Eth2 Staking explained as a Financial Instrument

post by Annapurna (jorge-velez) · 2020-12-02T03:33:19.776Z · LW · GW · 6 commentsContents

Eth2 Staking is very similar to purchasing a bond. The return you receive for staking Eth2 is inversely correlated with the amount of Eth2 staked in the protocol. None 6 comments

A major cryptocurrency can now be applied as an income generating asset.

If you don’t keep up with cryptocurrency news, you probably don’t know that today marks the beginning of one of the most important updates in one of the largest cryptocurrencies out there.

Ethereum, the largest cryptocurrency by transactions per day, and the second largest cryptocurrency by market capitalization, has started transitioning its consensus protocol from Proof of Work to Proof of Stake. This marks the beginning of Eth2 (also known as Ethereum 2.0 or Serenity).

I am not going to explain what Ethereum is or the main differences between Proof of Work and Proof of Stake. There are plenty of resources out there that explain what Ethereum is far better than I ever will. Instead, I am going to explain why Eth2 Staking is a financial instrument using finance terminology.

Eth2 Staking is very similar to purchasing a bond.

Staking (Depositing) Eth2 in the Beacon Chain is the equivalent of calling your broker and buying a corporate or government bond. That being said, today it is far easier to buy a bond today than it is to deposit Eth2. To buy a bond today, you would call your broker/financial advisor and they would ask a trading desk to source the bond. After agreeing on the price, the trade is executed and you will see the bond in your account the next day. To stake Eth2 today, the process is far more complex. That being said, some intermediaries have started to provide staking services and I would not be surprised if in a couple of years major financial institutions also offer staking services, which would make the Eth2 Staking process just as easy as buying a bond.

There is no end date to Eth2 Staking. This is similar to perpetual bonds.

To stake Eth2, you need 32 ETH ($19,611 USD). This is the equivalent of the Face Value (FV) Minimum Piece when buying a bond. Most FV minimum pieces for bonds are either 1,000, 2,000, 10,000 or 200,000.

If you want to stake more Eth2, you need to do it in 32 ETH increments. This is the equivalent of the FV Minimum Increment when buying a bond. Most bonds have minimum increments of 1,000, although rarely some bonds have higher increments. The Santander 5.179% 2025 bond is one of those rare bonds that has a minimum piece of 200,000 and a minimum increment of 200,000.

Today, you only can stake (deposit) Eth2. Once the Eth2 protocol reaches phase 1.5, you would be able to exit (withdraw) your stake and the returns generated. There will not be a secondary market for Eth2 stakes. This would be the equivalent of only being able to buy or sell the bond directly from the issuer. Every time you buy the bond from the issuer, the issuer creates a new piece and every time you sell your bond back to the issuer, the issuer takes that piece out of circulation. This is one of the major differences between Eth2 Staking and trading a traditional bond. Traditional bonds have secondary markets.

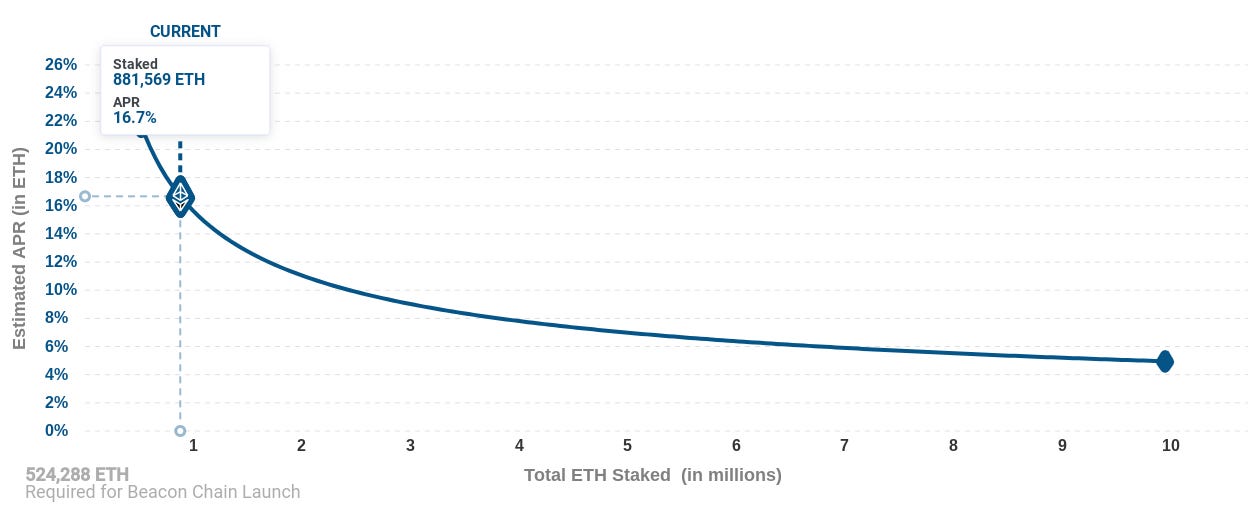

The return you receive for staking Eth2 is inversely correlated with the amount of Eth2 staked in the protocol.

The current APR for Staking Eth2 is 16.7%. Source: Eth2 Launchpad

Over time, the amount of Eth2 staked will increase, reducing the returns for everyone in the protocol. The system was designed to reduce the return through exponential decay, meaning it will never reach 0% APR. The APR is expected to never fall below 1.2%. Considering that today the US Treasury Bill expiring in a month pays 0.084%, The minimum APR is quite attractive. This is another major difference between Eth2 Staking and a traditional bond. A traditional bond has either a fixed rate (Like the Santander example above, which has a fixed rate of 5.179%) or a variable (floating) rate which is typically based on a reference rate (LIBOR being the most common one in recent years) + a spread. The return earned staking Eth2 will oscillate over time, and will be dependent on the participants trust on the Eth2 consensus protocol.

This makes Eth2 a novel income generating financial instrument. In the future, once the Eth2 is fully running (Phase 1.5 and beyond), an individual will be able to enter and exit the protocol based on what the current return is on staking Eth2. It’s too early to know what the return equilibrium will be, but if I had to guess, it would be a combination of the trust of the market on the Eth2 protocol (You can call this the ‘credit risk’ of Eth2) and the current risk free rate.

You can stake Eth2 today if you have at least 32 ETH. However that comes with significant risks listed below.

- In phase 0, there are no withdrawals. Your ETH will be locked for an undetermined period of time.

- As explained in this link, setting up an Eth2 Stake is quite complicated at the moment. Messing up the setup phase could mean losing your entire stake.

- Once your Eth2 stake is successfully setup, you need to ensure that your validator is properly running most of the time. Failure do to so would incur penalties.

- The Eth2 consensus protocol could not work as intended, significantly reducing the value of Eth2 relative to USD.

Most of these risks will disappear once the protocol reaches phase 1.5 and more intermediaries begin to set up staking services.

As we begin phase 0 of this new journey, investors will be watching closely how this new protocol develops. If Eth2 works as intended, Staking Eth2 will become a new type of asset to invest in, one that theoretically should have a low correlation with the market in general and should generate outsize returns relative to the risk free rate.

6 comments

Comments sorted by top scores.

comment by Zolmeister · 2020-12-02T06:41:23.325Z · LW(p) · GW(p)

There will not be a secondary market for Eth2 stakes

Actually, Coinbase just announced intent to deliver this secondary market. A tokenized Eth2 stake may then also be traded on DeFi exchanges. https://blog.coinbase.com/ethereum-2-0-staking-rewards-are-coming-soon-to-coinbase-a25d8ac622d5

Replies from: jorge-velez↑ comment by Annapurna (jorge-velez) · 2020-12-02T16:20:10.556Z · LW(p) · GW(p)

Thank you for sharing. It's great to see these services already commit to Eth2 staking.

I wouldn't call this a secondary market though. This is more Coinbase becoming an intermediary between the customer and the Eth2 staking process.

A secondary market would be being able to buy and sell validator nodes. I do not think this would happen for two reasons:

- Security. Every validator has a set of keys. A secondary market would imply the sharing of those keys.

- Pricing. A secondary market would imply that the market value of validators (32 ETH) would fluctuate. Why would you sell a validator for lower than 32 ETH (and inversely buy a validator for more than 32 ETH) if the consensus protocol will always allow you to set up a node (and in phase 1.5 and beyond, exit a node) for 32 ETH?

↑ comment by Zolmeister · 2020-12-02T21:26:06.065Z · LW(p) · GW(p)

If I understand correctly, then Rocket Pool fits the bill. It is a network (with mild centralization) that allows people to buy and sell shares of a validator pool. Risk is spread across the network in case of node failure.

Note on 1, the withdrawal key is separate from the validator key, such that one can validate but not withdraw.

Edit: Though I agree on 2, that in the long term the fees such networks will be able to charge will decline significantly.

comment by knite · 2020-12-05T00:36:01.610Z · LW(p) · GW(p)

As a holder of other crypto (primarily BTC), how interesting is this opportunity relative to riding current growth?

Replies from: jorge-velez↑ comment by Annapurna (jorge-velez) · 2020-12-08T15:21:58.749Z · LW(p) · GW(p)

Currently growth of cryptocurrencies (Including ETH) is solely based on what the market thinks it's valued (The most similar asset to compare it to would be gold). Sadly, the original vision of Satoshi Nakamoto has not come into fruition in any of the major cryptocurrencies.

The original utility of BTC was to become a medium of exchange. Today, the 'utility' of BTC is to primarily be used as a store of value.

The move of Ethereum from proof of work to proof of stake fundamentally changes the way we can derive its value. You can break it down the following way:

- ETH can still be considered a store of value just like BTC

- ETH can be staked to validate transactions and generate income

- The development of Sharding, if successful, will allow Ethereum to become a medium of exchange, just like a major currency.

↑ comment by Matt Goldenberg (mr-hire) · 2020-12-08T18:50:47.647Z · LW(p) · GW(p)

- The development of Sharding, if successful, will allow Ethereum to become a medium of exchange, just like a major currency.

I don't understand the relation to sharding and Eth being a medium of exchange. Can you elaborate?