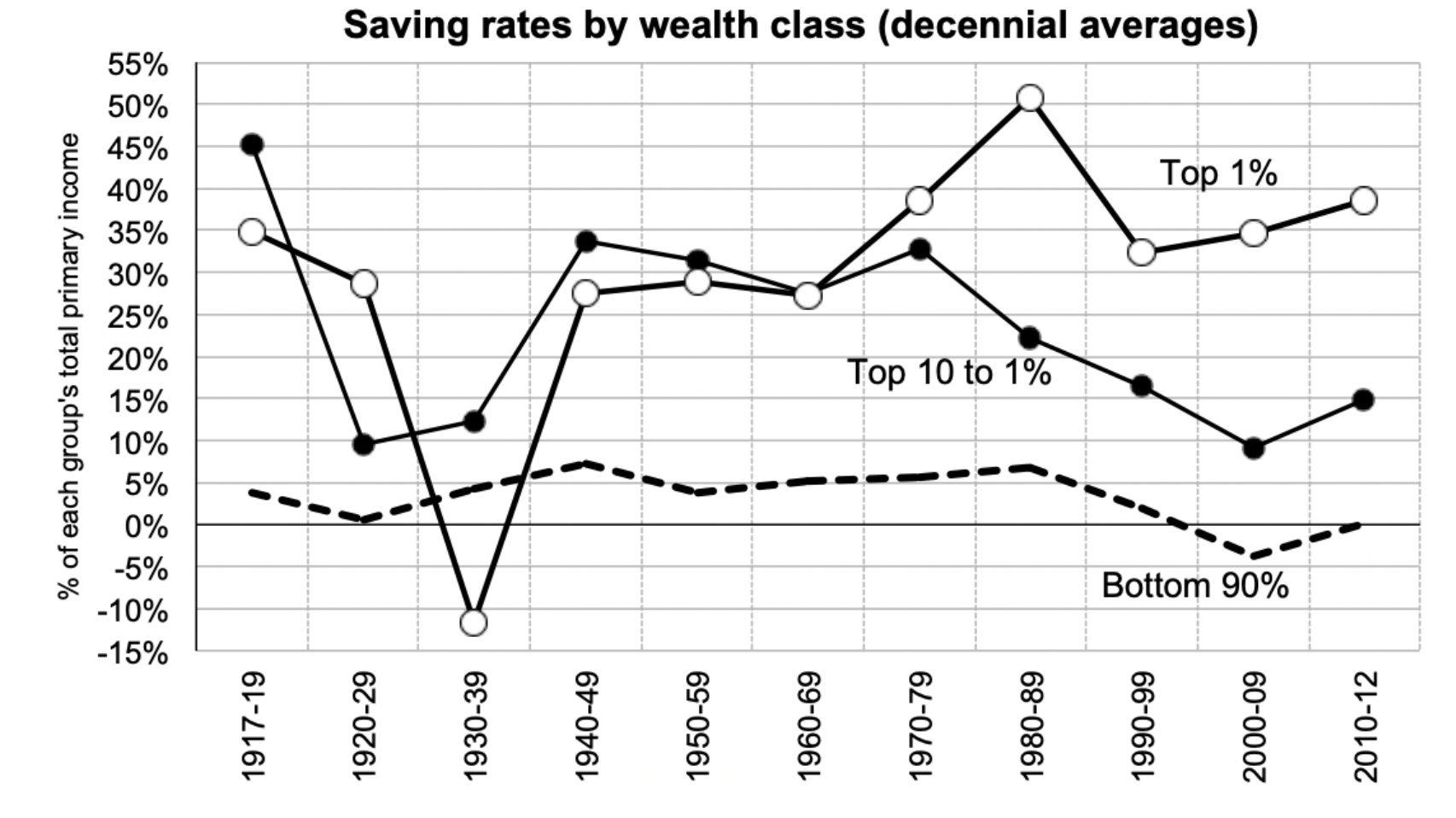

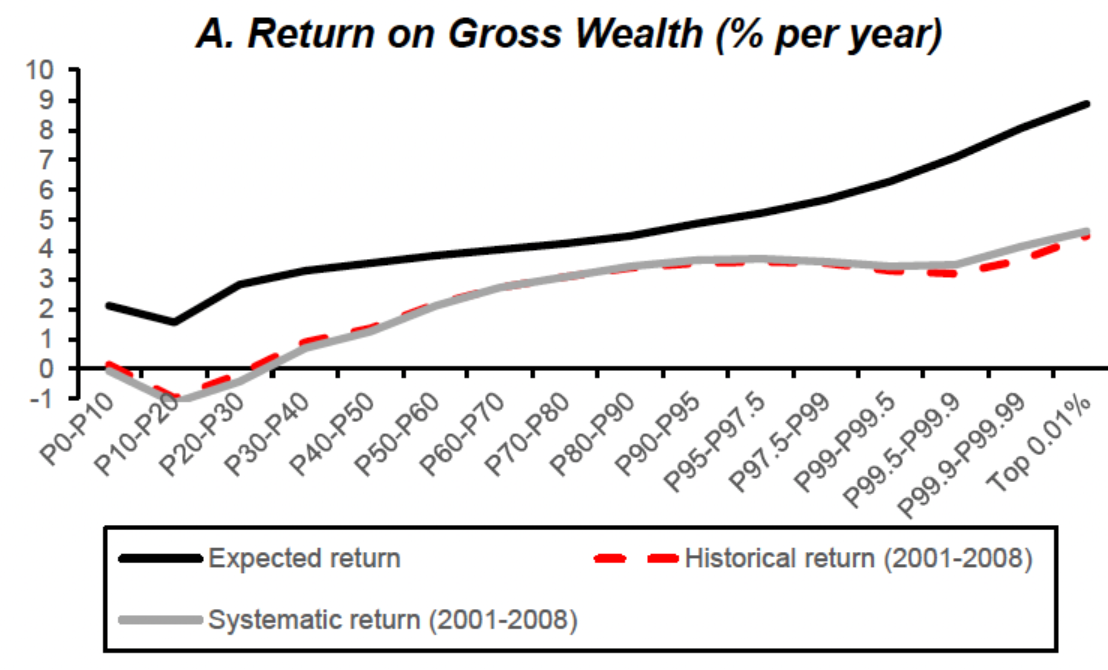

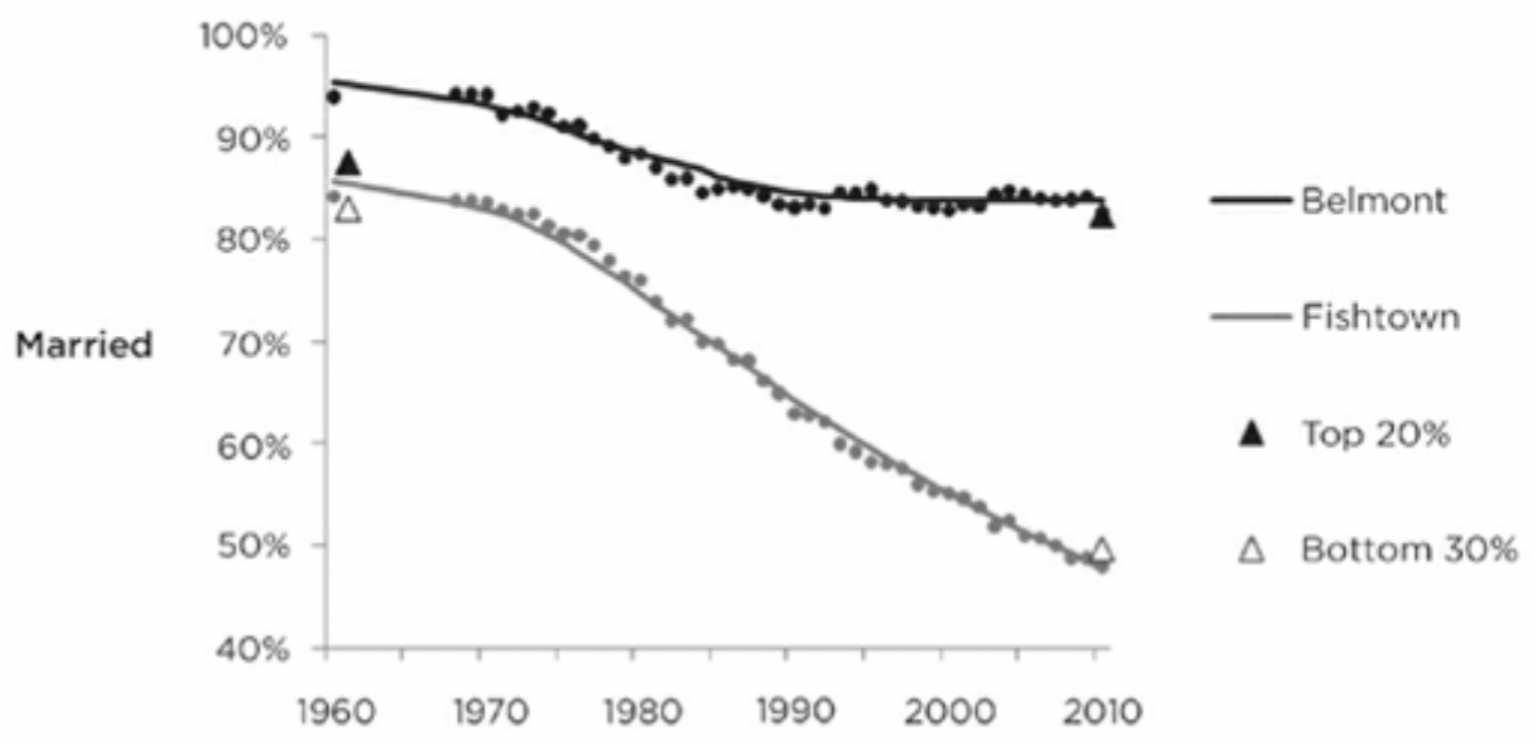

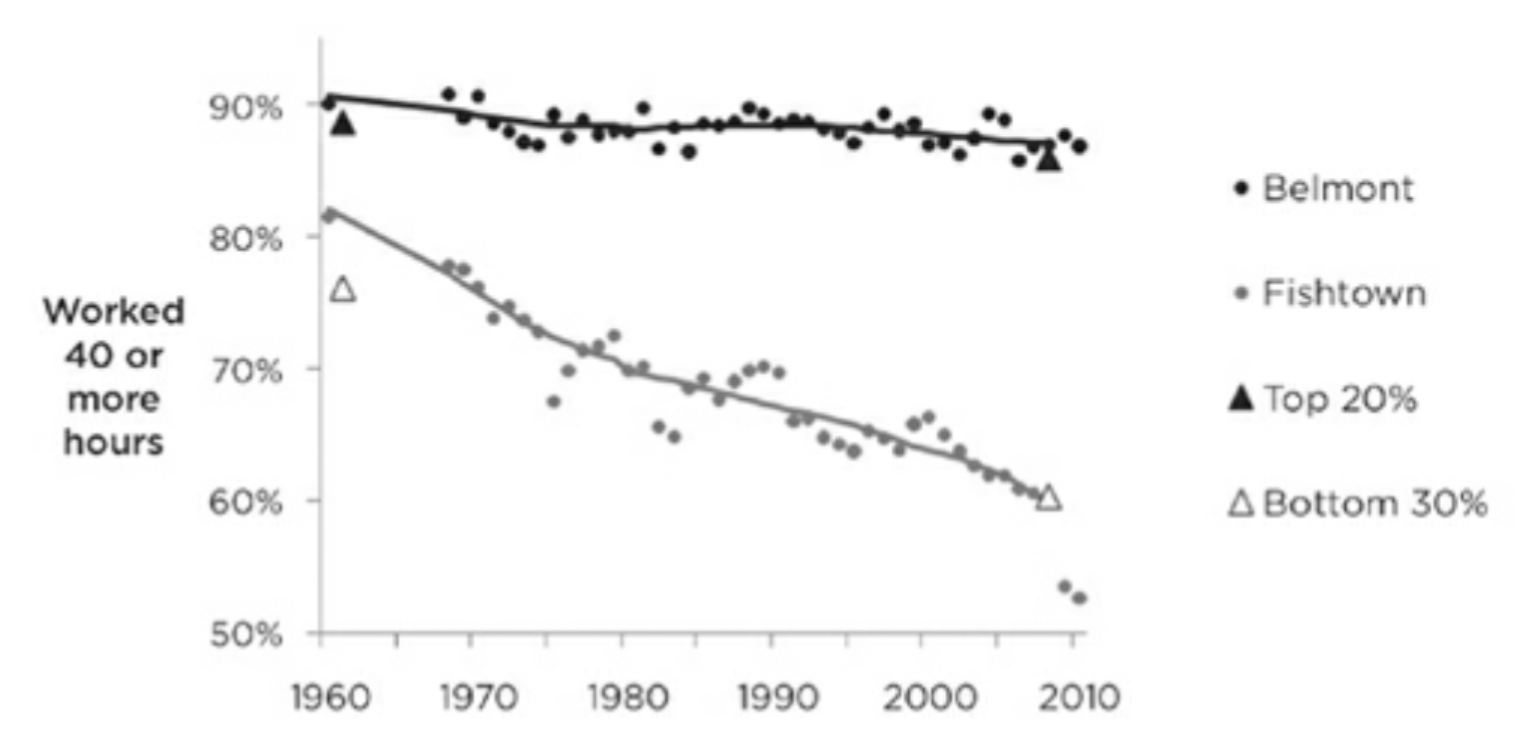

The important context for domestic stability is that this has happened, as in almost all other western economies, against the backdrop of a collapse in the household savings rate. Whilst this would suggest that short term improvements in living standards are being favored over long term investment, the improvement in material living standards has been concentrated exclusively among the wealthy:

Source: MURRAY, C. A. (2012). Coming apart: the state of white America, 1960-2010.

Because the wealthy save a larger proportion and earn higher returns, both the investment rate and the rate of return would have been even lower had growth been shared evenly.

Source: Wealth inequality in the US since 1913: Evidence from capitalized income tax data, Saez and Zucman (2014)

Source: Rich pickings? Risk, Return and Skill in Household Wealth, Laurent Bach, Laurent E. Calvet, and Paolo Sodini, (2018)

As Charles Murray documents in Coming Apart, the consequence is that the American working class have seen a devastating decline in all the metrics that sociologists believe predict happiness - relationship quality, income, quality of work, community participation. Here are two of the easier to interpret ones:

Source: MURRAY, C. A. (2012). Coming apart: the state of white America, 1960-2010.

Source: MURRAY, C. A. (2012). Coming apart: the state of white America, 1960-2010.

Unsurprisingly, the American working class (around 40% of the population as Murray defines it) is unhappy with the establishment political parties. They would like the US to choose domestic stability at the expense of the other two parts of the framework. If America increasingly sees China as a threat military spending will likely remain robust. That leaves only the, inequality-driven, artificially high, economic growth to trade-off.

Conclusion

Predicting the success or failure of nations over the long term is hard. The best that we can hope for is to ask the right kinds of questions. The prime virtue of Kennedy's framework is it helps us to do that. I think we can take away the following general themes:

- The value of this kind of work for economics is that particular case studies can serve as starting points for further research, though they are very weak evidence in and of themselves. Japan from 1950-1964 and India from 1960-2018 saw increasing rates of return with increasing investment rates. This is ,at least at first glance, difficult to explain in a conventional economic analysis that assumes investment projects are chosen in order of attractiveness and so higher investment rates should result in lower average returns.

- Both Stalin's Soviet Union and post WW2 Japan illustrate the importance of savings rates for growth. By the connection with demographics, this is a rare instance of a macroeconomic variable that we can have some confidence in predicting going forward.

- This framework helps us understand the mindset of policymakers. It is striking how directly in Stalin's thinking the analysis of the "productive balance" was. We can see in Stephen Kotkin's biography how prominently this calculation featured in Stalin's refusal to believe that Hitler would go to war with the Soviet Union, France, and Britain. It is also easy to see, perhaps, why savings had such a strong moral component before 1950 - the fate of the nation hinged on having enough capital to outgrow its competitors.

- I have frequently added tidbits from other literature to this review. The framework Kennedy proposes is sufficiently general in order to allow us to probe each trade-off in more detail. The Technology Trap, say, is a great example of the domestic stability vs. growth trade-off. Coming Apart tells us about dynamics internal to domestic stability, and we can use then relate the findings back to the framework.

3 comments

Comments sorted by top scores.

comment by jacopo · 2021-10-14T09:11:09.604Z · LW(p) · GW(p)

On Prussia:

- they managed to have almost the same GNP as France while keeping larger military spending, it's not surprising that they won the war

- of course, it may be surprising that they managed to get there. Given the model, you would expect that they sacrificed internal stability, but in fact it was France that was the most unstable country in that period! (Revolution, Napoleon, restoration, second Republic, second empire)

- you could say the political instability may have really hindered France, forcing higher consumption spending, but how comes this was true only post-napoleon?

- back to Prussia: it is the case that they never needed to maintain superiority over Austria and France over a long period. Nearly everyone in Germany wanted to unify, the question was how/under whom. The Prussians in 1970 needed few quick victories to convince everyone that they were the only choice. For this reason they could focus on the short term. After that, they absorbed the rest of Germany which had focused on economy. Compare the parallel unification of Italy under Piedmont/Sardinia, a much weaker power that played a similar strategy.

It's not a coincidence that Hegel came up with the Zeitgeist idea exactly in 1800s Germany...

My overall take is that this is an useful starting point, and that structural factors are often underestimated, but the model is too simplified to actually make predictions with any confidence.

Replies from: TheRealSlimHippo↑ comment by dmanningcoe (TheRealSlimHippo) · 2021-10-17T03:05:07.369Z · LW(p) · GW(p)

These are great points, thank you for pointing them out. I think I agree with your overall take - the analysis is not finished with Kennedy's framework, rather it's a good place to start. We can then go into more detail on each trade-off - analyzing why Japan gets to an investment rate of 45% whereas the Soviet Union only to 30%, say.

On your specific points:

1. Good point - although I think this can only be taken so far. The Entente powers spent less on the military but had slightly higher overall economic output, and that's why they had an advantage. Certainly its unusual that Germany would defeat France so decisively.

2. I agree! Which I think is one of the reasons why Prussia sits uneasily in the framework. I think its worth noting that whereas France had domestic issues - Prussia had significantly worse external problems. These caused far more destruction than France's convulsions. The "Miracle of the house of brandenburg" and the fact that the non-Russian Napoleonic wars were fought mostly in Germany come to mind.

3. Why do you say it wasn't true pre-Napoleon?

4. I think I have to disagree here. Prussia was in a century and a half contest with Austria the moment it seized the Silesian coal fields. I agree that quick and decisive victories did the trick, but the difficulty is its not clear how Prussia managed to win decisive victories whilst not falling behind economically.

Replies from: ADifferentAnonymous↑ comment by ADifferentAnonymous · 2021-10-19T02:54:53.994Z · LW(p) · GW(p)

Maybe military spending has a variable 'rate of return' just like investment? That would allow the Prussian army to get more bang for its buck, which fits my impression of what happened.