2024 was the year of the big battery, and what that means for solar power

post by transhumanist_atom_understander · 2025-02-01T06:27:39.082Z · LW · GW · 1 commentsContents

The economic niche of battery energy storage Economic comparison to natural gas peakers The niche pays better The near future of electricity generation None 1 comment

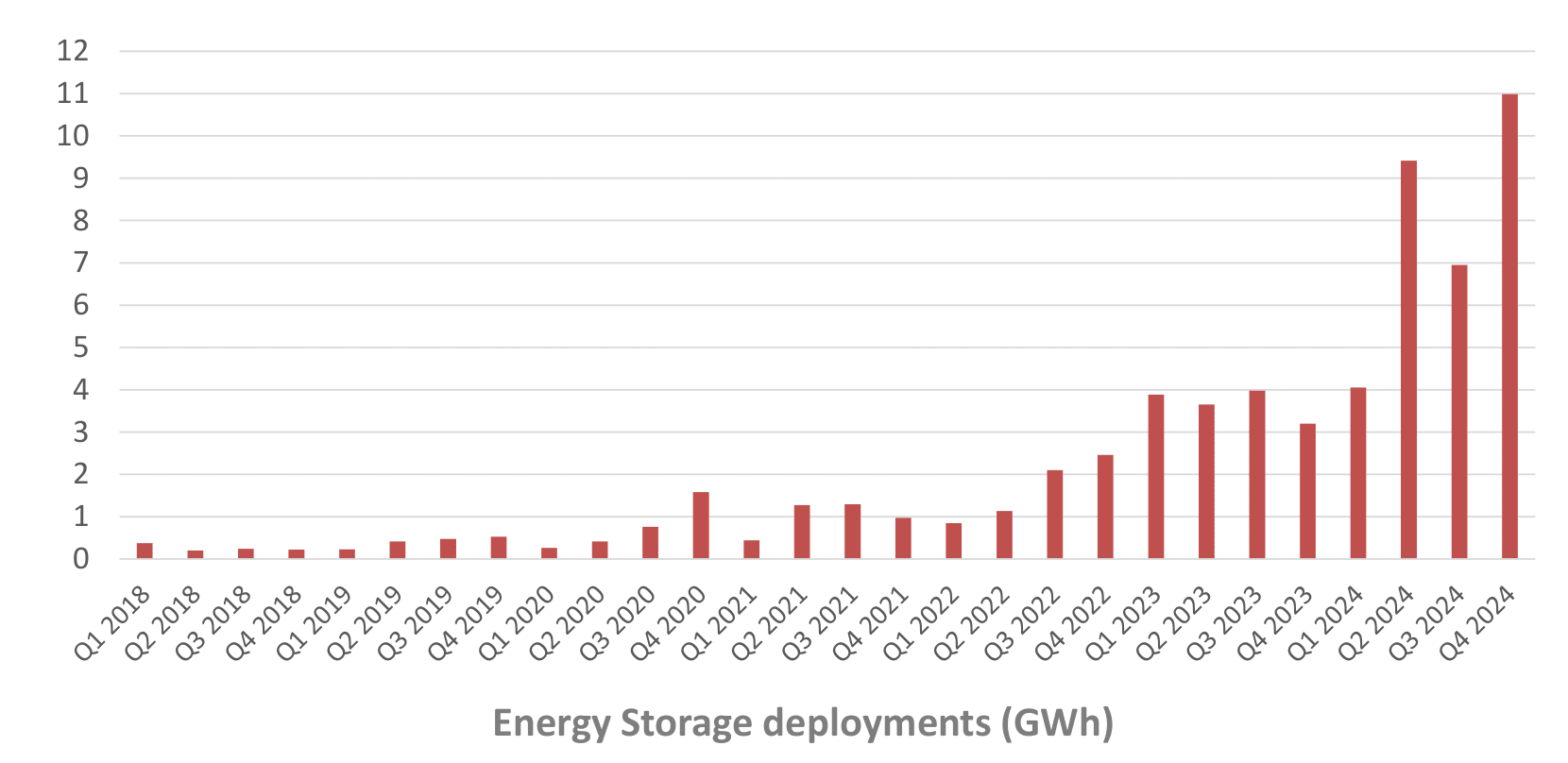

The sunlight hitting even a small portion of the United States has enough energy to power the whole country—that simple calculation was the subject of the last post [LW · GW]. All this shows on its own is that running the country on solar power is physically possible. With photovoltaics it may be not just possible but practical, but photovoltaics on their own left open the question of what to do at night. Now it seems that the answer may be battery energy storage. Here's Tesla's sales of battery energy storage systems again, but updated since my last post to include 2024 Q4:

It's natural and popular to believe that solar will either "win" or "lose", that declining panel and battery prices will bankrupt the competition or that they'll be revealed as a ruinous environmentalist fad. The reason I say this dichotomy is natural is because naively it seems that the solar+batteries approach must either be cheaper or more expensive than the competition. But after looking into the economics of batteries, I think a third possibility is also plausible: that solar+batteries will coexist with other forms of generation. I mean not only will other forms of generation continue operating, but they will continue to be built, even in prime solar areas like California and Texas. This is because batteries are competitive in a specific economic niche, which I call "peak adjustment": "adjusting" the solar generation peak to match the demand peak. I'll explain what this niche is, and illustrate it with data from California and Texas.

In the end, I won't have a firm prediction of what will really happen, but I will clarify what it depends on. It does not depend on just the current price of solar and batteries; we have to take into account that they are getting cheaper. But looking at just the direction of the trend isn't enough either. The future depends on the numbers: how much do prices have to decrease for batteries to serve in a particular role, and how long would that decrease take? I'll provide some crude estimates for these numbers. The probability mass of the hypothesis of "peak adjusting" batteries lives in the space between the price decrease required to dominate this niche, and the price decrease required to supply all power.

The economic niche of battery energy storage

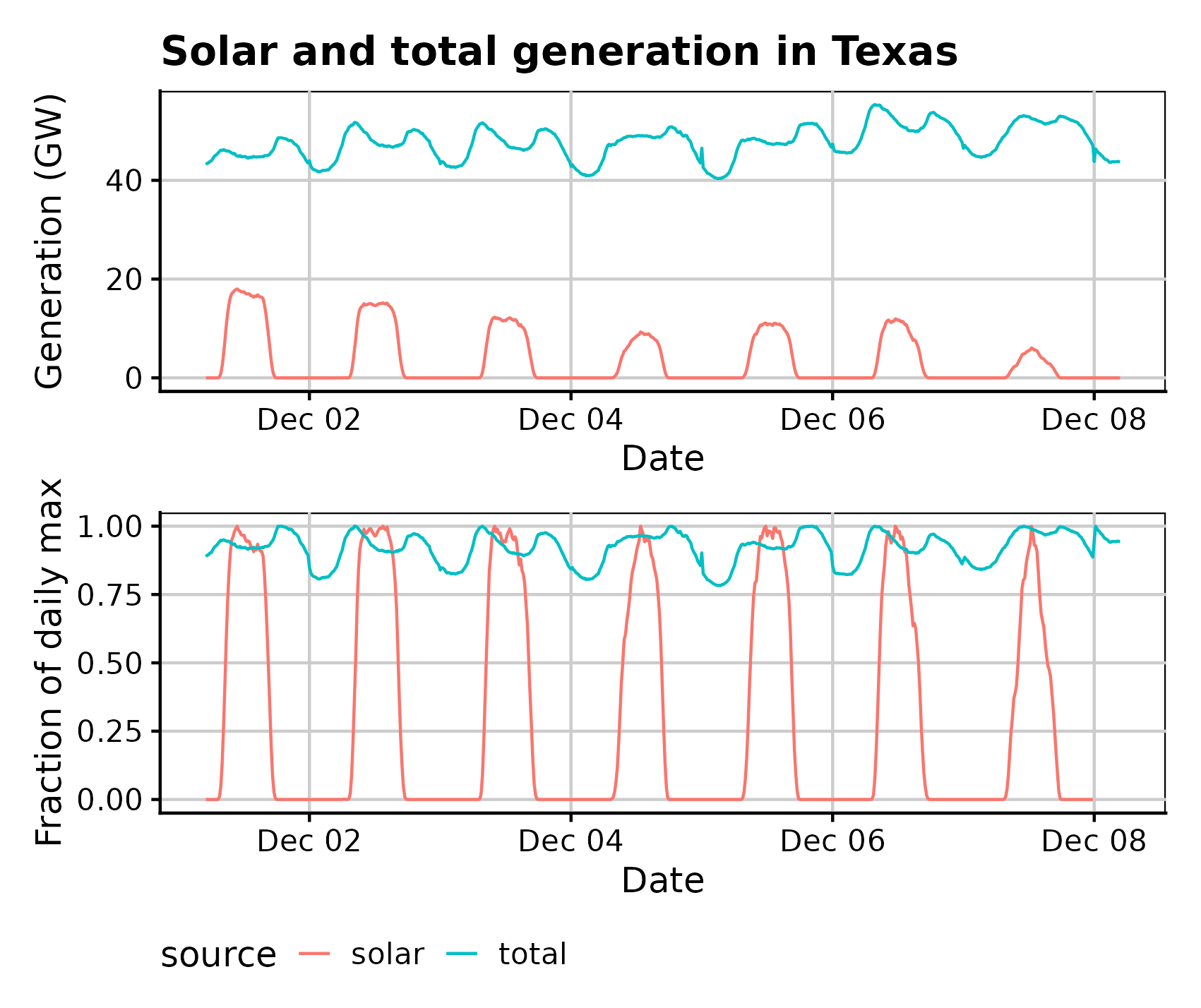

Solar generates during the day, and people use more electricity when they're awake. What could be more convenient? The problem is that these two peaks, the solar generation peak and the demand peak, do not match. Illustrating this with a week of generation in Texas, in December 2024, using ERCOT data:

In the bottom plot, I normalized to the max of each peak for that day, so you could see the mismatch better. This is in December, when the days are short, so you should consider it extreme, not typical. The mismatch between these peaks raises an awkward question for a solar-heavy grid: how to "adjust" the generation peak to match the demand peak?

The only way to supply the electrical power that is not coming from solar is by using combustion gas turbines that can ramp up and down quickly enough to follow the changes.

And in 2017, it really was the only way, at least in flat and dry places like Texas. Hydroelectric can also serve this role but is limited by geography. Only in the past few years—substantially just this past year—have batteries established themselves in the same role in the electric grid.

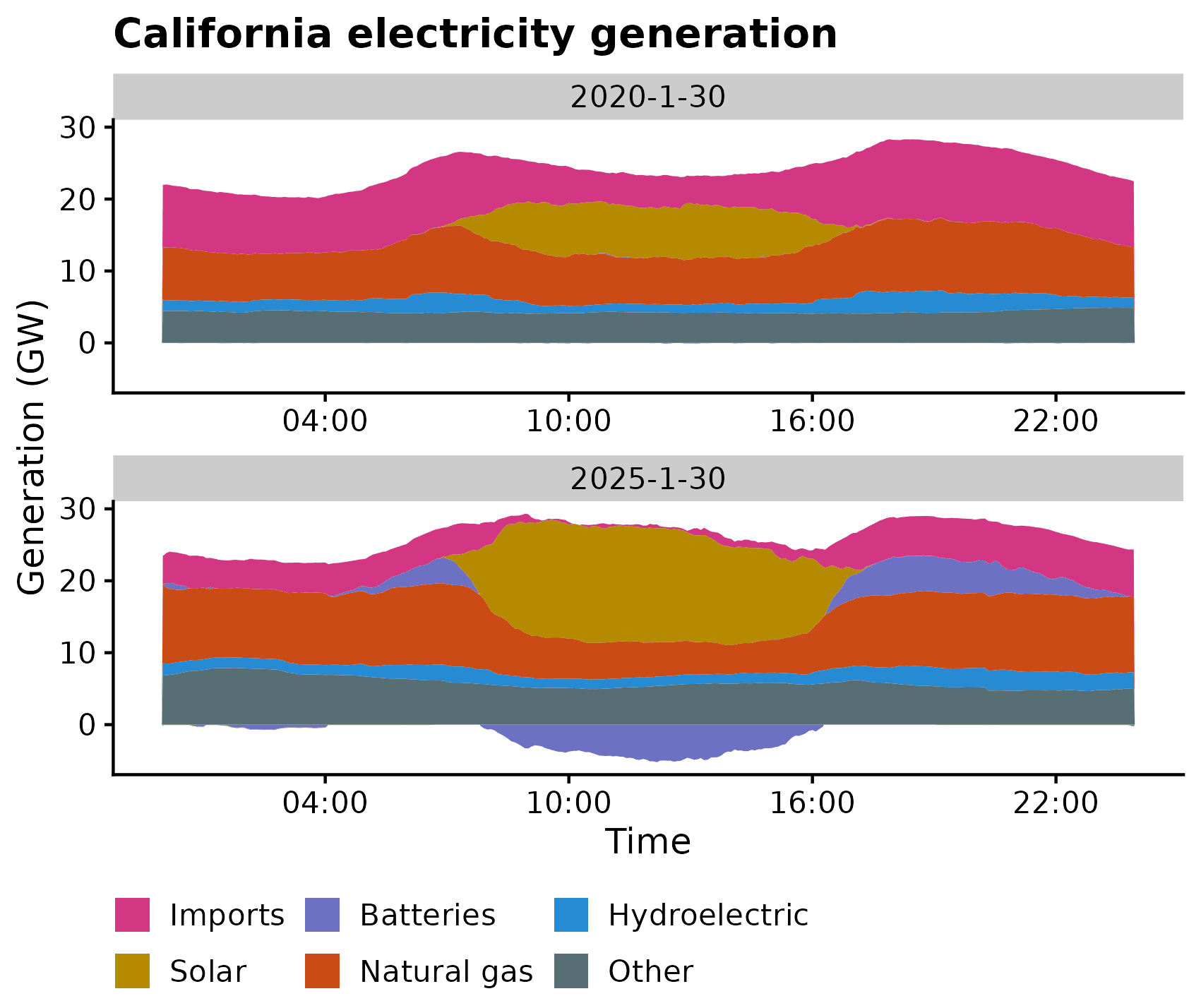

To see the difference over the last five years, I looked up data for generation in California from CAISO. I plotted a single day—namely yesterday, and the equivalent date five years ago. Again, the daylight hours are short, so you can consider this an extreme example of peak mismatch rather than a typical one.

You can see two local maxima of natural gas generation in 2020, in the early morning and early evening hours when people are awake but the sun isn't shining. On the same date in 2025 and at the same times, we see peaks of batteries discharging. (I assume negative generation from batteries corresponds to batteries charging.)

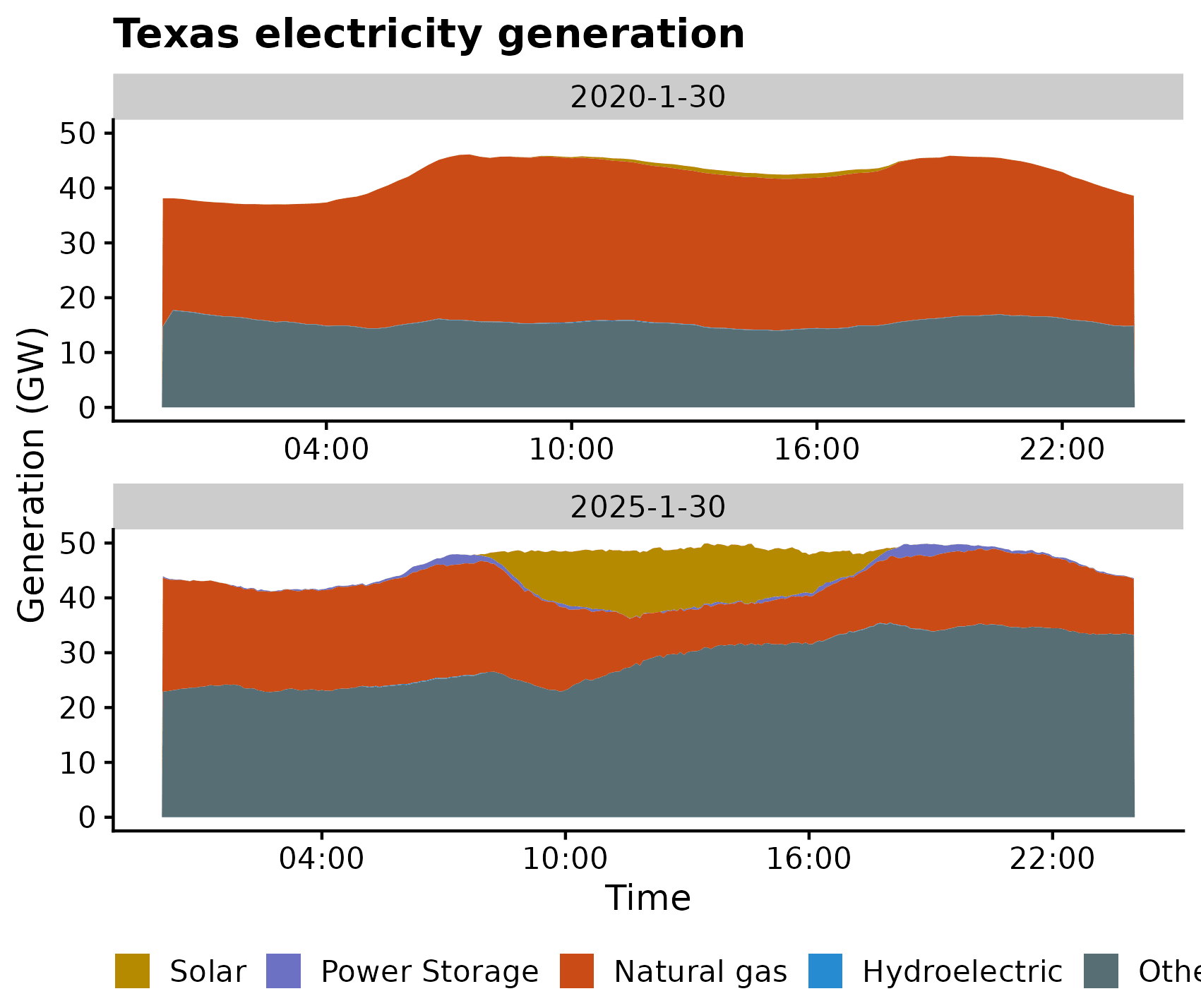

In Texas, using ERCOT's 2020 fuel mix report and their dashboard:

I assume "power storage" is almost entirely batteries, and I suppose this data doesn't include charging as negative values. We only really see peak adjustment of any kind recently, since Texas didn't have much solar until recently. But in Texas the use of natural gas to adjust the solar peak is much more clear than in California, which seems to rely as much on imports as flexible gas generation.

In California especially I was surprised how late into the night batteries are discharging, which challenges my peak adjustment story. But in both Texas and California, batteries are primarily discharging in the "peak mismatch": in the early evening after sundown but before lights out, and in the early morning when people wake up before sunrise.

Economic comparison to natural gas peakers

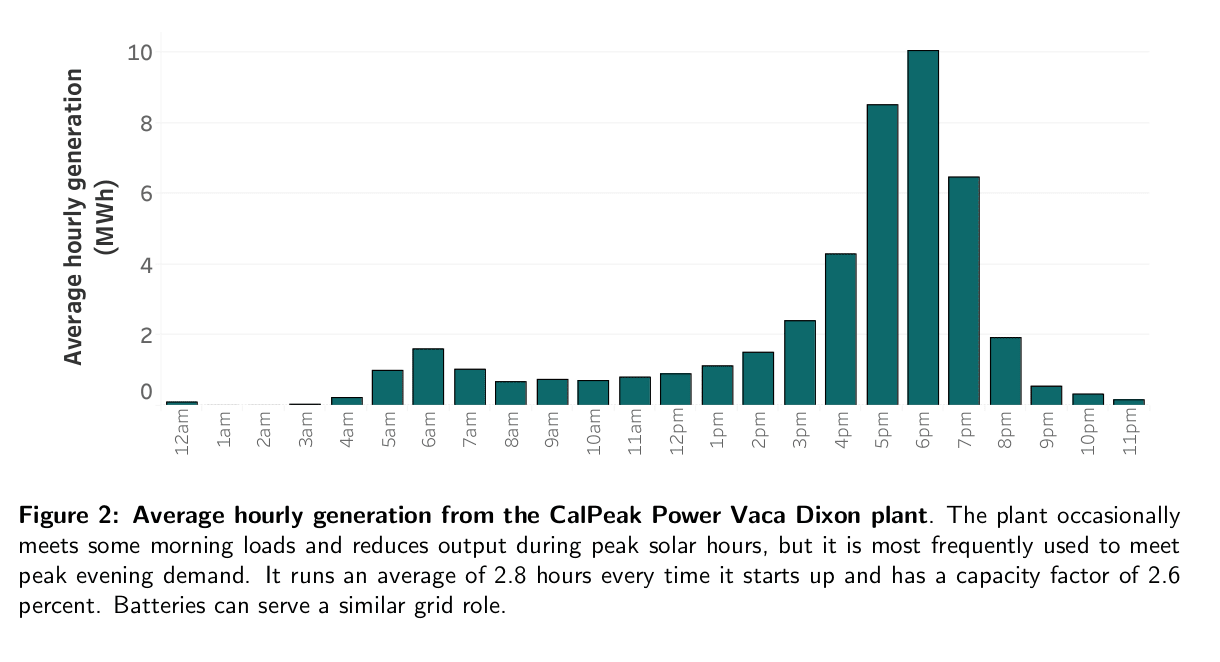

The key to understanding the success of batteries in this peak-adjustment niche is understanding the weakness of the competition, namely natural gas. In short, it's hard for a natural gas plant to make back the money invested in it if you only run it for a few hours a day. People do build such plants, called peaker plants—see Figure 2 of this report for an example of how little they generate throughout the day:

I've gotten the impression that you can build 1 GW of natural gas capacity for less than a billion dollars—maybe 0.8 billion, according to an EIA report? Let's round up to a billion, and consider what kind of battery storage facility you can build with a billion dollars. By the way, people sometimes call such a facility a "big battery", like the "Victorian big battery". But if you're imagining a "big battery" as some towering obelisk of lithium, I have to give you the disappointing news that it's actually a collection of modules. One way to build a "big battery" is to buy Tesla Megapacks, conveniently shipping container-sized modules that you affix to a concrete slab (image source):

The current price, rounding a bit, is about a million dollars per Megapack, which stores 4 MWh of energy. So for a billion dollars, you can buy a thousand of them, which would provide 4 GWh of energy storage. If the batteries are charged once a day during the daylight hours, then they can provide 1 GW of power for four hours, which is enough for peak adjustment, depending on the season.

This crude calculation is enough to show that battery prices have already fallen to roughly the same range as natural gas construction costs. Neither has an obvious overwhelming advantage over the other. I think the continued decline of battery prices will eventually tilt the scales definitively in favor of batteries. The key conclusion of this financial arithmetic is that battery prices don't have to decline that much to get ahead in this niche, if they're not already there.

But we can also adjust our financial arithmetic: what if instead of supplying four hours of power to adjust the peak, we wanted to supply the twelve or so hours without sunlight? Then instead of 4 GWh of batteries, we would need 12 GWh to replace a 1 GW natural gas plant. This would cost three times as much in capital investment. So when the battery price drops to the point that batteries can compete with gas in the 4 hour peak adjustment niche, they may have to then drop by an additional factor of 1/3 to compete at supplying power all night.

Although I'm ignoring everything but capital costs and making up numbers, the key point is that battery prices are already around the level at which they can substitute for a natural gas peaker plant, but substituting for a natural gas plant that runs all night requires a larger investment in batteries, and thus requires a lower battery price to be competitive.

The niche pays better

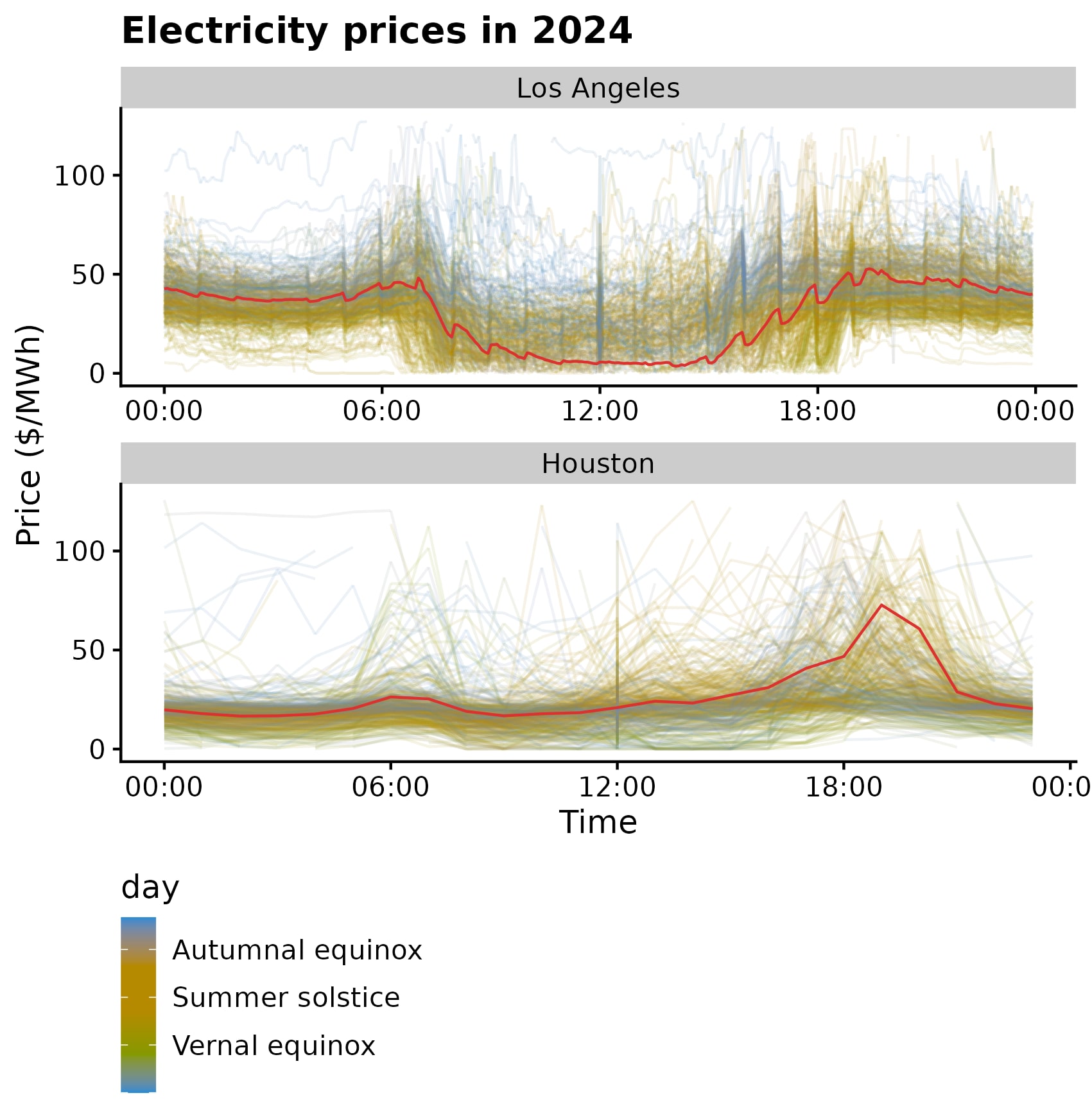

We can understand the economics of peak adjustment better, though, if we take the perspective of a Megapack owner. If we can make money by buying a Megapack, charging it with solar at noon, and discharging it in the early evening, what stops us from making money by buying a Megapack and discharging it at midnight? The answer is that in a solar heavy grid, electricity prices tend to be higher during that peak mismatch. I've retrieved prices from energyonline.com and plotted them throughout 2024, in Los Angeles and Houston, showing each day's prices with a transparent curve and the average with a solid red curve:

In Los Angeles, although there are occasionally price spikes during the peak mismatch, on average the price is not really that much higher than at night. But in Houston, the prices are much higher: the ratio of the maximum to the median of that averaged curve is 3.18. If batteries are just barely worth it for peak adjustment, then they would have to drop to about 1/3 of their current price to be worth it for supplying power in the middle of the night. That's the same ratio that we got from the arithmetic in the previous section, and though getting the same integer is just a coincidence, it backs up the impression that battery prices may have to drop significantly to escape the peak adjustment niche. I'm not sure what explains the difference in the electricity price patterns between the states.

The near future of electricity generation

Two independent lines of reasoning lead me to believe that batteries are either competitive or close to competitive with natural gas for peak adjustment. The first was a simple observation that people are in fact using batteries in this way, and the second was comparing capital costs using the Tesla Megapack price. But all this really established was that battery prices are somewhere in the neighborhood of being competitive. Here's where I want to invoke the declining price of batteries. Another 20% decrease or so in the price could bring them from the neighborhood of competitive to being competitive, or turn a small lead into a decisive one.

But for going beyond peak adjustment, and using batteries to supply stored solar power in the middle of the night, a 20% decrease in price won't do it. Two independent lines of reasoning indicated this. The first was that the night is several times longer than the peak mismatch, so you need several times as many batteries to substitute for a natural gas plant that's running all night than to substitute for a peaker plant. The second was that in Houston, Texas, electricity prices during the peak mismatch are about three times higher on average than the typical prices. The declining price of batteries could take care of this too, but it would have to be a much bigger decline, by a ratio of 1/3.

But whether the price dropping by 20% or 66% are really so different depends on the rate of price decrease. Every time cumulative battery production doubles, battery price drops by about 20%. 20% is called the "learning rate", and this kind of relationship between price and cumulative production is called Wright's law. Note that it is not telling us how to extrapolate in time, but rather with cumulative production: the total amount of lithium ion battery capacity ever produced. By "capacity" I just mean that we're measuring how many batteries we've produced in energy units—a 1 kWh battery is 1kWh of battery capacity. The trend has more or less held from when battery capacity was being produced by the kWh for flip phones in the nineties to the present day when it's being produced by the MWh for grid energy storage.

Although Wright's law doesn't directly tell us how long it will take for prices to drop, it gives us a sense of the scale of the effort that it takes to reduce prices. "Doubling cumulative capacity" means building as much battery capacity as has ever been built. And that's what comes with a 20% price drop—not reliably and mechanically, but on average over the history of lithium ion batteries. If a prediction about the near future requires the price to go down more than that, then it may require multiple doublings. That means people building new factories, deploying new production technologies, and maybe bringing new battery chemistries to market. Considering the scale of the growth that we're talking about, Wright's law is not so mysterious.

If a prediction about the near future requires multiple doublings of battery capacity, are we really talking about the near future anymore? I don't want to precisely define "near future". I'd rather say: think about what else people might do while you're waiting for all those new battery factories and technological improvements. Or put another way, what other investments in R&D and capital might be made, on a similar scale. If battery prices have to drop to 1/3 of their current value to escape the peak adjustment niche, that would take about five doublings (since 0.8^5≈1/3). What other engineering efforts of a similar scale might people carry out?

I do think that multiple doublings of cumulative battery production will occur, and batteries will consequently—eventually—become quite cheap. In fact, even if battery energy storage for the grid completely stalls, electric cars would keep battery production going and battery prices dropping. (By the way, this is also why I expect battery energy storage systems to continue to use minor variants on automobile batteries.) Globally something like 3% of cars on the road are electric, a number which can double five times, since 0.03 * 2^5 ≈ 1. (That would only correspond exactly to doublings of cumulative battery production if all lithium ion battery capacity ever produced was in electric cars currently on the road). It's just important to keep in mind that when we talk about the price drop you would get from this many doublings, we're talking about technological transformations of the world on the order of cars going all electric. So it's important to consider what other technological transformations of similar magnitude may occur first.

This is why I'm holding on to my stock in a nuclear power company, Nuscale. Nuscale makes small modular reactors, a technology that has never been commercially successful and maybe never will be. Building the small modular reactor industry up from nothing would be a huge effort, but it's not necessarily on a larger scale than multiple doublings of cumulative battery production.

1 comments

Comments sorted by top scores.

comment by Archimedes · 2025-02-02T03:51:38.034Z · LW(p) · GW(p)

Batteries also help the efficiency of hybrid peaker plants by reducing idling and smoothing out ramp-up and ramp-down logistics.