Money-generating environments vs. wealth-building environments (or "my thoughts on the stock market")

post by Nicole Dieker (nicole-dieker) · 2022-02-04T17:37:33.612Z · LW · GW · 9 commentsContents

9 comments

Very interested in whether you think I'm right; also interested in the ways you think I'm wrong.

This post is going to include a discussion of the stock market, which means that I am obligated to begin with a statement that you should not take any of this as investment advice.

The real question is whether I will.

Sooooo about a month ago I told you all [ON MY BLOG, WHERE THIS IS CROSSPOSTED FROM] that I wanted to write about money-generating environments vs. wealth-building environments, with the primary distinction between the two defined as follows:

- Money-generating environments are controlled by someone else (and the value that they are willing to release into the environment).

- Wealth-building environments are controlled by you (and the value you bring to the environment).

If you’re writing for a content site that offers defined jobs at a preset value per job, you’re working within a money-generating environment.

If you’re writing for clients who are reaching out to you based on your expertise and are giving you the opportunity to either name or negotiate your rate, you’re working within a wealth-building environment.

It’s worth noting that the latter environment has an upper bound; if someone asked me to write a 1,200-word article about how to choose a CPA, for example, and I said I’d only do it for $2 a word, they’d probably go find someone else.

But it’s also worth noting that in a wealth-building environment, the wealth that you’re building goes beyond money. You’re also building your reputation, your network, your portfolio, and so on.

Plus, you’re building a level of expertise that you will be unlikely to get if you only write low-paying content site stuff. When I was giving a presentation on freelancing to grad students at Texas Tech earlier this week, for example, I explained to the students that when the CARES Act was released in 2020, I read the entire thing — and was able to use my knowledge of what was actually in the CARES Act (in combination with the financial knowledge I already had in my toolkit) to pitch high-value work.

I created value for readers by being able to provide a professional-level analysis of a document I had actually taken the time to read.

I created value for clients by giving them the kind of article that attracted readers who were looking for specific information about the CARES Act.

I created value for myself by building a reputation as the kind of writer who would read a primary source in full before offering commentary or insight.

I also earned money.

What does any of this have to do with the stock market?

I’m going to argue — perhaps successfully — that the stock market is a money-generating environment that we mistakenly treat as a wealth-building environment.

And then I’m going to argue — while reminding all of you that I am not an investment professional, I’m just a person who reads a lot of primary sources — that we should enter the stock market with a win condition in mind.

And then, once our win condition is achieved, we should get out of the market and pay our taxes.

See, I can’t stop thinking about the GameStop investors.

They bought.

They held.

The stock went up — ridiculously (though not unpredictably) up.

Then it went down again.

There was an article in the NYT last week with the headline “Buy GameStop, Fight Injustice. Just Don’t Sell.” It highlighted the foolishness of the buy-and-hold position that much of the GameStop crowd is still valiantly maintaining (“buy-and-hold” being the kind of tactic that applies better to index funds than to individual stocks), while noting that the people who sold their shares as GME peaked actually generated a little money.

And then it got me thinking about how the numbers we see, when we log in to our Vanguard accounts or whatever, don’t represent actual money. They represent the value of our investments. Before we can redeem that value — and those are Vanguard’s words, not mine — we have to sell.

Obviously I’m also thinking about our recent market dip, although I agree with Helaine Olen’s assessment:

If, like half of all individual investors, you simply placed money in an index fund that replicates the broader stock market, you shouldn’t feel shaky. That’s because the S&P 500, for all the recent declines, was, at the close of the market Friday, still as high as it was in mid-October. If you felt satisfied with your portfolio then — and chances are pretty good you did — you should be happy now.

What does “happy” mean, though? Are you happy that the numbers were higher in October 2021 than they were in September 2021? You didn’t actually gain anything, except the opportunity to feel “sad” when the numbers started going down again.

If you were in fact happy with your portfolio in October 2021, why didn’t you redeem your shares, collect the money, and pay the taxes?

Because — and come on, we all know this — you weren’t really happy.

You wanted more.

At this point you’re going to say “ahh Nicole but but but but but I’m not 65 yet.”

Okay.

Let’s say that the majority (or the entirety) of your investments are held within retirement accounts — your IRAs, your 401(k)s, and the like.

You probably already know that you can’t withdraw money from those accounts until you turn 59 1/2, unless you want to pay both penalties and taxes on the money you withdraw (and yes, I know Roth IRA withdrawals are different, don’t @ me).

But that doesn’t mean you have to keep whatever mutual fund(s) you’re currently holding for the next 30 years.

You can set both a win condition and a minimum loss condition for the investments in your retirement accounts.

Then, when either of those conditions are achieved, you can redeem the value of your investments.

Unfortunately, there’s no fully-guaranteed way for you to keep that value until you retire. As far as I understand, money in a retirement account must be invested in something. Money market accounts, municipal bond accounts, and Treasury bond accounts appear to be the most secure options — but each of those still carries the possibility of loss.

And now you’re going to say “but inflation.”

Yes. The idea is that if you don’t buy and hold until you’re at least 59 1/2, you won’t be able to take advantage of the 6% average annual market growth — although that percentage is highly speculative (pun intended) — and much of the value of your accumulated cash will be lost to inflation.

Wellllllll if the market drops right before you retire, much of the value of your accumulated investments will be lost as well, soooooo yeah.

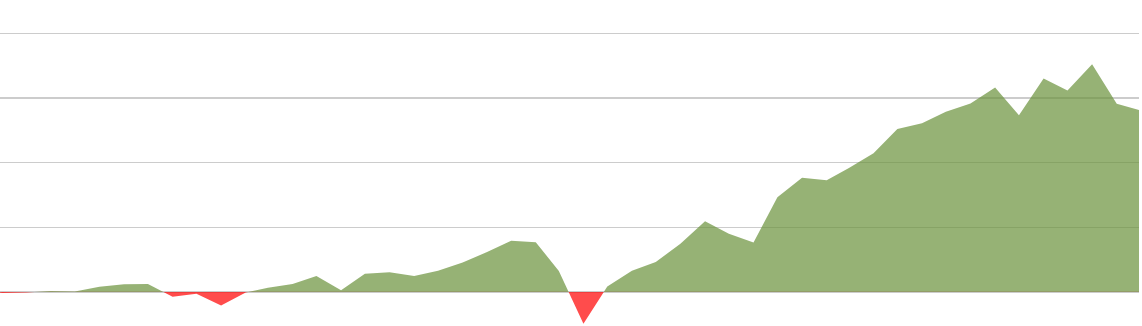

UPDATE: I thought about this a little more carefully, and the only way that your portfolio could lose so much value that it would be worse than “having stuck the money under a mattress” would be if you lost all of your accumulated market returns and dropped back to principal — or if the market lost so much money that you dropped below principal.

Which, if you take a look at the chart below, has happened! More than once! In my own investing history!

Yes, it bounced back. Yes, it has always bounced back so far (although the bounce generally takes years and occasionally decades to complete).

But it does happen.

And now you’re going to say, if you want to say it, “but if it weren’t for the possibility of increasing my cash reserves through long-term investment in the stock market, I wouldn’t be able to retire; I’m just not earning enough money from my current employment to do it any other way.”

Which brings me back to money-generating environments vs. wealth-building environments.

I don’t want to be the kind of person who stares at you through a browser window and says do whatever you can to get into a wealth-building environment, it is the most important thing you can do for your long-term financial security, because that sounds remarkably close to “pull yourself up by your bootstraps.” If wealth-building environments were prevalent and plentiful, we’d all be pulling ourselves into them.

Frankly, I’m not even sure I’m in a true wealth-building environment myself. I’m close, in the sense that every freelance assignment I complete and every class I teach increases my value and my clients’ values on multiple vertices (vs. every assignment I complete increasing an employer’s value or a content mill’s value without simultaneously increasing my own), but the dollar amount associated with that value is not determined by me (though I can negotiate it).

So I’ll say this, instead: money-generating environments may come with both limits and risks, but that doesn’t mean you shouldn’t try to pull as much money out of them as possible.

And then you’ll say “but you didn’t answer my question about how to save up enough money to retire.”

And then I’ll say “well, I’m about to.”

Before you invest in anything — an index fund, a career, an educational program, maybe even a partner — it’s a good idea to define both a WIN CONDITION and a MINIMUM LOSS CONDITION.

Both WIN and MINIMUM LOSS prompt a NEXT ACTION.

In the case of the stock market, WIN and MINIMUM LOSS both prompt sell.

What about leaving money on the table? Well, what you’re leaving on the table is risk. If you have the money you need, walk away and pay your taxes.

If you don’t have the money you need, let your investments continue to accumulate value until you hit WIN or MINIMUM LOSS — and continue running this program on other aspects of your life, like your budget and your career and your skillset, so you can generate as much money as possible out of various money-generating environments.

If you’re doing the math and thinking “with my income and my debt and my various financial responsibilities, I’ll never have the money I need,” then you can ask yourself whether you want to redefine retirement to include paid employment (which most of us are going to end up doing, including me) as well as what you want to do this year to generate more value (which can include money, skills, relationships, and so on, and remember that your value increases as you provide value to others). You can critical path it, if you want, and set up an action tree with various sets of WIN, MINIMUM LOSS, and NEXT ACTION.

THIS, BY THE WAY,

IS VERY HARD.

MOST SYSTEMS ARE NOT SET UP FOR US TO GAIN MORE VALUE THAN WE GIVE.

BUT WE CAN SET UP OUR OWN VALUE SYSTEM

AND THEN LIVE ACCORDING TO THOSE VALUES.

The real question, as I set out at the beginning of this post, is whether I will be brave enough to take my own advice.

To pull out of the market when my investments can be redeemed for an amount of money I’m happy with, which is likely to happen soon enough that I’m actually thinking about doing it.

Yes, taxes — but there are always taxes, and I’ve factored them into my happy number.

Yes, I’m potentially leaving money on the table — but I’m also leaving risk on the table.

If I want more money in the future, I can buy into the market, set my WIN and MINIMUM LOSS, and sell accordingly.

I’ll have a net worth that is as close to mine as possible (minus the amount that has to remain in money market or bond accounts until I’m 59 1/2), instead of investments that can only be worth what someone else is willing to trade for them.

And yet when I write that, I start asking myself “but what is a dollar if not an investment that is only worth what someone else is willing to trade for it” and then “wait, what if a stock is a better investment than a dollar” and then “no no no no no investing on top of investing is like double risk” and this is where you should rightfully say I should never take Nicole’s stock market advice because she is not an investment professional.

Which is exactly what I told you at the beginning of all of this.

If and when I sell, I’ll let you know. ❤️

9 comments

Comments sorted by top scores.

comment by 25Hour (aaron-kaufman) · 2022-02-04T21:23:03.089Z · LW(p) · GW(p)

I'd like to see the intuition expanded upon here:

And yet when I write that, I start asking myself “but what is a dollar if not an investment that is only worth what someone else is willing to trade for it” and then “wait, what if a stock is a better investment than a dollar” and then “no no no no no investing on top of investing is like double risk”

Is it double risk? We're going from a situation where we're talking to a widget producer and saying "yes I would like to exchange a dollar for a widget" to a situation where we're saying "I would like to exchange a fractional share of Microsoft for a widget." Seems basically analogous.

Now, obviously in our society all transactions are denominated in dollars, and you have to do the conversion to dollars beforehand because no retailer is actually able to accept shares-of-stock at the counter, but the fact that purchases have to be converted to dollars beforehand doesn't imply you're taking on the risk of that currency increasing or decreasing in value if you don't hold any of it at baseline.

And I guess if you accept this, the question is what defines a "better" or "worse" investment. It sounds like you're making an assessment that trading risk for money is fundamentally not worthwhile above a certain savings amount; I suppose that's fair; it just means that to maintain a specific retirement withdrawal rate you have to have a bunch more money saved up pre-retirement (in expectation) than someone who doesn't, though having done that you also face less risk of ruin from the stock market crashing.

I'm wondering if that mindset can be trivially extended to "but actually the really foolproof asset is freeze-dried meals, since 1 meal=1 meal, as opposed to one dollar which could equal any number of fractional meals in the future".

Replies from: nicole-dieker↑ comment by Nicole Dieker (nicole-dieker) · 2022-02-04T22:01:09.224Z · LW(p) · GW(p)

That paragraph was meant to be less intuitive and more "wait if you really follow this line of thought it takes you to some nonsensical arenas..."

But we don't get to say "I'd like to exchange a fractional share of Microsoft for a widget." You can only exchange a fractional share of Microsoft for A) cash or B) shares in something else, and you can only do so if someone else is willing to make the trade. There are situations in which you could have an asset you want to sell and nobody wants to buy it, which is also true for other assets like houses (and, if you own a business, whatever your business produces [and, if you are a worker with specific skills, the value those skills could bring to an employer]).

As to your last point, there's a non-trivial reason why some people suggest stockpiling a year's worth of food...

comment by Nicole Dieker (nicole-dieker) · 2022-02-04T17:42:09.519Z · LW(p) · GW(p)

One note that I wanted to add as we begin the discussion: in the hour it took me to write this post yesterday afternoon, Facebook stock had the largest one-day value drop in the market's history.

This is what appears to have happened:

- Facebook announced that it was losing users

- Bots (it's bots, right?) interpreted this news as "Facebook is going to lose value, better sell my shares while they are still high value"

- Bots (right?) sold shares (to whom?)

- Share value declined

All of the money-making value was redeemed before people like you and me even had a chance to trade. Right?

Replies from: aaron-kaufman, SimonM↑ comment by 25Hour (aaron-kaufman) · 2022-02-04T21:36:44.962Z · LW(p) · GW(p)

I think you're totally right that to the extent that the stock market is a zero-sum game retail traders will lose almost every time, since the big players on the other end will always have more information and power to leverage that information than retail.

I think a lot of the relevance of this comment depends on your view of stock-market-as-casino vs stock-market-as-generator-of-wealth-at-several-steps-removed. I take the view that it's mostly the latter; widget maker IPOs, accepts money from big institutional IPO investor and buys capital with it in exchange for proceeds, IPO investor (effectively after several intermediate trades) sells that share of proceeds-generated-from-capital to retail trader. The capital is still doing stuff for people! It's just exactly what it's doing is totally opaque to almost everyone.

Replies from: nicole-dieker↑ comment by Nicole Dieker (nicole-dieker) · 2022-02-04T22:02:06.175Z · LW(p) · GW(p)

agreed agreed agreed

but hey guess what the market rebounded today so yay for that?

↑ comment by SimonM · 2022-02-05T15:43:10.502Z · LW(p) · GW(p)

I don't know enough about how equities trade during earnings, but I do know a little about how some other products trade during data releases and while people are speaking.

In general, the vast, vast, vast majority of liquidity is withdrawn from the market before the release. There will be a few stale orders people have left by accident + a few orders left in at levels deemed ridiculously unlikely. As soon as the data is released, the fastest players will general send quotes making a (fairly wide market) around their estimate of the fair price. Over time (and here we're still talking very fast) more players will come in, firming up that new market.

The absolute level of money which is being made during this period is relatively small. It's not like the first person to see the report gets to trade at the old price, they get to trade with any stale orders - the market just reprices with very little trading volume.

All of the money-making value was redeemed before people like you and me even had a chance to trade. Right?

Correct, you absolutely did not have the chance to be involved in this trade unless you work at one of a handful of firms which have spent 9 figure sums on doing this really, really well.

comment by [deleted] · 2022-02-05T12:48:43.657Z · LW(p) · GW(p)

This post is going to include a discussion of the stock market, which means that I am obligated to begin with a statement that you should not take any of this as investment advice.

and this is where you should rightfully say I should never take Nicole’s stock market advice because she is not an investment professional.

I'm curious as to why you feel the need for such disclaimers. Are you afraid of legal consequences, or do you think the disclaimer will genuinely help some people, or both/something else?

Replies from: nicole-dieker↑ comment by Nicole Dieker (nicole-dieker) · 2022-02-05T14:17:18.405Z · LW(p) · GW(p)

It's both a CYA and a joke. Anyone who says anything about the stock market online begins with the statement that "this should not be constituted as investment advice," e.g. here and here (two examples pulled from top of google search).

There is assumedly a legal reason that this disclaimer came into practice, e.g. if I wrote something and you did it and you lost money you might sue me, so I am obliged to tell you that A) I am not giving you advice and B) you should not take it!

Replies from: None↑ comment by [deleted] · 2022-02-05T14:55:25.897Z · LW(p) · GW(p)

Anyone who says anything about the stock market online begins with the statement that "this should not be constituted as investment advice

...which is why I thought it would be much funnier if someone wrote "Everything I'm about to say constitutes official investment advice" on their econblog posts or "We don't care about your privacy" on cookie disclaimers and having most people misread it as the regular stuff. I'm surprised nobody is doing this, considering the low legal risk provided by online anonymity.