A Strange ACH Corner Case

post by jefftk (jkaufman) · 2024-02-10T03:00:05.930Z · LW · GW · 2 commentsContents

2 comments

It turns out ACH transactions can fail because your bank has too many people out for the holidays. Which isn't great if you're trying to get your donation in before the end of the year!

Juila and I were a bit late in deciding where we wanted to donate this year. We intended to sort this out in mid-December, but didn't nail it down until Saturday 2023-12-23. An electronic transfer saves the recipient money, but with the holidays we didn't end up receiving ACH details until the evening of Thursday 2023-12-28. I put in a "Next Day" transfer with Bank of America that evening, got an automated confirmation, and stopped worrying about it. A bit tight, but a few days to spare.

On Thursday 2024-01-04 I was confused why the money still was showing up in my account. Had I entered the numbers wrong? Did I not hit "submit"? Was I not going to be able to claim this donation on our 2023 taxes?

I called the bank and spoke with someone in the ACH Claims Department who was confused why it hadn't gone through: there was enough money in my account, and while it had initially been flagged as possible fraud it was released. They said it should have succeeded, but they saw it as cancelled on Wednesday 2024-01-03 and were also confused why I wasn't sent any form of notification. Since there was no way to resume a cancelled transaction, they recommended sending it again, which I did.

They also gave me a different department to try, but we were near the end of the business day and I couldn't reach them. I tried again the next day, 2024-01-05, and I learned that it was cancelled because there was a delay in the Person to Person Detection Unit. Apparently this is the first step in their internal checking of whether a transfer is allowed. It sounds like there was some manual processing required, with the holidays they didn't have enough staffing to handle it in time, it "timed out", and was automatically cancelled.

I asked if they could send me written confirmation, but they weren't authorized to. I talked to a few other people on the phone who also weren't authorized. Eventually someone told me to go to a branch in person, which seemed odd, but I went in.

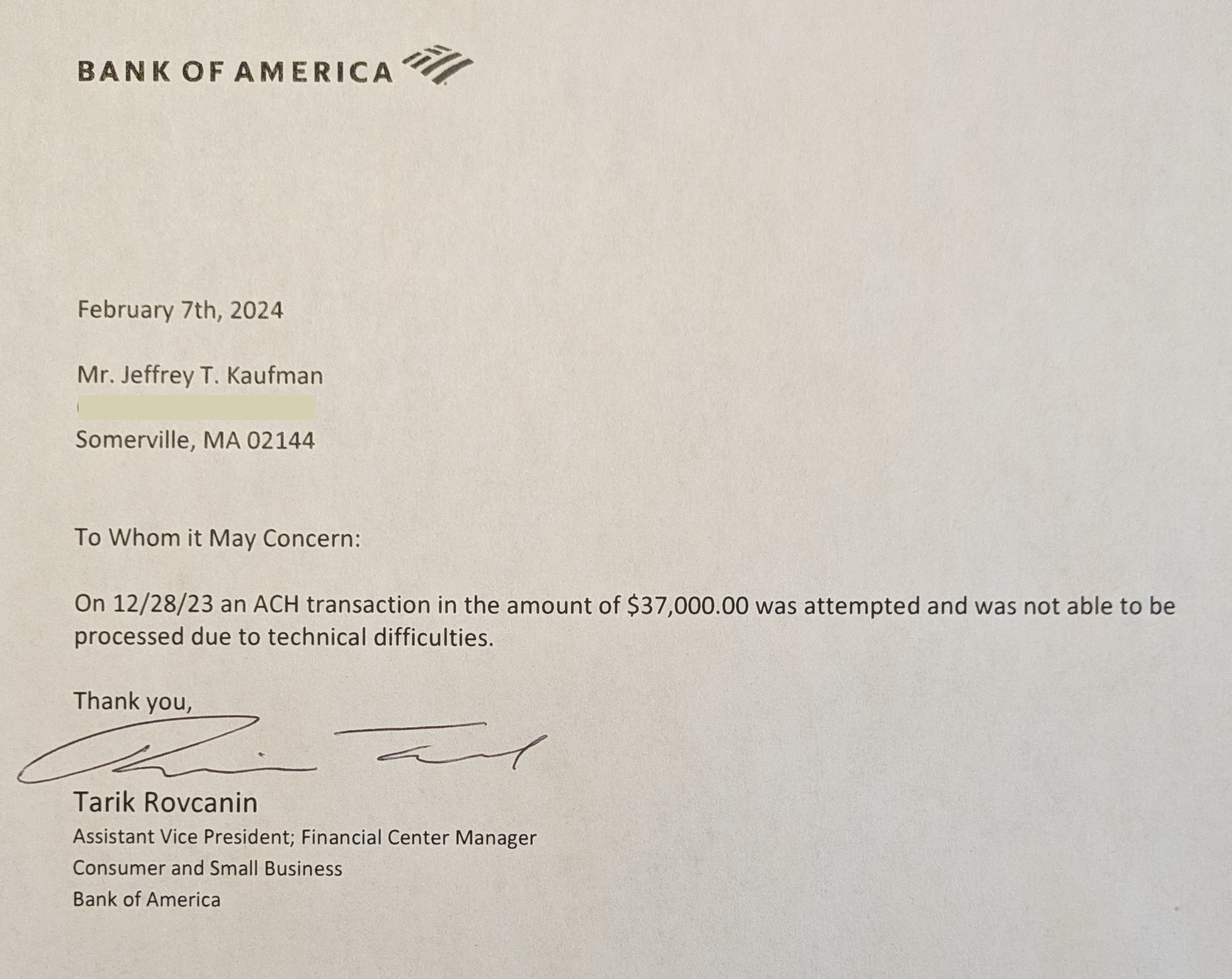

I ended up talking to a Financial Center Manager, who was very sympathetic. He told me he'd escalate internally, and while it took a little while I ended up receiving a letter today:

It's unclear whether this can be counted as a 2023 donation. If you put a check in the mail before the end of the year, it counts for that year. If the check bounces, though, it doesn't. But how do you handle it if the bank fails to complete the payment because of their own internal failures?

I suspect I can't count it as a 2023 donation, though our accountant hasn't gotten back to me yet.

Overall, this is a potentially expensive lesson in why it's better to make up your mind about year-end donations early and transfer the money with plenty of time to spare.

Comment via: facebook, mastodon

2 comments

Comments sorted by top scores.

comment by Dagon · 2024-02-10T21:17:19.896Z · LW(p) · GW(p)

Yup, known risk of hyper-legible IRS requirements and best efforts (but pretty good) banking system. Cash-basis (most personal and tiny-business accounting) is strictly based on "when money changes hands", which is ambiguous in many transactions. If you have the documentation that you submitted the ACH before midnight local time on Dec 31, it's "probably" ok (obDisclaimer: not legal or financial advice). Your accountant may have a different opinion, based on risk and hassle if someone decides to make a stink about it. There are written guidelines, but not enough case law to know exactly how it'll be enforced, and in fact it almost certainly won't be enforced. And if it is, the penalty will only be the tax difference plus interest (plus hassle and accountant fees, which are probably the bigger worry), as you had no intent to defraud.

On the object level, if you have investments at a broker and make significant donations, I HIGHLY recommend setting up a "Donor-Advised Fund" with your broker. This is an account to which you can donate money AND securities (which are liquidated at donation time), and get to count as a donation of appreciated value in the current year without reporting capital gains. You can request (which is always honored) donation to any legal charity at any time, with no tax consequences about the timing of the donation. Value donated but not yet directed grows in a money-market fund.

This means your annual tax choice is only about HOW MUCH to donate (and what unrealized capital gains to donate with it). The choice of WHO and WHEN to give it is decoupled from taxes.

comment by M. Y. Zuo · 2024-02-10T17:55:19.571Z · LW(p) · GW(p)

Isn’t this an implied possibility of having a physical organization handling anything?

Even if it was fully staffed, if the department offices caught on fire you still would have been delayed by this ‘strange ACH corner case’.

So I’m not really sure how it’s a corner case, since there are an infinite number of possible ways the bank’s internal procedures are not completed within that time window.