Two ominous charts on the financial markets

post by arunto · 2022-01-08T14:07:30.897Z · LW · GW · 23 commentsContents

1. Shiller CAPE 2. Historical interest rate trends 3. What follows from this? None 26 comments

The following two charts have been on my mind quite intensively for some time and have had a relatively strong influence on my thinking about dangers for the future development of the financial markets in recent months:

1. Shiller CAPE

An interesting measure of stock market valuation from my perspective is Shiller's CAPE (Cyclically Adjusted PE Ratio). Basically, it is just a price-earnings ratio, but using adjusted earnings over the last 10 years to smooth out the normal cyclical fluctuations.

Source: multpl.com

Admittedly, it is not yet possible to tell from it that valuations and thus share prices will soon be heading downward. But the risk of a crash seems evident to me.

The only time valuations were even higher was in the dot-com bubble around 2000. There is another interesting parallel here. If you look at the statistics on speculation on credit (margin), you see a significant increase in margin positions (FINRA) for some time. At the linked site, you can also find historical data on margin positions, and if you look at 1998-2000, the trend is similar.

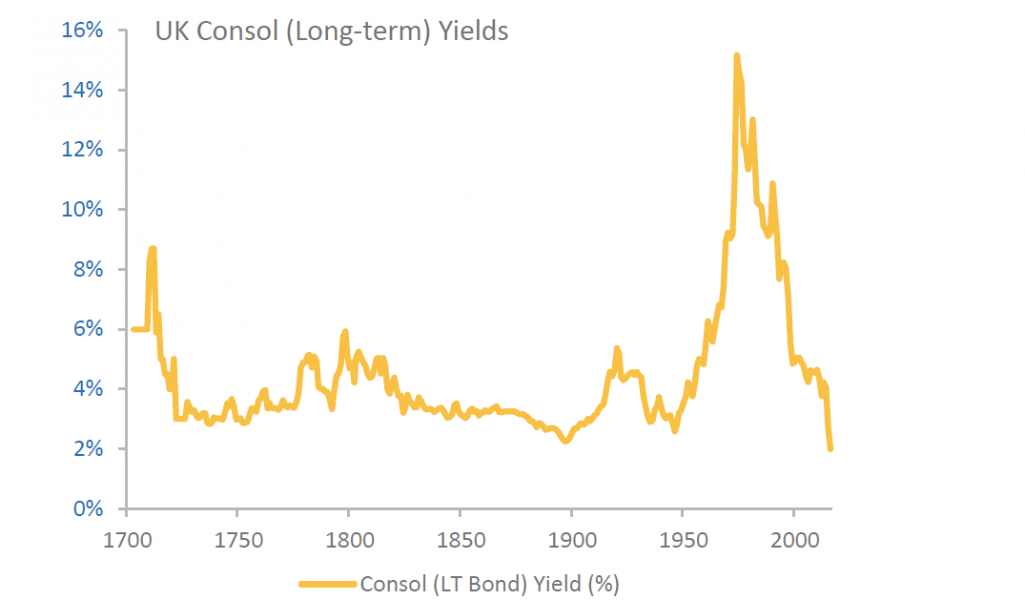

2. Historical interest rate trends

I found the following chart in the book "The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival" by C. Goodhart and M. Pradhan (The book is very interesting in that it derives a forecast of rising inflation not from monetary developments, but from global demographic developments. I found it well worth reading). While I had read the underlying facts (the ongoing interest rate cuts of the past decades cannot continue) before, it was not until I saw this graphic that I actually became fully aware of the problem.

Source: SUERF

From the graph (UK long term bond yield; it could be drawn analogously for many other countries), I draw some rather uncomfortable conclusions:

(a) The interest rate cuts that have characterized the last 40 years in financial markets can no longer continue. In this respect, we are facing a fundamental change in the development of interest rates (transition from falling interest rates to more or less stable interest rates or to rising interest rates).

b) All my implicit knowledge about the financial markets that I gained as a teenager and an adult was formed in an interest rate environment (falling interest rates) that will soon be a thing of the past. So I can no longer rely on my implicit knowledge.

c) The practical experience and thus the tacit knowledge of the vast majority of players in the global financial markets comes from an environment that will not be the same in the future.

In particular, I think the combination of a) and c) is very worrying. We are facing (or perhaps already in) a fundamental change of direction in the financial markets and almost all players only know the previous environment. And for that we have (see 1.) almost a maximum in equity valuations. This can be a recipe for very interesting times.

3. What follows from this?

First of all, this is not financial advice. I am only writing down my personal conclusions and assessments from the above facts:

a) To infer future average equity returns from the past decades seems to me quite dangerous.

b) The valuation level (Shiller CAPE) and the elimination of the interest rate reduction effect for stock valuations indicate that expected future equity returns will probably be significantly lower than those of past decades.

c) The change in the interest rate environment and the inexperience of the vast majority of players with such a change can lead to price movements that go far beyond usual price movements in the business cycle.

d) Even for a relatively short investment horizon, the range of possible returns seems extremely wide to me. If I had to give a range for the price development (e.g. SP 500) until the end of 2022, where I am 90% sure that the price development will lie within this range, my current estimate would be from approx. +30% to - 60%.

23 comments

Comments sorted by top scores.

comment by SimonM · 2022-01-08T17:18:48.266Z · LW(p) · GW(p)

tl;dr all your conclusions are equally consistent with equity returns being similar to the past going forward

a) To infer future average equity returns from the past decades seems to me quite dangerous.

Agreed, although what else do we have?

b) The valuation level (Shiller CAPE) and the elimination of the interest rate reduction effect for stock valuations indicate that expected future equity returns will probably be significantly lower than those of past decades.

Which decades are you looking at? As recently as the decade before last (2000s) we had negative real (and nominal) returns for 10 years.

c) The change in the interest rate environment and the inexperience of the vast majority of players with such a change can lead to price movements that go far beyond usual price movements in the business cycle.

I'm not sure this sentence makes sense?

d) Even for a relatively short investment horizon, the range of possible returns seems extremely wide to me. If I had to give a range for the price development (e.g. SP 500) until the end of 2022, where I am 90% sure that the price development will lie within this range, my current estimate would be from approx. +30% to - 60%.

I think giving 90% CI is probably a bit wide to be useful, but coincidentally:

- The options market forecasts almost exactly 90% for the interval you describe.

- The implied volatility (if we were in a flat vol world) for that [-60%, +30%] having that sort of probability (90%) is ~22% which is pretty typical for equity volatility.

I'd say I'm probably equally bearish as you, but for probably much simpler reasons.

- Real rates (globally) are very low

- Risk premiums are compressed

Therefore we should expect forward returns to be low. The problem (for me) is there isn't much to be done about this. TINA. There is no alternative.

Replies from: waveman, clark-benham, arunto↑ comment by waveman · 2022-01-09T04:31:46.277Z · LW(p) · GW(p)

TINA. There is no alternative.

When required to be fully invested this is trueish.

However you can sit in cash while no appealing investments exist. And buy in size when prices become more appealing.

inb4 market timing is not possible

Have a look at Warren Buffett's track record and the amount of cash he held in early 2000 and now.

↑ comment by Clark Benham (clark-benham) · 2022-01-09T16:51:41.636Z · LW(p) · GW(p)

Options Nitpick: You can't use equity index* option prices as true probabilities because adding hedges to a portfolio makes the whole portfolio more valuable. People then buy options based on their value when added to the portfolio, not as individual investments.

The first reason option hedges make your portfolio more valuable is preferences: people don't just want to maximize their expected return, but also reduce the chance they go broke. People don't like risk and hedges reduce risk, ergo they pay more to get rid of risk. However you can't just subtract X vols to adjust as this "risk premia" isn't constant over time.

Secondly hedges maximize long term returns (or why you shouldn't sell options) You want to maximize your average geometric annual return not average annual return. You care about geometric averages because if for 3 years your returns were +75%, +75%, -100%, your don't have 50% more money then when you started but 0. The average of annual returns was 10.7% over the past 30 years, but if you'd invested in 1992 you'd've only compounded at 8.5% year till 2022.

Geometric returns are the the nth root of a product of n numbers and have the approximation = Average Annual Return - (variance/2). If you could reduce variance and not reduce Annual returns, your portfolio (market + hedges) would grow faster than the market.

These reasons are why despite the worst Annual return being -48% in 1931, you say there's a 5% chance of > -50% returns based on option markets.

*I'm specifically talking index options because that's the portfolio investors have (or something similar) and the total is what they care about. If you were to use prices as true probabilities for say a merger going through these reasons don't apply as much and would be more accurate.

PS. I've referred to investors as all having the same portfolio because most people do have highly correlated index holdings and it's at this level of generality you can think about investors as a class.

Replies from: SimonM↑ comment by SimonM · 2022-01-09T17:09:03.202Z · LW(p) · GW(p)

I absolutely considered writing about the difference between risk-neutral probabilities and real-world probabilities in this context but decided against because: Over the course of a year, the difference is going to be small relative to the width of the forecast

I'd be interested to hear if you think the differences would be material to my point. ie that [-60%, +30%] isn't a ~90% range that stocks return next year and that his forecast is not materially different to what the market is forecasting.

Replies from: clark-benham↑ comment by Clark Benham (clark-benham) · 2022-01-10T08:08:03.906Z · LW(p) · GW(p)

The 2000-2021 VIX has averaged 19.7, sp500 annualized vol 18.1.

From a 2ndary source: "The mean of the realistic volatility risk premium since 2000 has been 11% of implied volatility, with a standard deviation of roughly 15%-points" from https://www.sr-sv.com/realistic-volatility-risk-premia/ . So 1/3 of the time the premia is outside [-4%,26%], which swamps a lot of vix info about true expect vol.

-60% would the worst draw down ever, the prior should be <<1%. However, 8 years have been above 30% since 1928 (9%), seems you're using a non-symetric CI.

The reasoning for why there'd be such a drawdown is backwards in OP: because real rates are so low the returns for owning stocks has declined accordingly. If you expect 0% rates and no growth stocks are priced reasonably, yielding 4%/year more than bonds. Thinking in the level of rates not changes to rates makes more sense, since investments are based on current projected rates. A discounted cash flow analysis works regardless of how rates change year to year. Currently the 30yr is trading at 2.11% so real rates around the 0 bound is the consensus view.

Replies from: SimonM↑ comment by SimonM · 2022-01-10T09:04:43.764Z · LW(p) · GW(p)

The 2000-2021 VIX has averaged 19.7, sp500 annualized vol 18.1.

I think you're trying to say something here like 18.1 <= 19.7, therefore VIX (and by extension) options are expensive. This is an error. I explain more in detail here [LW(p) · GW(p)], but in short you're comparing expected variance and expected volatility which aren't the same thing.

From a 2ndary source: "The mean of the realistic volatility risk premium since 2000 has been 11% of implied volatility, with a standard deviation of roughly 15%-points" from https://www.sr-sv.com/realistic-volatility-risk-premia/ . So 1/3 of the time the premia is outside [-4%,26%], which swamps a lot of vix info about true expect vol.

I'm not going to look too closely at that, but anything which tries to say the VRP was solidly positive post 2015 just doesn't gel with my understanding of that market. (For example). (Also, fwiw anyone who quotes changes in volatility in percentages should be treated with suspicion at best)

-60% would the worst draw down ever, the prior should be <<1%. However, 8 years have been above 30% since 1928 (9%), seems you're using a non-symetric CI.

Yeah, it's not symmetric, but I wasn't the person who suggested it. All I'm saying is "OP says [interval] has probability 90%" "market says [interval] has probability 90%".

The reasoning for why there'd be such a drawdown is backwards in OP: because real rates are so low the returns for owning stocks has declined accordingly. If you expect 0% rates and no growth stocks are priced reasonably, yielding 4%/year more than bonds. Thinking in the level of rates not changes to rates makes more sense, since investments are based on current projected rates. A discounted cash flow analysis works regardless of how rates change year to year. Currently the 30yr is trading at 2.11% so real rates around the 0 bound is the consensus view.

OP being my post of arunto's?

There's several things unclear with this paragraph though:

- Stocks are currently 'yielding' 1.3% (dividend yield) or 3.9% ('earnings' yield). Not sure exactly what yield you think is 4% over bonds. (Or which maturity bond you're considering).

- "Thinking in the level of rates not changes to rates makes more sense, since investments are based on current projected rates.". The forward curve is upward sloping, yes, but if arunto thinks rates are going to change higher than what the market forecasts that will definitely change the price of equities. "A discounted cash flow analysis works regardless of how rates change year to year." Yes, but if you change the rates in your DCF you will change your price

- "Currently the 30yr is trading at 2.11% so real rates around the 0 bound is the consensus view.". Currently 30y real rates are -15bps after a steep sell-off after the start of the year. 30y real rates were as low as -60bps in December.

10y real rates are more like -75bps (up from -110bps in December).

"the 0 bound" is something people talk about in nominal space because the yield on cash is somewhere in that ballpark. (These days people generally think that figure should be around -50 to -100bps depending on which euro rates trader you speak to). For real rates there's no particular reason to think there is any significant bound - 10y real rates in the US have been negative since the start of 2020; in the UK they've been negative since the early 2010s.

↑ comment by arunto · 2022-01-09T07:55:41.091Z · LW(p) · GW(p)

Which decades are you looking at? As recently as the decade before last (2000s) we had negative real (and nominal) returns for 10 years.

Sorry, I should have made that more clear. I am talking about the period since the start of the interest rate decline (mid 1980s to today).

"c) The change in the interest rate environment and the inexperience of the vast majority of players with such a change can lead to price movements that go far beyond usual price movements in the business cycle."

I'm not sure this sentence makes sense?

Let me try to rephrase that: I think we will be seeing a fundamental change in the financial markets due to an end to the 35year long reduction of real interest rates. And most of the actors have only known investing in an environment with more or less constantly decreasing real interest rates. I believe this combination could lead to widespread panic in the markets once the people making investment decision realize that they don't know anymore how the markets react due to the new environment.

Therefore we should expect forward returns to be low. The problem (for me) is there isn't much to be done about this. TINA. There is no alternative.

I believe that rationale for investing in equities is quite widespread today. Obviously, there is an alternative (accepting secure negative real returns), but in order to avert guaranteed losses investors take on risk. I am not saying that this is necessarily the wrong strategy, but it poses an interesting question: How will investors with this motivation for holding stocks react in a downturn?

Replies from: SimonM↑ comment by SimonM · 2022-01-09T09:55:47.129Z · LW(p) · GW(p)

Sorry, I should have made that more clear. I am talking about the period since the start of the interest rate decline (mid 1980s to today).

I think you're going to have to be more explicit about what time period you're forecasting your market collapse. (Or whatever it is you're forecasting, it's still not clear to me).

Let me try to rephrase that: I think we will be seeing a fundamental change in the financial markets due to an end to the 35year long reduction of real interest rates. And most of the actors have only known investing in an environment with more or less constantly decreasing real interest rates. I believe this combination could lead to widespread panic in the markets once the people making investment decision realize that they don't know anymore how the markets react due to the new environment.

Please can you quantify this. There have been plenty of market panics since the mid 1980s til now. What are you saying is going to be different now?

I believe that rationale for investing in equities is quite widespread today. Obviously, there is an alternative (accepting secure negative real returns), but in order to avert guaranteed losses investors take on risk. I am not saying that this is necessarily the wrong strategy, but it poses an interesting question: How will investors with this motivation for holding stocks react in a downturn?

Probably the same way they always react. Selling their stocks aggressively. But again, this isn't different, this is what they've always done.

comment by PeterMcCluskey · 2022-01-09T04:03:12.191Z · LW(p) · GW(p)

I am somewhat more optimistic about interest rates (although I still see some increase coming). The high savings rates of the wealthy will offset the harm from aging. See my blog post here for more on this effect.

As long as interest rates remain somewhat close to current levels, the stock market isn't in much danger of a major crash. But there are a fair number of overpriced stocks, and your concerns are worth some attention.

comment by Radford Neal · 2022-01-08T17:36:30.011Z · LW(p) · GW(p)

In your first figure, are the "adjusted earnings over the last 10 years" adjusted for inflation? When looking at current earnings and price, inflation may not matter (if it isn't changing really quickly), but comparing earnings from 10 years ago to the price today, when there has been a recent sharp increase in nominal prices, could be misleading.

Note that the stock market is somewhat of an inflation hedge, since it (to some extent) represents ownership of real assets. Of course, an inflationary environment is generally bad for the economy as a whole, so one would expect real stock values to decline, but not necessarily nominal stock prices.

The bond yields in your second figure are obviously not adjusted for inflation (ie, they are nominal yields, not real yields after inflation). So I'm not sure one can draw much of a conclusion from it.

By the way... For those squinting at the figures, note that in Firefox one can right click and open the image in a new tab, where it's bigger. May be possible in other browsers too.

Replies from: arunto, waveman↑ comment by arunto · 2022-01-09T07:38:14.428Z · LW(p) · GW(p)

The bond yields in your second figure are obviously not adjusted for inflation (ie, they are nominal yields, not real yields after inflation). So I'm not sure one can draw much of a conclusion from it.

That's true, I should have used a chart with real interest rates (I chose that specific graph because it was the one that made the problem salient for me when I had first seen it).

However, with real interest rates it looks similar:

↑ comment by SimonM · 2022-01-09T10:00:18.164Z · LW(p) · GW(p)

That's not a chart of "real rates", that's the spread between a 10y rate and a spot inflation estimate. Real rates is (ideally) the rate paid on an inflation linked bond, or at least the k-year rate minus the k-year forecast inflation. The BoE have historic data here going back to '85 and the rally is several hundred basis points less than your chart implies.

↑ comment by waveman · 2022-01-09T04:35:22.890Z · LW(p) · GW(p)

are the "adjusted earnings over the last 10 years" adjusted for inflation?

Generally CAPE past earnings are adjusted to inflation.

Historically the stock market has responded badly over time to a rapid change upwards in inflation particularly if interest rates rise correspondingly, due to valuation effects ("net present value") . Subsequently once the market has fallen it tends to act as a reasonable inflation hedge. Typically this occurs around the point when Time Magazine has a front cover saying something like "The Death of Equities".

Different stocks respond differently to inflation. Consider the analogy of the Nifty Fifty of the late 1960s and the high flying tech stocks of today.

comment by FCCC · 2022-01-21T15:16:01.186Z · LW(p) · GW(p)

I wrote something up a few months ago, predicting with 65% confidence that the S&P 500 will drop below 3029 before July 16, 2022 [LW · GW]. I’m not a professional investor, so take it with a grain of salt.

comment by arunto · 2022-01-08T14:11:51.537Z · LW(p) · GW(p)

(I know the charts are too small but I haven't figured out yet how to adjust the size of the charts in the editor).

Replies from: maxwell-peterson↑ comment by Maxwell Peterson (maxwell-peterson) · 2022-01-08T15:10:42.814Z · LW(p) · GW(p)

I’m not sure you can resize in the editor. If the image sizes on the sites you got them from are small by default, causing them to be small here, maybe zoom way in on the originals in your browser, screenshot them, and try re-uploading the resulting larger images?

Replies from: arunto↑ comment by arunto · 2022-01-08T15:25:09.526Z · LW(p) · GW(p)

Thanks. Resizing the image isn't a problem but how can I upload the resized image? If I click on the image icon in the editor I have to put in an URL.

Replies from: maxwell-peterson↑ comment by Maxwell Peterson (maxwell-peterson) · 2022-01-08T17:52:37.435Z · LW(p) · GW(p)

Huh. I just tried now and when I click the image icon in the editor it opens up my laptop's filesystem for me to choose an image. If you can't find that, it should also work to open the image file on your laptop, ctrl+A to select all of it, then ctrl+C to copy it, and you can paste it into the editor just like you'd paste text. That's how I usually enter images into posts

Replies from: arunto↑ comment by arunto · 2022-01-09T08:18:29.456Z · LW(p) · GW(p)

Thank you very much, now I have realized the problem.

For some reason I had activated the option "Restore the previous WYSIWYG editor". After unselecting that I can paste pictures into the editor (but I don't have to because the current editors automatically used the best size for the pictures).

Replies from: maxwell-peterson↑ comment by Maxwell Peterson (maxwell-peterson) · 2022-01-09T13:46:49.956Z · LW(p) · GW(p)

Great!

comment by [deleted] · 2022-01-09T19:29:44.596Z · LW(p) · GW(p)

Replies from: SimonM, arunto↑ comment by arunto · 2022-01-10T06:42:05.878Z · LW(p) · GW(p)

Am curious, are you suggesting any actionable trading strategy?

No, primarily I wanted to point out certain risk factors. The last sentence of my post was meant primarily as an illustration of the sentence before that.

d) sounds like you might be suggesting long vol, are you suggesting that?

Based on the risk factors stated above (but also based on the fact that overvaluations can be quite long lasting) I think most likely is one of two scenarios: A continued increase in the stock market based on the feeling of "there is no alternative" or a marked reduction of equity prices, so basically a bimodal distribution of expected returns.

Whether this is already priced in in the current option market I don't know. (And since I don't do short term trading I don't really care that much.) Without a specific prediction for the distribution of the expected returns (which I am unable to give above the more qualitative statement in the previous paragraph) I think it isn't possible to answer that.

Replies from: None