A quantitative introduction to churning

post by electroswing · 2021-06-28T22:21:09.028Z · LW · GW · 4 commentsContents

Disclaimer

The big picture

Really? 20%?

Is churning right for you? Common strategies & cost-benefit analysis

Strategy 0: Holding a credit card

Strategy 1: Holding a couple credit cards with good earn rates

Strategy 2: Simple churning

Strategy 3: Complex churning strategies

Why churning is hard

Banks have constraints on credit cards

Churning can lower your credit score

Psychological pressures

Don't spend more

Beware the sunk cost fallacy

Don't pay more to get more unless you actually want more

When to be cautious about using a credit card

When they're not accepted

When you don't want the vendor you're purchasing from to carry the fees

When what you're doing looks like fraud

Concrete suggestions for getting started

None

4 comments

Credit card companies offer sign up bonuses and other benefits to incentivize you to open a credit card with them. Churning is the art of going after these benefits systematically. It's surprisingly lucrative.

This post serves two purposes. One, I will describe common churning strategies. Two, I will do some rough cost-benefit analysis on these strategies so you can decide for yourself whether churning is worth it. Comments, critiques and corrections are welcome.

Disclaimer

- I am a knowledgeable, but not expert churner. Fact check me before making personal financial decisions. A good resource is /r/churning. This is not financial advice.

- This advice works best if you're in the US and have a decent credit score (or no credit history).

The big picture

Say you're planning on making a $1000 purchase.

One way to do this is with your debit card or cash. Spend $1000, get the $1000 item.

You can pay a bit less by using a credit card instead. For example, the Chase Freedom Unlimited offers 1.5% cash back on all purchases. You spend $1000, get the $1000 item, and get 1500 Ultimate Rewards Points which can be redeemed as a $15 statement credit.

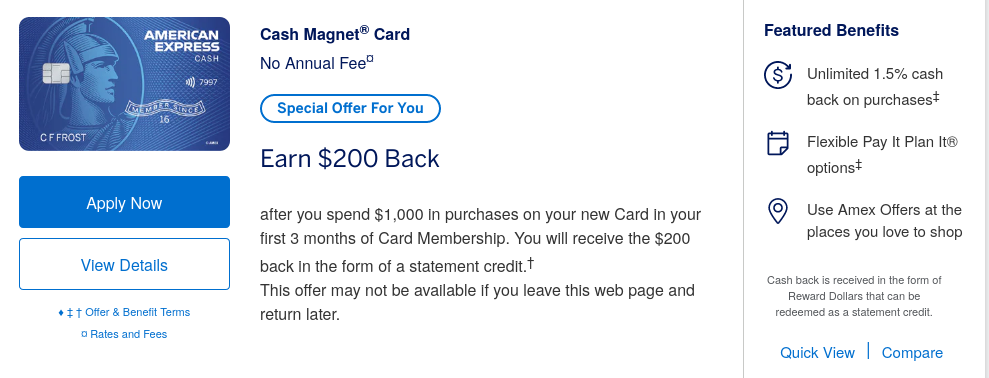

You can do even better by signing up for a new credit card. For example consider this American Express card:

So you can make the $1000 purchase and get an extra $200 from the signup bonus. All while paying no annual fee. (Yes, this card also earns 1.5% cash back, but you would have counterfactually earned this on a card like the Chase Freedom Unlimited so this isn't super relevant here.)

The Cash Magnet card isn't a once in a lifetime opportunity. There are dozens of stellar signup bonuses offered by various credit providers.

Effective churning is basically a 20% coupon on everything you purchase. The cost? A little time and a bit more attention to detail.

Really? 20%?

Yes, really. To estimate the benefit of churning, I've gone through the credit cards offered by Chase, American Express, Bank of America, Citi, Barclays, and US Bank. I kept track of each card's costs and benefits.

Costs:

- Minimum spend requirement (MSR): amount you need to spend on it in order to unlock the sign-up bonus.

- Annual fee (AF) for the first year.

Benefits:

- The sign-up bonus (SUB). This can come in the form of statement credits, credit card points, airline miles, and hotel points.

- Other relatively liquid benefits. Miles and points still count here, as well as statement credits for broad categories like travel, groceries, or dining. Other more nebulous benefits like "free checked bag", "free hotel room with restrictions", etc are not counted.

- Benefits are converted to dollars using conservative estimates. See the data sheet for details.

We can then calculate the "Effective Coupon %" of a card as follows:

(SUB + Other benefits - AF) / (MSR)

For example, take a card with a $3,000 minimum spend requirement, $95 annual fee, $500 sign-up bonus, and $300 in other benefits. Then (SUB + Other benefits - AF) = $705, meaning you get a net $705 in rewards by holding this card for a year. This corresponds to a $705/$3000 = 23.5% coupon on the $3000 item you planned to purchase.

Here are 5 data points (of 76 total), corresponding to the 0th, 25th, 50th, 75th, and 100th percentile values when the cards are ordered by Effective Coupon %.

| Coupon % | Issuer | Card name | MSR | AF | SUB | Other benefits |

| 0.13% | Citi | Prestige | $4,000 | $495 | $500 | $0 |

| 13.5% | Chase | United Quest | $5,000 | $250 | $800 | $125 |

| 20.0% | Chase | United Gateway | $1,000 | $0 | $200 | $0 |

| 30.0% | Chase | Disney Visa | $500 | $0 | $150 | $0 |

| 5010% | Barclays |

| $10 | $99 | $600 | $0 |

In particular, note that the median Effective Coupon % is 20% and the 25th-75th percentile range is 13.5%-30.0%. 42 cards out of the 76 I listed lie in this range.

All of the data collected can be found here (google sheets link).

Is churning right for you? Common strategies & cost-benefit analysis

These first few sections describe how holding credit cards can be beneficial, even if you don't churn. Later I go into more elaborate churning strategies.

For these estimates, I use the time valuation of $60/hr. If you value your time differently, change the conclusions accordingly. (If thinking about credit cards is fun for you, you might pick a substantially lower time valuation, or even $0/hr. I can attest to its enjoyability—it feels like a deck building game.)

Strategy 0: Holding a credit card

If you are over 18, do not have a credit card, and do not have a good reason not to have a credit card, you should probably get one. Cards with no annual fee and 1.5% cashback on all purchases include Chase Freedom Unlimited and Amex Cash Magnet Card. You may as well take the discount.

The cost to you is a credit card application—a quick form which asks for your basic information—and remembering to pay off your balance every month. I estimate costs of 1 minute per month and benefits of 1.5% back on living expenses. If you value your time at $60/hr, then 1 minute per month is worth $12 per year. If you were going to spend over $800 in a year on living expenses, then using a credit card is worth it.

Strategy 1: Holding a couple credit cards with good earn rates

You can do a bit better than 1.5% by holding a couple of no annual fee cards with better earn rates in specific categories. For example, the Amex Blue Cash Everyday Card gives 3% back on groceries. Chase Freedom Unlimited gives 3% back on dining and drugstore purchases. Chase Amazon Prime Rewards gives 5% back on Amazon purchases if you have prime. Discover's Cash Back Card offers a rotating 5% back in categories such as gas, restaurants, and grocery stores.

The cost to you is the time it takes to apply to a couple credit cards, the time it takes to pay off their balances every month, as well as the mental load to remember which cards have which earn rates in which categories. This is highly variable based on how organized you are and how good your memory is. I estimate costs of 5 minutes per month and benefits of 3% back on the aforementioned categories.

So when should you follow this strategy instead of the previous strategy (flat 1.5%)? You're spending 4 more minutes per month, so $48 of your time per year. So this strategy is only worthwhile if you're spending at least $3200 annually on these categories (grocery, dining, drugstore, gas, possibly more).

Because of this, optimizing for earn rates can end up being not a worthwhile use of your time. It may still be worthwhile if you enjoy this process (effectively valuing your time at a lower dollar value).

Strategy 2: Simple churning

From this section on, we will disregard earn rates of credit cards. (Note that some cards which are good to churn have earn rates substantially higher than 3 or 5%. For example, the Amex Platinum Card earns 10x points on groceries. So, it can be worthwhile to pay a little attention to earn rates on cards you're churning.)

Say you spend $5000 per year on living expenses such as food, travel, anything you buy without a credit card fee. The data from before shows that you can expect a median effective coupon of 20% when churning. So you would save 20% * $5000 = $1000 by churning.

What are the costs? The effective coupon % figures already account for annual fees, so we only need to factor in time. Say it takes 15 minutes / month to handle the logistics of deciding which cards to sign up for, applying for them, keeping track of the minimum spend requirements, closing / product changing cards with an annual fee after a year, and so on. This works out to 3 hours / year, or $180 of your time.

(Another cost, which I won't assign a dollar value to, includes the temporary hit to your credit score when you make a new inquiry. If you highly value a high and/or consistent credit score, this may affect the cost-benefit balance.)

Overall, the benefits of simple churning are 20% of the costs of your annual living expenses and the costs are $180. Often, this is worthwhile.

Note: even very simple churning will probably eventually involve cards with an annual fee. The strategy for these cards is to only pay one year's worth annual fee. When the second year rolls around, it's usually best to product change the card to a card with 0 annual fee, or ask for a retention offer.

Strategy 3: Complex churning strategies

Here is a quick and incomplete overview of more complex churning strategies.

- Bank bonus churning. Some banks give you $Y for opening a checking, savings, or brokerage account with $X and keeping the money there for a certain number of months. Sometimes these bonuses also have a direct deposit requirement. Often, the return on investment beats the stock market. This is a good option if you have a high paying job with a payroll department willing to split your paychecks across different banks.

- Making the most of points and miles. By paying careful attention to how much points and miles are worth in different contexts, you can often get far greater than 1 cent per point (1cpp), which is the estimate I've used in the analysis above.

- Paying rent, taxes, etc. with your credit card. Often there are 2-4% fees associated with paying rent or taxes using a credit card. However, since churning a new card gives you 20% back on your minimum spend requirement, paying these fees can be worthwhile.

- Business card churning. If you have a business (can be very small), you can open business cards for it. Business cards have lucrative sign-up bonuses and do not show up on your personal credit report, so they are desirable for advanced churners.

- Manufacture spending. Say you only have $5000 of living expenses per year, but you want to churn $10,000 worth of credit cards. You can "manufacture spend" the extra $5,000 by buying cash equivalents, for example Visa gift cards. It can be tricky to liquidate them. Some manufacture spending strategies violate credit card terms and conditions, so be careful and do research if you do this.

Why churning is hard

Banks have constraints on credit cards

Different banks allow you to open different numbers of credit cards over different time periods. One example is Chase's 5/24 rule: Chase will not approve your credit card application if you have applied for 5 credit cards (with any issuer) in the last 24 months. (If you want to keep Chase cards in your churning rotation, this effectively limits you to 2.5 cards per year.) Other banks have similar frequency restrictions.

Also, while it is possible to earn a bonus from the same card more than once (this is where the term "churning" comes from), most banks impose frequency restrictions. For example, you can only earn a bonus from a Citi card you've already earned a bonus from if you wait 24 months from opening or closing the card.

Churning can lower your credit score

Number of inquiries and average age of accounts are two factors which negatively impact credit score. Keep an eye on your credit score and make sure it stays in an acceptable range for your needs. Over time, it will increase, even if you churn a lot.

Psychological pressures

Credit card companies are not your friend. They take advantage of cognitive biases to make you make them more money (= spend more). Some specific points:

Don't spend more

If you're spending more money than you would have without churning, then you are a sucker. This is exactly what credit card companies want you to do.

Assuming you're not paying interest and your annual fees are covered by sign-up bonuses, they are trying to make money off of you via interchange fees, the 1-3% fees credit card companies charge merchants per transaction. They want you to think to yourself, "Wow, 5% back on dining? I should eat out more often!" Don't do it. You are only "earning" anything if you spend your money exactly as you would have if credit card rewards were not a thing.

Beware the sunk cost fallacy

Relatedly, beware of the sunk cost fallacy when considering whether to keep a card with an annual fee for more than a year. For example, suppose you have a Chase Sapphire Preferred ($95 annual fee), and you earned a $1000 sign-up bonus. Unless the card's benefits (not including sign-up bonus) are worth $95 to you, you should ditch the card after a year. It doesn't matter that the free $1000 could cover 10 years' worth of annual fee for the card.

Don't pay more to get more unless you actually want more

Here's a situation. You have a lot of airline miles from a sign-up bonus. You can redeem them for economy tickets at 1 cent per point (1cpp) or first class tickets at 2cpp. The first class tickets have the better redemption rate, but if they cost more points than the economy tickets, you're still spending more points. Think carefully about how much marginal utility you gain from first class vs economy, and whether paying more is worth it.

This applies to category-restricted statement credits as well. $10 back on UberEats sounds great until you realize that the UberEats fees for your order exceed $10. So again, you have to do a cost-benefit analysis.

When to be cautious about using a credit card

Putting purchases on a credit card in order to hit a minimum spend requirement is often the most efficient use of your money, but there are situations where you should not use a credit card.

When they're not accepted

This may be an obvious point, but when planning purchases, make sure your credit card is accepted by your desired merchant. In particular, Amex often isn't accepted outside of the US.

When you don't want the vendor you're purchasing from to carry the fees

See this LessWrong post. [LW · GW] If you donate to a charity using a credit card, your $1000 donation might be more like a $980 donation after interchange fees. So, if your intent is to donate $1000, you may need to pay more like $1020. (This $20 inefficiency can still be worthwhile if you are aiming to hit a minimum spend requirement.)

When what you're doing looks like fraud

This can happen with various manufacture spend techniques.

This can also happen if you pay off your balance multiple times in the month in order to avoid hitting your credit limit.

Credit card company algorithms are inscrutable, so if you plan to engage in abnormal purchasing patterns, do careful research and make sure you're taking on an acceptable amount of risk.

Concrete suggestions for getting started

If you are new to credit cards and want a gentle start, consider a card with no annual fee, decent earn rates, and some sort of sign-up bonus. Some examples are the Chase Freedom Unlimited and Amex Cash Magnet cards. This way, you can earn a bit of a sign-up bonus, get used to paying off your monthly balance, and build credit, paving the way for the possibility of churning later.

If you have a few basic credit cards, it's common to go after premium Chase products next (due to the 5/24 rule), one example being the Chase Sapphire Preferred ($95 annual fee for $1000 sign-up bonus). If you travel a lot, you may want to look into cards which give you airline miles or hotel points.

If you already have a lot of credit cards and need to wait until you can apply for more, you can explore other churning mechanisms such as bank bonus churning.

For more information, check out /r/churning or doctorofcredit.

4 comments

Comments sorted by top scores.

comment by Viliam · 2021-06-29T00:38:11.912Z · LW(p) · GW(p)

I estimate costs of 1 minute per month and benefits of 1.5% back on living expenses. If you value your time at $60/hr, then 1 minute per month is worth $12 per year. If you were going to spend over $800 in a year on living expenses, then using a credit card is worth it.

What are the costs of making a mistake? Suppose your plan is to spend 1 minute per month doing the credit card magic, but when the day comes, you forget, or you are on a hike in a forest with no internet signal, or your internet provider has an outage... Would making two or three mistakes a year eliminate the profits?

Replies from: electroswing↑ comment by electroswing · 2021-06-29T02:35:06.421Z · LW(p) · GW(p)

I think the obvious answer here is AutoPay -- this should hedge against situations you are describing.

The costs of making a mistake are certainly high, since it's a permanent hit to your credit report. I am not super knowledgeable of how late payments affect credit score (other than that it has a negative sign), this is an interesting question.

Replies from: korin43↑ comment by Brendan Long (korin43) · 2021-07-02T17:51:12.976Z · LW(p) · GW(p)

It's not permanent. Late payments stay on your credit report for up to 7 years, but they have very little effect after a year or two (assuming it's a one-time thing). There are also ways to get late payments removed from a credit report, especially if you pay the bill as as soon as possible after realizing it's late.

https://www.creditkarma.com/credit-cards/i/how-long-do-late-payments-stay-on-credit-report

I agree that anyone using a credit card should have autopay enabled though.

comment by benjaminikuta · 2021-06-29T01:46:22.146Z · LW(p) · GW(p)

Your base level no fee cash back card should be 2%, not 1.5%. Citi and Fidelity have cards that are examples.

Regarding the algorithms for things that look like fraud: https://www.reddit.com/r/CreditCards/comments/hze1ir/do_not_do_this_if_you_want_your_credit_card_to/