Prediction markets are consistently underconfident. Why?

post by Sinclair Chen (sinclair-chen) · 2024-01-11T02:44:02.824Z · LW · GW · No commentsThis is a question post.

Contents

Answers 27 Unnamed 15 PeterMcCluskey 3 followthesilence None No comments

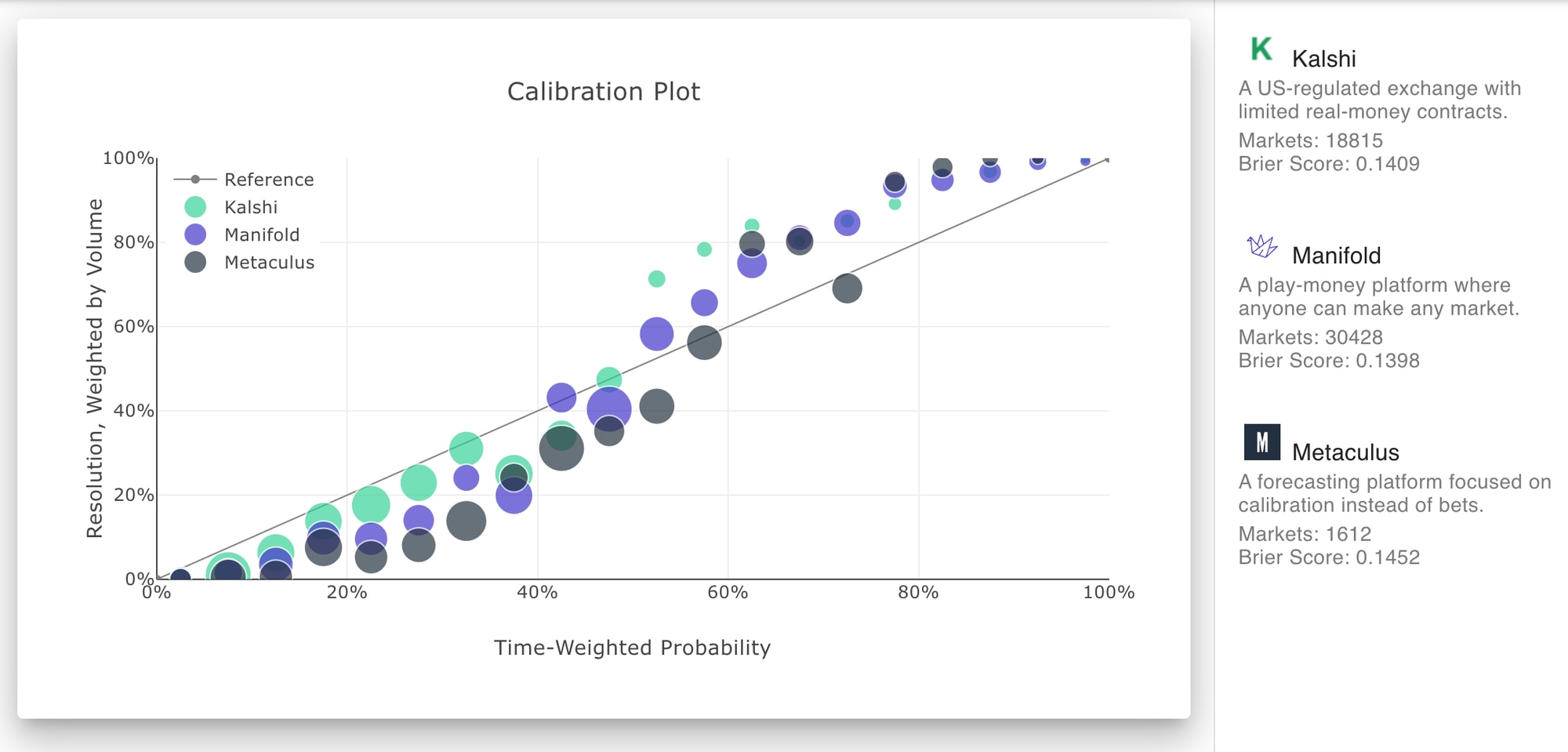

look at this calibration s-curve from calibration.city

markets are consistently closer to 50% than should be. why?

I have my own guesses but curious to hear yours.

Answers

What's "Time-Weighted Probability"? Is that just the average probability across the lifespan of the market? That's not a quantity which is supposed to be calibrated.

e.g., Imagine a simple market on a coin flip, where forecasts of p(heads) are made at two times: t1 before the flip and t2 after the flip is observed. In half of the cases, the market forecast is 50% at t1 and 100% at t2, for an average of 75%; in those cases the market always resolves True. The other half: 50% at t1, 0% at t2, avg of 25%, market resolves False. The market is underconfident if you take this average, but the market is perfectly calibrated at any specific time.

↑ comment by followthesilence · 2024-01-11T22:42:58.406Z · LW(p) · GW(p)

Exchanges require more capital to move the price closer to the extremes than to move it closer to 50%.

The Metaculus point scoring system incentivizes* middling predictions that would earn you points no matter the outcome (or at least provide upside in one direction with no point downside if you're wrong) so that would encourage participants with no opinion/knowledge on the matter to blindly predict in the middle.

Harder to explain with real money markets, but Peter's explanation is a good one. Also, for contracts closing several months or years out where the outcome is basically known, they will still trade at a discount to $0.99 because time value of money and opportunity cost of tying up capital in a contract that has very low prospective ROI.

*Haven't been on the site in a while but this was at least true as of a few months ago.

No comments

Comments sorted by top scores.