Information Markets 2: Optimally Shaped Reward Bets

post by eva_ · 2022-11-03T11:08:49.126Z · LW · GW · 0 commentsContents

Aligned Incentives Reshaping Interests Example on a Binary Problem For a Continuous Target No Price Explosion at Certainty Shareable Evidence None No comments

Sequel to Information Markets [LW · GW], which contains a long text outline of what I consider to be the correct alternative to Prediction Markets [? · GW], which I don't like for a long list of reasons.

This post is intended to fill in the gap in the original regarding what an ideally shaped bet to prove a belief to someone wanting to buy true information efficiently actually looks like.

Aligned Incentives

Suppose the seller has Utilityfunction , and the community . Without the sellers information, the market will believe distribution , and so make decision . With the sellers information added, the market will believe distribution , and so make decision .

For the seller to have aligned incentives, we need:

(if the info is true, you should share it)

(if the info is false, you shouldn't share it).

The difference between these two define a Bias for or against telling the truth, and which may need to be overcome to convince them to share honestly. For now, we assume an unbiased source has no difference in Utility depending on the markets decision, and so that complexity can be skipped over. They can still hava a difference in utility in terms of the effort of the cost of making the claim, or the reward the market offers for telling it information, and we can give them shaped incentives with an Optimally Shaped Bet.

Reshaping Interests

To motivate a seller to communicate information, we want to offer them in profit for telling us X, if it's actually true. If it's False, we want a loss sufficient to pay someone for correcting it back:

adding no information gives no payout

a wrong bet must lose enough to correct it back

a correct bet gives you expected profit

For our function to be optimal, we need that the seller who believes is best off buying a bet that communicates their sincere beliefs, meaning that:

We also want to minimise risk, if it is true information, because excessive risk becomes a transactional cost, subject to above constraints:

Whats the chance this is sufficient to exactly pin down our mystery functions Bet, at least up to a constant factor of how much subsidy is offered?

Which implies an expected reward matches the gain in Shannon Information:

and for false information you make exactly enough of a loss to pay the person who corrects it back.

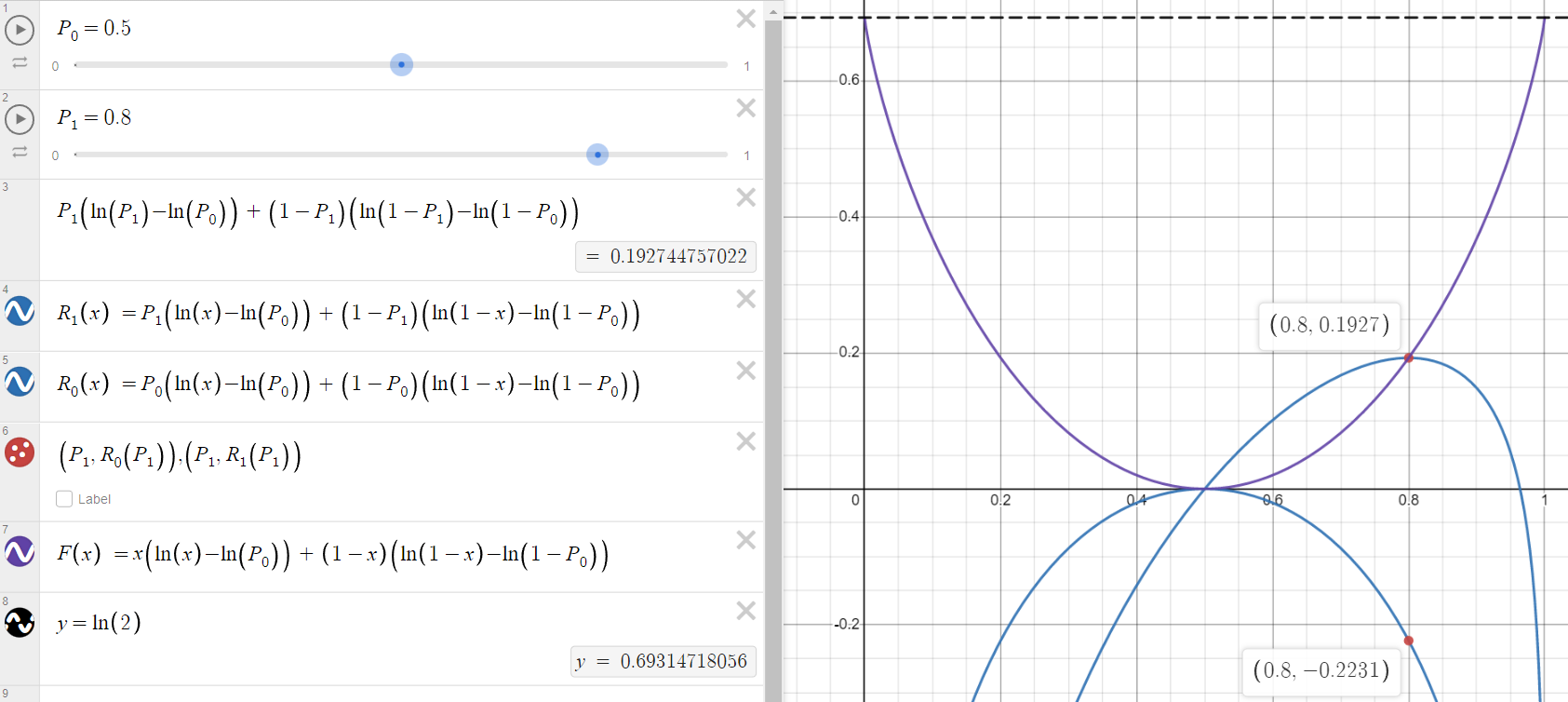

Example on a Binary Problem

Suppose the market currently believes a future binary observable has p=0.5 chance of occuring. If you sincerely believe that p=0.8, you can make a bet which moves the market to 0.8 and pays as below. You get maximum expected return by betting your true belief, while making enough expected to loss to pay the person who corrects it back if you bet without information. In total if the market moves to certainty it only has to pay out ln(2) arbitrary value units, but this can be much higher for markets with more possible outcomes with lower prior chance.

For a Continuous Target

Since the subsidiser wants a constant upper bound on payout offered, and a prior that fits its actual beliefs (otherwise it'd just immediately bet in its own market), it divides the target probability distribution into equally probable buckets (under its prior), and then offers bets with payout dependent only on the probability assigned to the winning bucket. This can be used to escape any continuity targets, and leaves the subsidiser out to pay at most units which it can scale arbitrarily as it wants.

No Price Explosion at Certainty

If a question resolves, and a specific once expected to have of occuring in fact occurs, then someone who managed to deduce that before the subsidy deadline gets a profit of exactly. On the other hand, in order to actually back up their "It's 100% x" claim, they need to be willing to stake infinite capital that none of the other outcomes will happen, which mortal traders don't typically have. This gives a de facto upper bound on how confident market participants are allowed to be. While the subsidiser only pays finite In the other direction, if the market closes with strong belief in the wrong direction, the subsidier makes a profit as compensation for getting bad predictions.

Shareable Evidence

Sellers who have unfakeable or expensive-to-fake information might want to profit from selling it without the effort or risk of making a calibrated bet. If you show your proof to multiple traders, they'd be willing to bid up to some fraction of their expected profit or the cost-to-fake in cash to buy the right to use the information. They wont offer this for unprovable information because then they'd be swamped by people trying to sell fake information who aren't willing to place a confidence-proving bet themselves.

In a competitive market with many buyers, you should expect provable information to pay out close to the that it moves the market by without the seller having to take on the risk of the bet themselves.

0 comments

Comments sorted by top scores.