While we wait for the verdict on Anthropic’s Claude Sonnet 3.7, today seems like a good day to catch up on the queue and look at various economics-related things.

No tax on tips. It’s dumb, but it’s a campaign promise. He notes that as long as people still have to declare their tips, and we don’t allow those with high incomes to pretend to take half their income in tips, not taxing tips directly won’t matter much, so we should relax.

I think this is far too big an assumption of competence, but given this has to get through Congress, we’re probably safe from the madness.

No tax on social security. He explains why the benefits shouldn’t be taxed.

I get that, but this is a big benefits increase, in a way that doesn’t seem necessary, that transfers money from young to elderly, and which puts a lie to every other ‘we are running out of money’ complaint.

No tax on overtime pay. This one is sufficiently stupid that he can’t pretend that it would not be a huge disaster, the incentives are so awful.

Renewing the Trump tax cuts. Yeah, yeah. Probably a good idea.

Adjusting the SALT cap. He’s against this because of the incentive it gives to states to raise their income taxes.

I notice that when SALT was capped no states lowered their income taxes? He’s only going to fiddle at margins anyway.

Closing the carried interest “loophole.” He says this one is unclear. He points out actual capital gains taxes are stupid, so we should be thankful the rate on those is lower (true), and given this is the case the financial wizards would only find a new loophole.

The level of friction required to get loopholes matters, and indeed many out there already do actually pay their taxes, myself included.

Most of this tax break is going to hedge funds and private equity, I don’t see any reason the tax code should be encouraging these forms of business. I’m not against them, but we are likely allocating too much capital and talent here.

A small portion of the tax break goes to venture capitalists, and yes this part is good policy and we should try to preserve that part of it or make up for it some other way.

Taxing Unrealized Capital Gains

Norway doubles down on its unrealized capital gains tax strategy, including an exit tax of 38% of net assets including unrealized gains, despite having a gigantic sovereign wealth fund from its oil wealth. Norway has a lot of ruin in it due to the oil and high human capital, but this is painful to see.

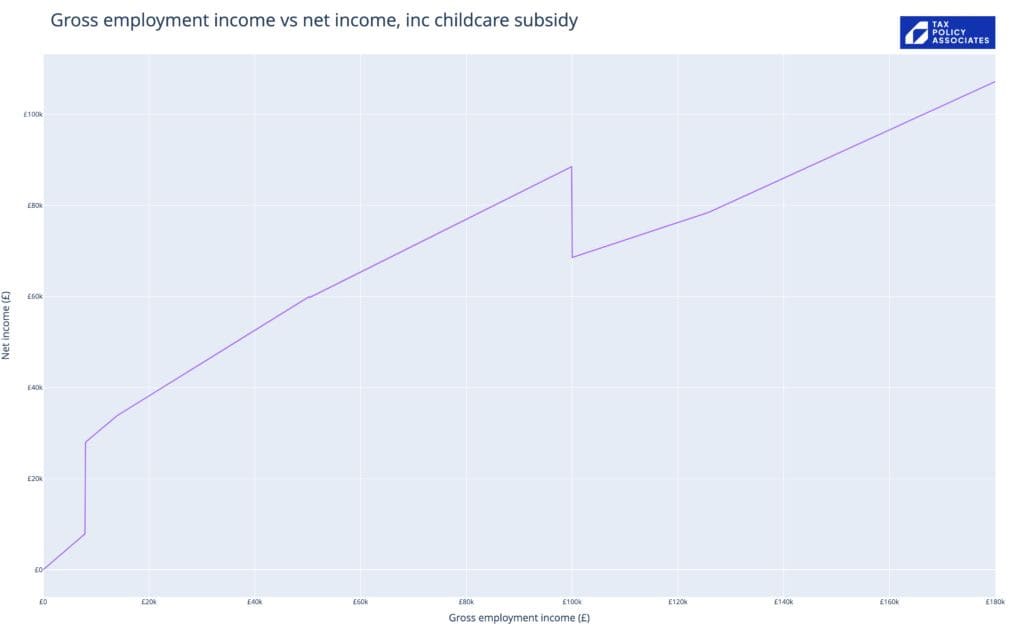

Dan Neidle: The 20,000% spike at £100,000 is absolutely not a joke – someone earning £99,999.99 with two children under three in London will lose an immediate £20k if they earn a penny more. The practical effect is clearer if we plot gross vs net income:

David Algonquin: This must be one of the worst pieces of tax policy design ever. I know people who have dropped down to a 4-day week or, if self-employed, take on less work to avoid this trap.

That’s hard to see, but it means that in this scenario you are better off making 99k than 100k+, unless you can make over ~145k. Normally it’s nowhere near this crazy, but you can be a lot less crazy than this and still rather crazy.

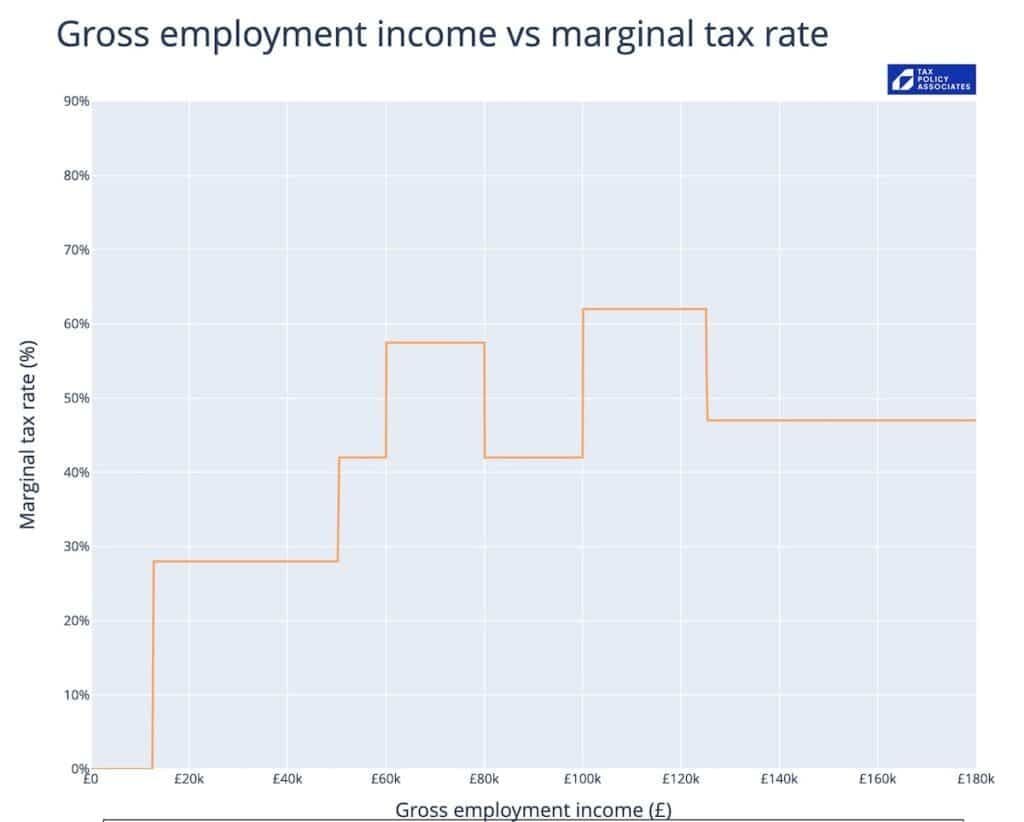

Dan Neidle: It’s perfectly coherent and rational to think high earners should pay 62% tax (and of course also coherent and rational to disagree).

But surely nobody thinks we should have 62% tax on people earning £100k-125k, and 47% on people earning more than £125k?

And it can get worse. If Jane’s still repaying her student loan, that’s another 9% – the student loan system behaves like a crude graduate tax. Jane’s marginal rate reaches 71%.

Trade Barriers By Any Name Are Terrible

Europe still has sufficiently strong trade barriers that they are equivalent to a 45% tariff on manufacturing and 110% for services, according to Mario Draghi. That’s without even considering the ‘trade barriers’ that exist within-countries in the form of ‘EU being the EU.’ o3-mini-high estimated that this costs the EU RGDP growth in the range 0.2%-0.5% per year, versus taking those barriers down.

A similar situation exists between Canadian provinces, which continues to blow my mind because not only is it a huge own goal for no reason, it is so profoundly unpopular and everyone wants to get rid of it, and somehow it is still there.

Destroying People’s Access to Credit

One serious danger with the new administration is a potential cap on credit card interest rates at 10%, with Senators Sanders and Hawley planning to work on this with President Trump. This would severely limit the ability of the poor, or those with poor credit, to access credit cards, and the alternatives to credit cards are all vastly worse.

Living Paycheck to Paycheck

We also had yet another round of people falsely claiming that 60% of Americans live paycheck to paycheck, for various reasons this claim simply will not die despite a majority of Americans having actual cash savings that can pay for 3 months of expenses, even before dipping into credit cards, and the median household having a net worth of $193k. There are horrible crimes of statistics happening around such claims, in both directions, but the central truth is very clear.

Damon Chen: My friend told me he and his wife live paycheck to paycheck.

I don’t believe it because they both are high earners in tech, and he even works for Google. But after doing a little bit of math, I found out he didn’t lie.

• Mortgage: $17,000/month for a $3M home

• Property Tax: $3,000/month

• Private School: $3,000/month for 1 kid

• Travel: $2,000/month (assuming $20k/year)

• Utilities: $1,000/month

• Groceries: $2,000/month

• Eating Out: $1,000/month

• 2 cars: $1,000/month

So in total $30k per month, not including other misc costs like house maintenance, paying for Netflix, etc.

W-2 employees usually take home only 50% of their salary, so they have to make $60k per month pretax, which is $720k in annual TC.

What’s the point of living a life like this?

This is almost entirely housing and taxes. They’re paying California taxes, which is an extra 10% or so of gross income in this income range, or about $6k/month at $720k annual, and the property costs $21k including utilities (which seem strangely high for a region without much need for heat or AC, are they doing a ton of EV charging maybe? If so that half of it should be filed under the cars). That’s $27k, everything else costs a combined $9k.

Cutting other spending won’t make that much difference for them. Yes, $20k/year for travel (that can’t be expensed) seems crazy to me, but some people value it. Others are saying groceries and eating out are too high here, again there is room to cut but I do think you can get a lot of value from the premium there. So it really does come down to, how much does a family of three want a $3 million home (with a not fun interest rate)?

I’d also question buying both a $3 million home and a private school. If you’re paying that much, presumably (since he’s working at Google) they’re in Palo Alto, which does kind of justify the home price if you want to go large enough to plan for a big family, but then that area is said to have excellent public schools. It’s a hell of a lot to pay for that shorter commute.

Presumably this is because the franchise value and forward deal flow of VC firms was cratered so much by government crackdowns that the firms have chosen to hound past founders despite knowing this destroys their future deal flow. All that’s left is to get what they can from their existing obligations, which in China technically gave them the opportunity to do this, and now they’re actually doing it at scale.

One assumes that no sane person would sign such terms now that the equilibrium has shifted. It’s one thing to have confidence in your startup and take a shot knowing the odds are against you. It’s another thing to do that when failure ruins your life.

From most perspectives I know, this makes absolutely no sense. It is the ultimate ‘isn’t there someone you forgot to ask’ meme. It’s not even a reduction to what the judge considered reasonable, it’s throwing out the entire package.

Paul Graham: It used to be automatic for startups to incorporate in Delaware. That will stop being the case if activist judges start overruling shareholders.

This evening the CEO of a public company told me that all startups should reincorporate in Nevada. That’s apparently the best alternative, and for startups that are still private it’s trivially easy.

The judge’s explanations are, again by most perspectives I know, absurd.

Judge McCormick: Even if a stockholder vote could have a ratifying effect, it could not do so here. Were the court to condone the practice of allowing defeated parties to create new facts for the purpose of revising judgments, lawsuits would become interminable.

“We can’t allow defeated parties to create new facts”? What the actual ****? I mean, do you even hear yourself? This makes no sense.

Similarly, claims that the disclosures on the current round were not good enough? They literally stapled the judge’s previous ruling to the disclosures, and were very very clear what Musk was getting, even though it was now vastly more valuable. Absurd.

I presume Judge McCormick’s actual logic is something else entirely. I presume it is some combination of:

Elon Musk broke the rules, and potentially committed outright fraud, by using a compliant board to give him an absurd pay package. We cannot allow him to use this to create an anchor from which he will then benefit.

I don’t think it’s reasonable to pay this much money, and I have the right to impose that opinion on Tesla.

Seriously, though, f*** this guy.

Should startups respond to this by reincorporating in Nevada? I have not done the research on the host of other consequences, but my assumption would be no. This is an extraordinary case that is unlikely to be a meaningful precedent. Most of the time, when someone has the level of chutzpah and obviously unacceptable self-dealing that Musk has, invalidating their absurdly huge pay package is a reasonable decision. I see why people would be concerned, but I see this as a one off.

I also see this as part of the standard warning from the startup and Paul Graham crowd, or the Marc Andreessen crowd, that if anyone ever does something they don’t like, that entity will rue the day, rue the day I tell you, because either the startup ecosystem will be Ruined Forever or everyone involved will pick up their balls and go elsewhere. The sky is always about to be falling. Usually, the sky is fine.

I mean, obviously, if you had a full time machine. The sky’s the limit, then. But what if you only had a glimpse to work with and limited options?

In the ‘Crystal Ball Trading Game’ players are given $1 million in play money, and 15 opportunities to see the front page from two days in the future (on the same 15 randomly chosen days) and then trade, with up to 50 times leverage, the S&P 500 and 30-Year Treasuries, evaluated at tomorrow’s close. They report that the median trader, from a mostly savvy pool, had only $687,986 left.

Spencer Jakab: But how does one explain the median loss of 31%? Surely being able to bet heavily on the really obvious, no-brainer newspaper headlines should make up for a few errors? In fact that proved to be many players’ financial undoing, with a not-insignificant number having negative money by the end. The first lesson from the game, then, might be to curb your enthusiasm in such cases.

Any true inhabitant of The River would think very differently about this.

You are being given a one-time unique opportunity. There are no transaction or financing costs, so you definitely have an edge however small, but you only get 15 moves, some with clearer edge than others. The more money you make early, the more you can bet later.

Yes, there are decreasing marginal returns to money, but you’re not in that much danger of hitting them. If you bet at random with the maximum 50x leverage on the S&P for 15 random uncorrelated days, you probably don’t even go broke.

So in that situation, you would correctly want to risk ‘going broke’ within the experiment, bet with giant leverage, and act such that, unless you are outstandingly good at directional predictions, more often than not you lose money.

This contrasts with the story of giving someone 30 minutes of 60/40 coin flips and $25 to bet, with a maximum win of $250. If you can’t win the max almost all the time there, you’re doing something very wrong. Indeed, you should play remarkably conservatively, exactly because you should have no trouble hitting the cap. So instead of betting Kelly’s 20% each time, you should bet substantially less than that.

However, suppose the experiment was very different and you didn’t have a $250 limit. But again, you only have 30 minutes. So you get a 60/40 flip as fast as you can name the sizing and do the flip. Let’s say you can, if you do your sizing quickly, do 4 flips a minute, so you get 120 flips. Kelly only wins you a few thousand dollars on average. If you instead bet half each time, you average a few million. You should definitely be at least that aggressive here given the time limit, at least until you get quite a lot of funds in hand.

Remember Ocean’s 11. The house always wins, unless when you have the edge, you bet big, and then you take the house.

Are You Better Off Than You Were Right Before the Election?

This data very clearly says that people’s economic perceptions are being heavily warped by that hell of a drug, partisanship, in both directions. There’s no other way this data makes sense. What are people thinking?

Zachary Mazlish: Well, turns out, if you are so bold as to close FRED for a second and ask people, 81% of people believe that prices increase faster than wages during inflationary times, and 73% of people believe their purchasing power decreases.

But are they right?

…

I myself have been extremely confused about this issue, and after having spent the bulk of my post-election haze trying to decipher things, I can now report in high spirits that I am only somewhat confused.

Inflation did make the median voter poorer during Biden’s term.

In no part of the income distribution did wages grow faster while Biden was President than they did 2012-2020.

This is true in the raw data, and even more stark after compositional adjustment.

In particular, the change in median incomes was well below its 2012-20 run-rate.

But, the change in median wages is not what matters; it is the median change in wages that does. And this metric was even weaker under Biden: lower than any period in the last 30 years other than the Great Recession.

People do not feel wages, they feel total income. And median growth in total income — post taxes and transfers — was not just historically low: it collapsed and was deeply negative from 2021 onwards.

Much of this decline is due to timing of pandemic stimulus and even less the “fault of Biden” than other things.

So on #1, the obvious response is, that wasn’t the question. That does not tell you whether people were made poorer, it tells you they became overall less richer. But that’s fine, this was only the setup.

Why is this what matters? It’s a bizarre metric. Why should we care what the median change was, instead of some form of mean change, or change in the mean or median wage? Unless the claim is that voter perception is shaped primarily by their own change in income. That could be a political story but it isn’t a story about economic reality.

So we’re saying that what is happening here is that voters are evaluating income post taxes and transfers, purely for themselves, and then blaming the result on inflation? Perhaps they are indeed doing that, and you can’t do that. I mean, obviously you can, but it’s not a map that matches the territory, again unless the territory you care about is perception.

The attempt to justify #2 is… not great:

To see why the median change in wages is the relevant object for thinking about the election, imagine a world where you had 3 different people: person A with an income of $4, person B with an income of $5, and person C with an income of $10. If four years later person A is now only making $1, person B is making $6, and person C is also making $6, the median income has increased!

But if there were an election, the median worker — who is also the median voter2 — did not have a good last four years, financially speaking. Hence why the median change in income is the object of interest.

In this world, mean income went from $6.66 to $4.33. Of course everyone thinks things got a lot worse. The median income happened to go up, but wages overall are dramatically down. It’s a perverse example, where median income happens to be horribly misleading.

Contrast that with this world (all numbers in real terms):

Time period 1: A makes $1, B makes $6, C makes $10.

Time period 2: A makes $10, B makes $5, C makes $9.

The median change in income is negative, two out of three people saw their wages decline. Do you think this means the economy got worse?

Here’s another graph.

That does look like poor (although still net slightly positive) performance for Biden.

In my opinion, weekly earnings are more relevant than hourly earnings for understanding voter psychology, and likewise, annual earnings are more relevant than weekly earnings: it is annual earnings that determines the overall state of your finances.

This seems to me like a well researched story about voter psychology, that is then being portrayed as inflation making people actually poorer, when we can’t even attribute the voter psychological reaction to the inflation, without knowing the counterfactual.

And indeed, the third point makes clear a lot of what this was about:

Point 3: Post all taxes and transfers, the median household’s real income collapsed while Biden was in office — due to the timing of the Pandemic stimulus.

Yes, exactly. The story is that the big subsidies happened under Trump, and then got taken away, and voters blamed Biden for the difference, plus things overall were unimpressive especially relative to the previous boom decade once we pulled out of the Great Financial Crisis. And indeed, the author notes explicitly this is not the fault of either Biden or inflation.

If you put this all together, saying ‘inflation’ gave the voters a way to blame Biden for the decline in their real purchasing power that came in large part from the end of the stimulus, in addition to its other effects. You also see the partisan splits in perception of the economy, as you always do. In a world where a majority of voters dislike each party, and Biden was unpopular, it’s easy for people to use any excuse to think the economic times are bad.

Could Biden have done anything about all this? To some extent absolutely. There were any number of pro-growth policies he left on the table, and ways he actively got in the way of growth, and he overspent. But he was also, as many have noted, dealt a rather terrible hand on this, with the timing of the stimulus and resulting inflation. The fact that we outperformed almost all other countries economically during this period? Irrelevant to the median voter, who wouldn’t notice or care.

Most People Have No Idea How Insurance Works

People think insurance should be some sort of magic thing, and complain when insurance companies price their products based on their costs plus a profit margin, and attempt to actually model the risks involved. Yes, insurance companies will act like scum to weasel out of paying if they can, but that’s a distinct issue.

The most pure version of this was an old Chris Rock routine where he says that they should call insurance ‘in case shit.’ And then he says, ‘if shit don’t happen, shouldn’t I get my money back?’ And the audience cheers. Except, well, yeah.

And no, this isn’t a weird Chris Rock thing. It’s common.

Spooky Werewolf Media: To be fair it’s not just that people don’t understand rudimentary aspects but that these things are propagandized and confused and marketed to hell and back by legions of bullshit artists.

Jeremy Kauffman: The degree to which society functions despite massive swathes not understanding even rudimentary aspects is a huge testament to capitalism.

Do Not Spend Too Much Attention on Your Investments

(Nothing I write is ever investment advice, etc etc)

I write this note every so often, I think it’s important.

Duderichy: People vastly underestimate the alpha you have in your career!

If you’re in tech, you should be focusing on locking in a $500,000+ staff job instead of getting an extra $20,000 per year off your investments.

You can make a lot off your investments, but it’s hard to turn a lot of extra time into a lot of extra alpha, especially when your net worth is not large compared to your earning potential.

You do want to put in enough time to do something ‘reasonable’ but the answer (assuming you’re not planning for AGI) is plausibly things like ‘just find the right place to live, have an emergency savings account and then buy index funds, maybe buy index funds in industries that look promising and throw in some individual stocks and then forget about it.’

Beyond that, if your shower thoughts are focused on your investments, that will usually be a mistake until your investments are large compared to your income and career potential. Even when the amount of money at stake look large, that doesn’t mean the difference in alpha available from more attention is very high.

Insider trading increases liquidity from insiders that you don’t want to trade against. It decreases liquidity you do want from everyone else, who are subject to adverse selection.

In my experience, markets vulnerable to insider trading see their liquidity shrink dramatically – a clean example is if there is important unknown injury information in a sporting event, it all but kills the action until the information gets out, and markets for potentially fixed leagues are super thin.

Or: Who do you think is paying the insider traders their profits?

Insider trading might increase price efficiency, or it might not. Insiders have the incentive to fix prices, but others have far less incentive to do so. If I see Nvidia trading at 400 and my analysis says it should be 360 or 440, how do I know this isn’t because of insiders, and given that how do I dare trade? Or as they say in sports trading when the odds look weird: “Somebody knows something.” Maybe.

Whereas the insiders, this says, are against insider trading. Which I could see if it was due to it killing liquidity and ability to raise capital, but then that feeds back into the previous claim.

Alex Tabarrok asserts an evolving new consensus on the minimum wage, that effects are heterogeneous and take place on more margins than employment. I don’t know about the claim of an emerging consensus, but the claims themselves seem obviously true. In particular, those hurt by minimum wage laws are typically the worst off among us, with others largely unaffected, as economics 101 would suggest.

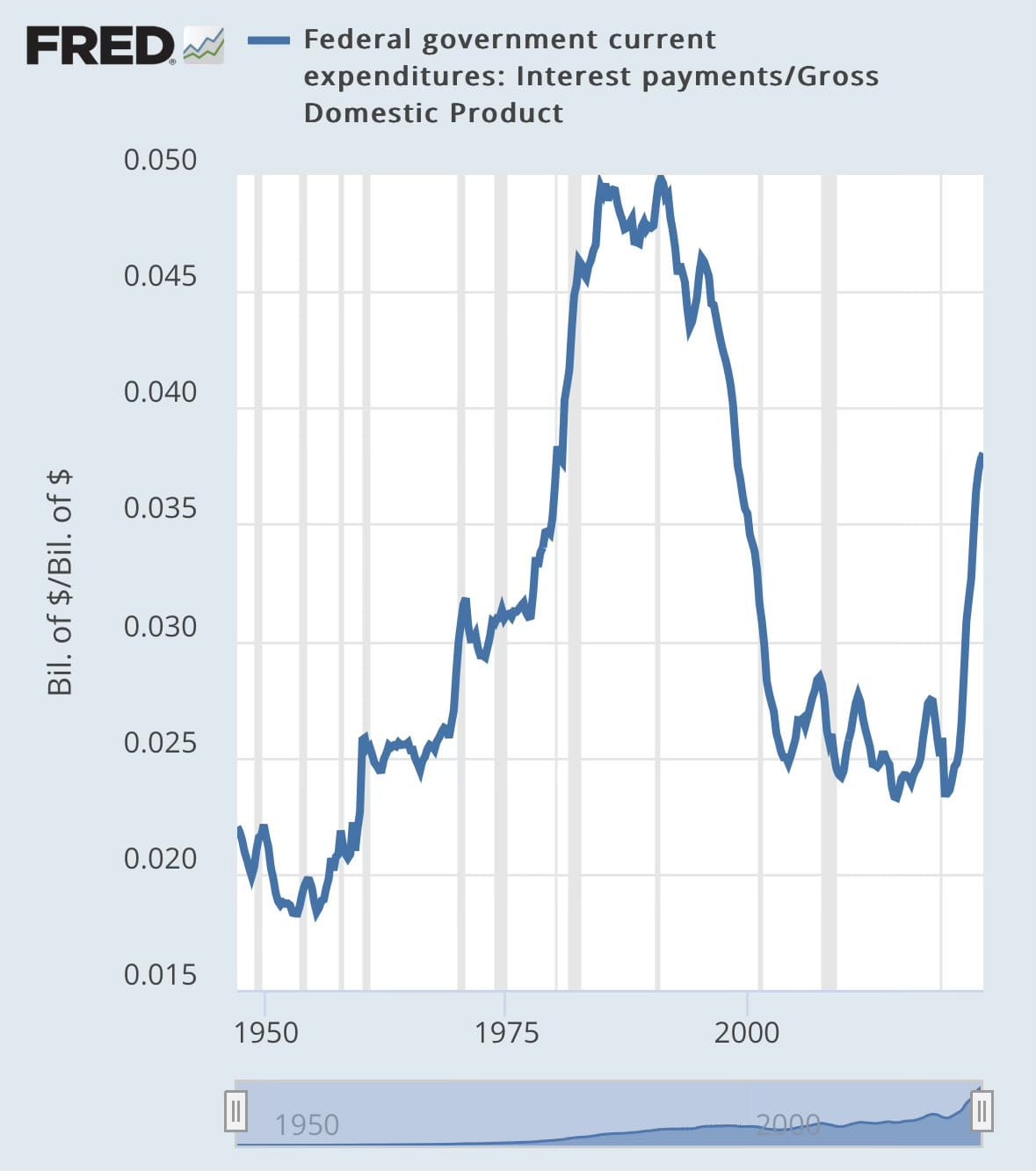

The National Debt

Whenever I see warnings about the national debt, like this one by Arnold Kling, they usually employ calculations like this one, where Kling quotes Cowen pointing the Rauh.

Joseph Rauh: if I use CBO projections to calculate the interest-to-revenue ratio, it reaches 22.9% by 2034.

The important warning that Kling is the latest to reiterate is that the bond market is currently in the good but unstable equilibrium of everyone expecting the government to pay its debts in valuable dollars, at least on a rolling basis. That means interest rates are reasonable. If we shift to the bad equilibrium, where investors do not assume this and demand higher prices, then we won’t be able to pay our debts without some form of large default, we will be vastly poorer, and there is no easy way back.

When we take on more debt, we raise both the danger that this happens, and the damage it would cause if it did happen. The good reason not to take on more debt is this tail risk.

There are remarkable similarities to things like AI existential risk – we know that going down this road will at some point start introducing steadily increasing risk of catastrophe, but until then we likely enjoy good times. There’s huge value in taking on a non-trivially risky amount of debt.

As we enjoy those good times, we don’t know what level of debt is how risky, with some even saying we can take on essentially unlimited debt and it’s fine, and every time we take on more debt people update that it’s safe to take on yet more debt – either you respond before the crisis, or you respond too late. As Kling puts it, ‘pretending there is no problem means that a sudden crisis is likely.’

How much debt is unsustainable? What is the actual current or anticipated debt burden? Tracking interest as a percentage of revenue is asking the wrong question.

There are essentially two questions that seem like they should matter here.

Can the good equilibrium be sustained? If we retain the ability to borrow at the risk-free rate of interest, or something not too far above it, can we keep the debt-to-GDP ratio from rising?

What will the bond market think is the bond market’s future answer to #1?

Japan, among other examples, shows us that we have a poor model of #2, as does the continued willingness to keep buying the debt of Argentina cycle after cycle. The coyote absolutely can sometimes run across thin air for longer than you think. That’s not the kind of thing I am in a position to model well, so I tend to focus more on #1.

According to Google, America pays about 3.35% on its monthly interest-bearing debt, and an average of 3.28% overall. Nominal GDP growth is higher than that, at 4.96%, similar to its historical average of 6.17% from 1948 to 2024. At current prices, the actual effective amount we pay in interest on the debt is less than zero – we could have debt of 100% of GDP, then have a primary deficit of 1.5% of GDP, and end the year with a better debt-to-GDP ratio than when we started.

That tells me that the answer here is more about demand for market priced safe government debt than it is about market price, similarly to the situation in Japan. My expectation is that the limiting factor here is that the ‘giant pool of money’ chasing safe assets is only so large. For now, demand exceeds supply by a lot, so we’re fine, and if someone dumps their supply that’s not an issue. If we try to borrow too much at once, we would exhaust demand, and have to adjust price in order to drum up more demand, not because of risk but because demand curves slope upward. So that’s what I would want to study, to find out where we should worry about potential breaking points.

Paying 5% of GDP in interest definitely sounds like a lot. It makes sense that everyone was actively concerned with the deficit and debt back then. But again, I’d be asking more about the steady-state cost of debt. What would it cost to make payments sufficient to prevent the debt from growing as a share of GDP, if the primary budget was in balance?

Which again brings us back to the question of multiple equilibria. The debt is fine, except for the risk that suddenly it very much isn’t. How far dare we go?

Jim Babcock explains how many memecoins [LW(p) · GW(p)]and ‘market caps’ work, and how very often there is vastly less there than meets the eye. I find the whole thing deeply stupid, and if you propose I get involved with one I will absolutely block you.

Arguments and data in favor of the Peter Principle, that employees get promoted to their level of incompetence. To me this is one of those principles that is obviously true, the question is magnitude. The idea that ‘oh firms know about that, they’d successfully control for it so it wouldn’t happen at all’ is Obvious Nonsense.

Yay economies of scale. Much of what we consume has almost zero marginal product, and its marginal prices are usually falling rapidly to zero. An excellent reason to want more people around.

"Contrast that with this world (all numbers in real terms):

Time period 1: A makes $1, B makes $6, C makes $10.

Time period 2: A makes $10, B makes $5, C makes $9.

The median change in income is negative, two out of three people saw their wages decline. Do you think this means the economy got worse?"

I'm not sure I'm following your overall points in this section, but I'd certainly expect people to vote like they believed the economy got worse in such a situation.

I agree with you. Unless the signal is so strong that people believe that their personal experience is not representative of the economy, it's going to be overweighted. "I and half the people I know make less" will lead to discontent about the state of the economy. "I and half the people I know make less, but I am aware that GDP grew 40%, so the economy must be doing fine despite my personal experience" is possible, but let's just say it's not our prior.

Dan Neidle: The 20,000% spike at £100,000 is absolutely not a joke – someone earning £99,999.99 with two children under three in London will lose an immediate £20k if they earn a penny more. The practical effect is clearer if we plot gross vs net income.

Can't it actually be good to encourage people to not work? I'd imagine if everyone in the United Kingdom worked half the number of hours, salaries wouldn't decrease very much. Their society, as a whole, doesn't need to work so many hours to maintain the quality of life, they only individually need to because they drive each others' wages down.

Economy can be positive-sum, i.e., the more people work, the more everyone gets. Do you think the UK in particular is in a situation where instead if you work more, you are just lowering wages without getting more done?

Not quite. I think people working more do get more done, but it ends up lowering wages and decreasing the entropy of resource allocation (concentrates it to the top). If you're looking for the good of the society, you probably want the greatest free energy,

The temperature is usually somewhere between 0.2 (economic boom) and 1.0 (recessions), and GDPTotal Assets≈0.1 in the United Kingdom. I couldn't find a figure for the Theil index, but the closest I got is that Croatia's was 0.295 and Serbia's was 0.369 in 2011, and for income (not assets) the United Kingdom's was 0.268 in 2005. So, some very rough estimates for the free energies are

The ideal point for the number of hours worked is where the GDP increases as fast as the temperature times the decrease in entropy. I'm not aware of any studies showing this, but I believe this point is much lower than the number of hours people are currently working in the United Kingdom.

You do want to put in enough time to do something ‘reasonable’ but the answer (assuming you’re not planning for AGI) is plausibly things like ‘just find the right place to live, have an emergency savings account and then buy index funds, maybe buy index funds in industries that look promising and throw in some individual stocks and then forget about it.’

I had to say, "wait, which AGI....like in taxes or the other one??" Funny little crossover there.

Why is this what matters? It’s a bizarre metric. Why should we care what the median change was, instead of some form of mean change, or change in the mean or median wage?

The critique that the justification wasn't great because the mean wage dropped a lot in the example is fair. Yet, in the proposed alternative example it remains quite likely that people will perceive the economy as having gotten worse, even if the economy is objectively so much better - 2/3 will say they're personally worse off, insufficiently adjust for the impersonal ways of assessing the economy, and ultimately say the economy is worse.

Neither Δ(MedianIncome) nor Median(ΔIncome) is a bizarre metric. Δ(MedianIncome) may be great for observers to understand general trajectories of income when you lack panel data, but since people use their own lives to assess whether they are better off and in turn overweight that when they judge the economy, Median(ΔIncome) is actually more useful for understanding the translation from people's lives into their perceptions.

Consider a different example (also in real terms): T1: A makes $3, B makes $3, C makes $3 ,D makes $10, E makes $12 T2: A makes $2, B makes $2, C makes $3, D makes $9, E makes $16 The means show nice but not as crazy economic growth ($6.20 to $6.40), and the Δ(MedianIncome) is $0 ($3 to $3) - "we're not poorer!" However, the Median(ΔIncome) is -$1. And people at T2 will generally feel worse off (3/5 will say they can't buy as much as they could before, so "this economy is tough"). Contrast that with (still in real terms): T1: A makes $2, B makes $2, C makes $4 ,D makes $10, E makes $12 T2: A makes $3, B makes $3, C makes $3, D makes $10, E makes $12 The means show nice but not as crazy economic growth ($6 to $6.20), and the Δ(MedianIncome) is -$1 ($4 to $3) - "we're poorer!" However, the Median(ΔIncome) is $0. And people at T2 will generally feel like things are going okay (only 1 person will feel worse off).

And these are comparing to 0. Mazlish's post illustrates that people will probably not compare to 0 and instead to recent trajectories ("I got a 3% raise last year, what do you mean my raise this year is 2%?!"), so #1 means people will be dissatisfied. #2, as it bore out in the data, also means dissatisfaction. And #3, largely due to timing, means further dissatisfaction.

Then it is no surprise that exit polls show people who were most dissatisfied with the economy under Biden (and assumed Harris would be more of that) voted for Trump. Sure, there's some political self-deception bias going on (see charts of economic sentiment vs. date by party affiliation), but note that the exit polls are correlational - they can indicate that partisanship is a hell of a drug or that people are rationally responding to their perceptions. It's likely both. And if your model of those perceptions is inferior in the ways Mazlish notes, you'd wrongly think people would have been happy with the economy.

The fun thing is that the actual profile of wages earned can be absolutely identical and yet end up with incredibly different results for personal wage changes. For example:

In year 1, A earns $1/hr, B $2, C $3, D $4, and E $5. In year 2, A earns $2/hr, B $3, C $4, D $5, and E $1.

A, B, C, and D personally all increased their income by substantial amounts and may vote accordingly. E lost a lot more than any of the others gained, but doesn't get more votes because of that. 80% of voters saw their income increase. What's more, this process can repeat endlessly.

If in year 2, A instead earns $5/hr, B $1, C $2, D $3, and E $4 then 80% of voters will be rather unhappy at the change despite the income distribution still being identical.

Exactly, which is why the metric Mazlish prefers is so relevant and not bizarre, unless the premise that people judge the economy from their own experiences is incorrect.