Post-crash market efficiency 1696-2020

post by bfinn · 2020-05-22T14:13:50.903Z · LW · GW · 8 commentsContents

UK crashes US crashes None 8 comments

WHAT DO past stock market crashes tell us about the weak-form Efficient-Market Hypothesis? In a meltdown, do prices become more predictable?

In theory, they instantly adjust to all public information. Hence technical analysis – predicting future stock prices from patterns in past ones – should not work. In particular, there should be no usable trends – tendency for prices to keep moving up or down – nor predictable reversals.

On the other hand, big crashes are so rare and extreme that they might be exceptions. In a crisis, perhaps enough traders act impulsively, or at least do something unusual, that there's a smidgeon of predictability. Surely greed and fear don’t always exactly cancel out?

So let’s take a look. Do big crashes on average produce any kind of pattern or trend in prices?

I’ll consider all major meltdowns that have ever happened in the US and UK, using their broad indices, the S&P 500 and FTSE All-Share; and defining a crash as a fall of 20% or more within 8 weeks.

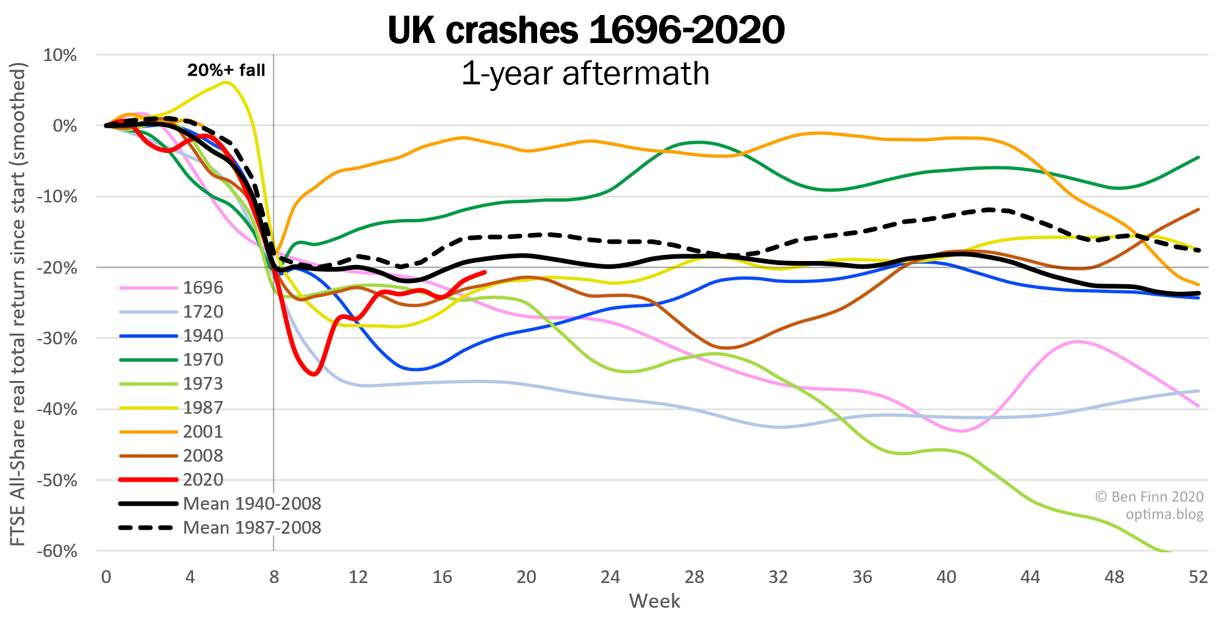

UK crashes

Starting with the UK (as its stock market began first), here are all crashes throughout history:

Each coloured line is a crash – starting with a 20% fall – and its aftermath. I’ve even included the Bank of England crisis of 1696, and the still-famous South Sea Bubble of exactly 300 years ago (which coined the term ‘bubble’), though both are omitted from the averages. Thereafter, despite slides and slumps, there were no more actual crashes until World War 2, after which they became more frequent.

The red line is the current crash, from mid-January up to this week. The FTSE fell further, faster, than ever before, then has partly recovered; though this may yet turn into a dead cat bounce.

Superficially, all these crashes have little in common: caused by speculation, oil, program trading, terrorism, disease; all kinds of shapes – L, V, U, W; they fall 20% or 70%, take days or years to hit rock bottom, and up to a decade to recover. Like spaghetti, the lines are all over the place.

But to find an underlying pattern of sorts, we can simply take an average: the solid black line shows the mean of all crashes over the past century. And after the initial drop, it’s basically flat for the rest of the year. On average, the market didn’t under- or over-react: prices neither kept falling, nor bounced or recovered. There is no sign of any trend. So the fact that there has been a crash predicts nothing about whether stocks will go up or down, either days or months later; not even by a few percent.

This consistency is surprising. Not least as half these crashes pre-date computers, so there was no algo trading, far less data and number-crunching, and vast scope for biases and iffy strategies.

If we exclude those bad old days, and average the three crashes of the computer era – 1987, 2001 and 2008 – the picture stays much the same (see dashed black line). In week 8, you may as well toss a coin to decide whether to buy or sell; for by year end, prices will be almost unchanged. And if it looks like you could make a few percent by week 42, consider the huge variation between these crashes, with high volatility: your risk-adjusted return would be mediocre.

Of course, this does not prove that the Efficient-Market Hypothesis holds for crashes. We are looking at the whole UK stock market, not individual shares, which may still have mispricings – though perhaps too small, rare, or erratic to make much money from. And we are only considering price history, not other information that might matter (e.g. news of a virus). Once the market has fallen 20%, everyone knows why; but earlier on, traders may not see the storm clouds forming.

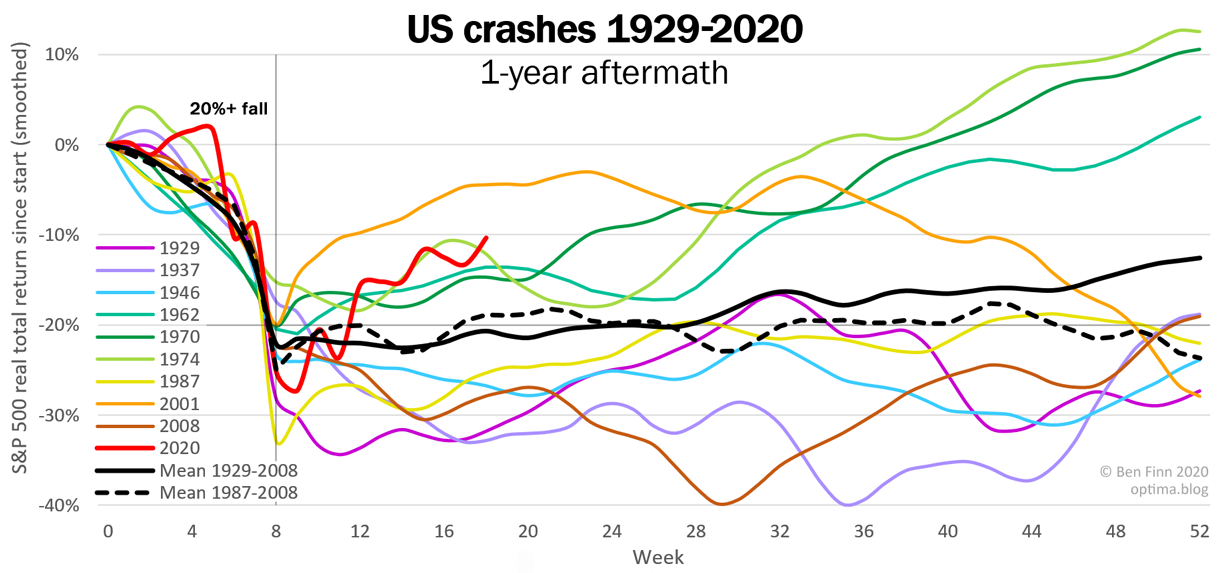

US crashes

Across the pond, stock trading didn’t get going until the 19th century. The first meltdown was the famous one, the Wall Street Crash of 1929. This was followed by others, about one per decade – increasingly in sync with UK crashes, due to globalization:

This is similar to, but not quite the same as, the UK chart. For the solid black line shows a gradual rise through the year, somewhat faster than usual (which is 6.6% p.a. for this index). But again, there are probably no excess returns once you adjust for risk. And in any case, the dashed black line suggests that this slope was steamrollered by the advent of computers.

There’s a bit of a post-crash bounce in the dashed line, but this looks unlikely to be a real effect as it wasn’t there before 1987, and is similar to random meanderings in later months.

So, past US and UK meltdowns seem to confirm the Efficient-Market Hypothesis. Like a goldfish bumping into the side of its bowl, indices instantly forget they’ve crashed, and just carry on as normal.

P.S. Though things behave differently after a year - which I've since written up here [LW · GW].)

8 comments

Comments sorted by top scores.

comment by Dagon · 2020-05-22T15:06:40.372Z · LW(p) · GW(p)

Note that the indices you're tracking are _already_ giant averages. I would love to see an analysis of how crashes change the composition of the indices, and whether there's any predictability in sector or individual big winners and losers.

I want to think that a crash is a fragility sieve, which accelerates the creative destruction of capitalism. Over-leveraged companies, and those very dependent on whimsy and excess take a bigger hit than those with depth of assets and a solid value chain to a durable market. And I suspect that's not how it actually works - companies big enough to measure this way are simply too complex for those stories to apply.

Replies from: bfinn↑ comment by bfinn · 2020-05-22T20:27:30.176Z · LW(p) · GW(p)

Indeed this analysis would be interesting, though I don't know if long-term enough data (e.g. a century's worth) is available in this level of detail.

I assume there might indeed be clearer patterns in how individual companies' prices react, perhaps depending on their size and liquidity. Though again I expect most, if not all, of any predictability has disappeared in recent decades.

comment by alexf01 · 2020-05-23T12:53:39.682Z · LW(p) · GW(p)

Comparing the crashes before and after the end of the bretton woods agreement 1971 should not be done. Those are to separate currencies, they had still the same name "USD" but the attributes changed dramatically and this gave the FED much more tools during market crashes.

E.g. its simpler to reflate the stock prices if the FED just issues trillions of $ and ignores CPI and Asset price inflation. That was not so easy in currency system that was Gold backed.

This site gathers some of the economic data that got skewed after the currency system change.

https://wtfhappenedin1971.com/

Replies from: bfinn↑ comment by bfinn · 2020-05-23T15:08:48.252Z · LW(p) · GW(p)

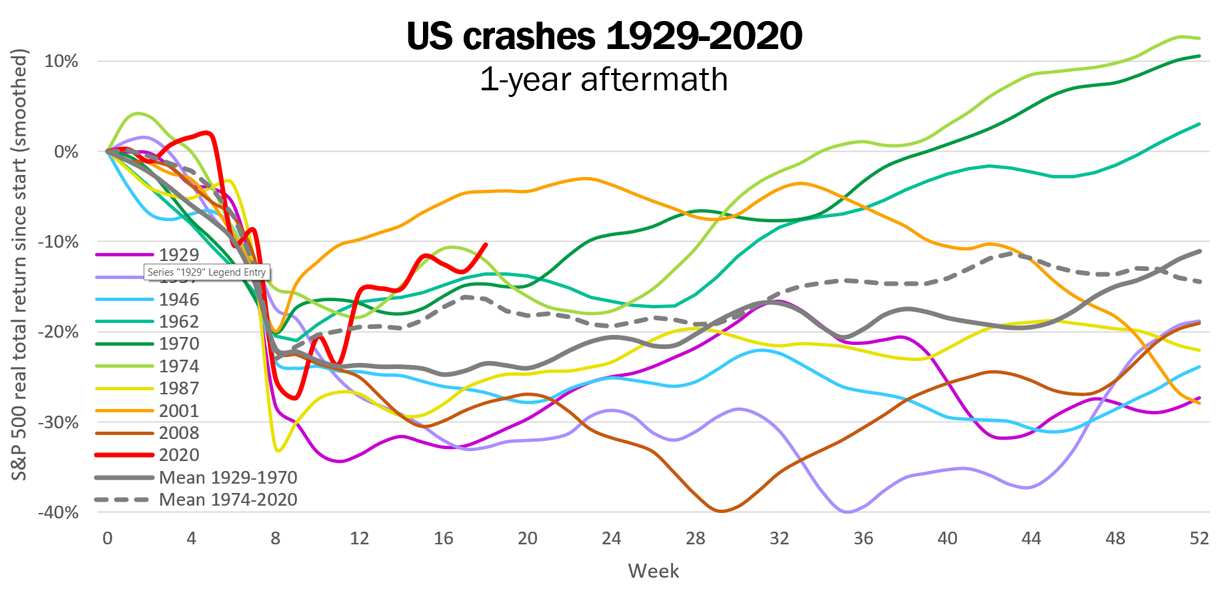

OK, well out of interest I've just done you a chart with grey lines averaging crashes before & after Bretton Woods. ('After' includes 2020 on this one.)

https://i.postimg.cc/wMgs7Jn0/Bretton.png

{kind=link}

Not sure whether the difference is significant. The post-Bretton (dashed) line shows a bounce back for the first few weeks, but by year end they're much the same.

comment by johnswentworth · 2020-05-23T02:00:44.792Z · LW(p) · GW(p)

Where did you get the data for this? I'm particularly impressed with the older price series, I imagine that must have come from specialized sources...

Replies from: bfinn↑ comment by bfinn · 2020-05-23T12:01:36.054Z · LW(p) · GW(p)

UK from Global Financial Data (paid), US from Yahoo Finance (free).

Global Financial Data now provide *daily* FTSE 100 data from 1692 - remarkable. (The 1696 & 1720 lines above were from their earlier monthly data.)

Replies from: gwern↑ comment by gwern · 2020-05-25T20:56:12.386Z · LW(p) · GW(p)

Is the FTSE data here based on commodities? I was surprised it went so far back, and it seems to derive from the London Stock Exchange, but WP says

At that coffee house, a broker named John Castaing started listing the prices of a few commodities, such as salt, coal, and paper, and exchange rates in 1698. Originally, this was not a daily list and was only published a few days of the week.[6]

If he was only listing commodities in 1698, then what is being indexed years before in 1692 for the crash?

Replies from: bfinn↑ comment by bfinn · 2020-05-25T22:22:01.881Z · LW(p) · GW(p)

There were I believe only three major equities being traded back then - Bank of England, and a couple of others (can't recall - East India Company maybe), plus the South Sea Company soon after. The stock market continued to consist of a smallish number of large monopoly companies until the 19th century, when many more companies were listed.