The Oil Crisis of 1973

post by Elizabeth (pktechgirl) · 2020-05-22T15:50:02.578Z · LW · GW · 10 commentsContents

10 comments

Last month I investigated commonalities between recessions of the last 50 years or so. But of course this recession will be different, because (among other things) we will simultaneously have a labor shortage and a lot of people out of work. That’s really weird, and there’s almost no historical precedent- the 1918 pandemic took place during a war, and neither 1957 nor 1968 left enough of an impression to have a single book dedicated to them.

So I expanded out from pandemics, and started looking for recessions that were caused by any kind of exogenous shock. The best one I found was the 1973 Oil Crisis. That was kicked off by Arab nations refusing to ship oil to allies who had assisted Israel during the Yom Kippur war- as close as you can get to an economic impact without an economic cause. I started to investigate the 1973 crisis as the one example I could find of a recession caused by a sudden decrease in a basic component of production, for reasons other than economic games.

Spoiler alert: that recession was not caused by a sudden decrease in a basic component of production either.

Why am I so sure of this? Here’s a short list of little things,

- The embargo was declared October 17th, but the price of oil did not really spike until January 1st.

- The price of food spiked two months before the embargo was declared and plateaued before oil prices went up.

- A multiyear stock market crash started in January 1973, 9 months before embargo was declared.

- Previous oil embargoes had been attempted in 1956 and 1967, to absolutely no effect.

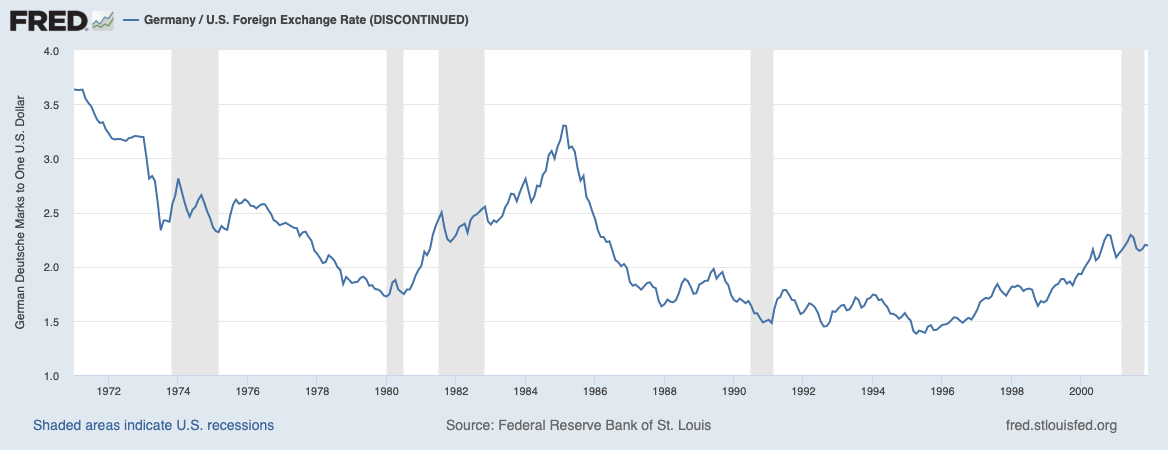

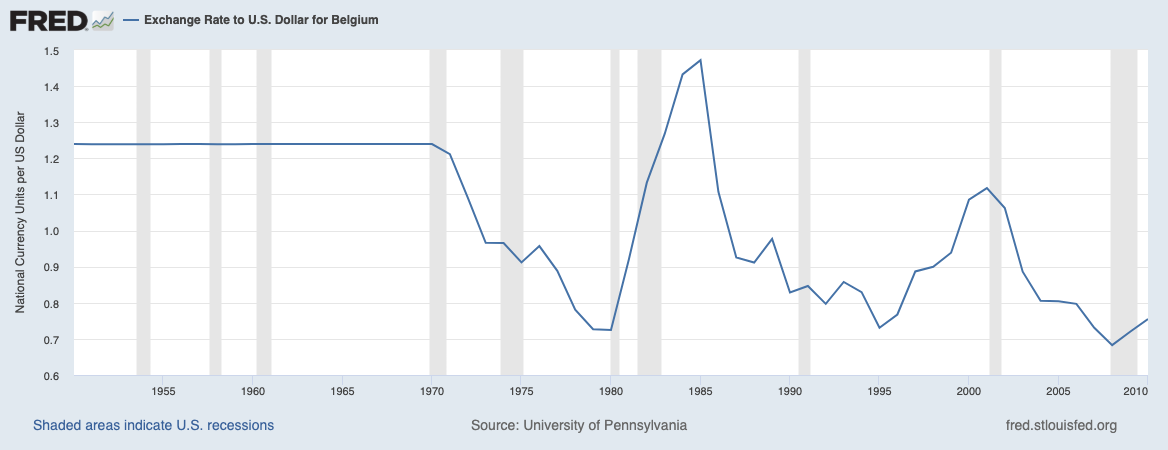

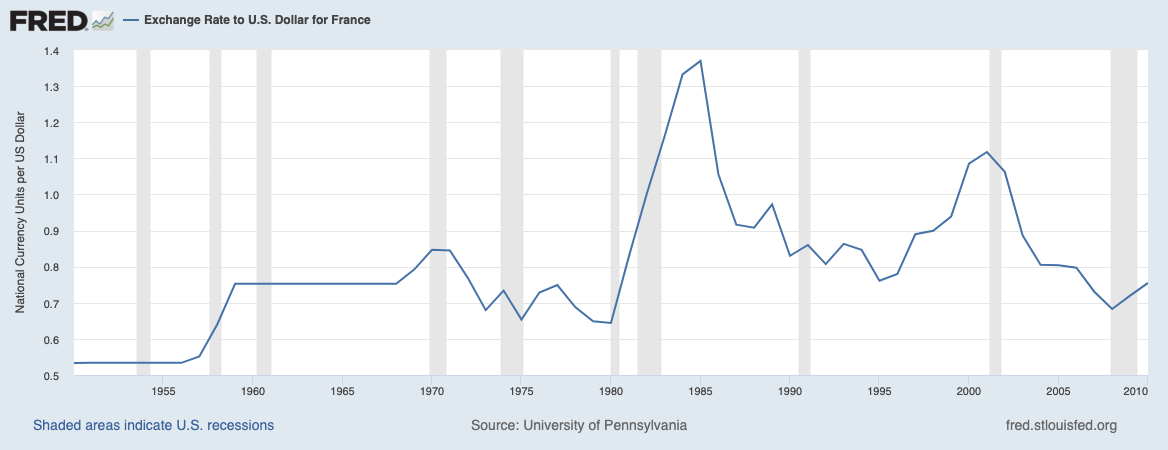

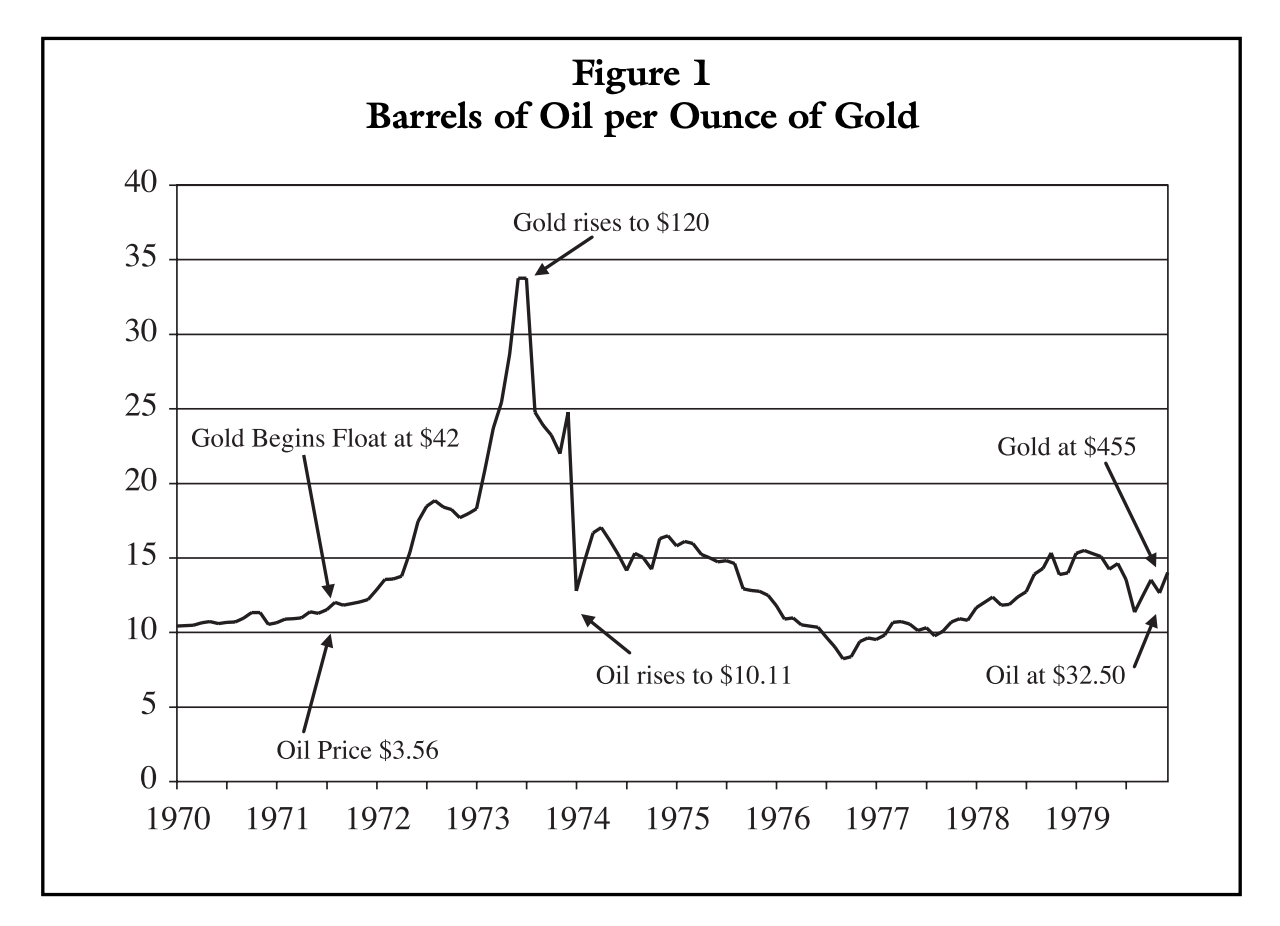

But here’s the big one: we measure the price of oil in USD. That’s understandable, since oil sales are legally required to be denominated in dollars. But the US dollar underwent a massive overhaul in 1971, when America decided it was tired of some parts of the Bretton Woods Agreement. Previously, the US, Japan, Canada, Australia and many European countries maintained peg (set exchange rate) between all other currencies and USD, which was itself pegged to gold. In 1971 the US decided not to bother with the gold part anymore, causing other countries to break their peg. I’m sure why we did this is also an interesting story, but I haven’t dug into it yet, because what came after 1971 is interesting enough. The currency of several countries appreciated noticeably (Germany, Switzerland, Japan, France, Belgium, Holland, and Sweden)…

(I apologize for the inconsistent axes, they’re the best I could do)

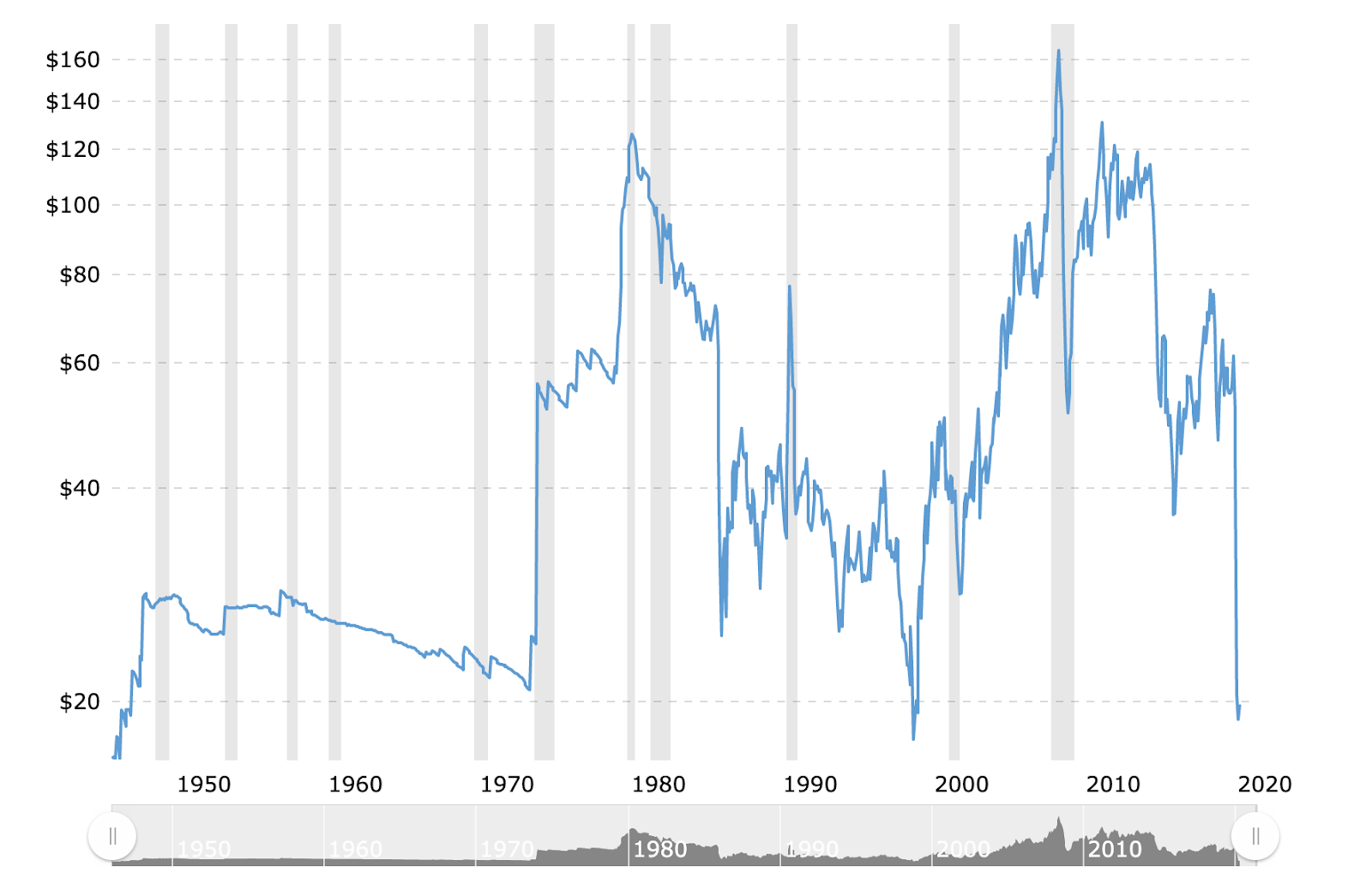

…but as I keep harping on, oil prices were denominated in dollars. This meant that oil producing countries, from their own perspective, were constantly taking a pay cut. Denominated in USD, 1/1/74 saw a huge increase in the price of oil. Denominated in gold, 1/1/74 saw a return to the historic average after an unprecedented low.

This is a little confusing, so here’s a timeline:

- 1956: Failed attempt at oil embargo

- 1967: Failed attempt at oil embargo

- 1971, August: US leaves the gold standard

- 1972: Oil prices begin to fall, relative to gold

- 1972, December: US food prices begin to increase the rate of price increases.

- 1973, January: US Stock market begins 2-year crash

- 1973, August: US food prices begin to go up *really* fast

- 1973, October, 6: Several nearby countries invade Israel

- 1973, October, 17: Several Arab oil producing countries declare an embargo against Israeli allies, and a production decrease. Price of oil goes up a little (in USD).

- 1974, January, 1: Effective date of declared price increase from $5.12 to $11.65/barrel. Oil returns to historically normal price measured in gold.

This is not the timeline you’d expect to see if the Yom Kippur war caused a supply shock in oil, leading to a recession.

My best guess is that something was going wrong in the US and world economy well before 1971, but the market was not being allowed to adjust. Breaking Bretton Woods took the finger out of the dyke and everything fluctuated wildly for a few years until the world reached a new equilibrium (including some new and different economic games).The Yom Kippur war was a catalyst or excuse for raising the price of oil, but not the cause.

Thanks to my Patreon subscribers for funding this research, and several reviewers for checking my research and writing.

10 comments

Comments sorted by top scores.

comment by A Kaleberg (a-kaleberg) · 2020-05-24T03:55:52.667Z · LW(p) · GW(p)

LBJ's guns (Vietnam) and butter (Great Society) were already causing a lot of inflationary pressure. Nixon imposed wage-price controls in 1971 around the time he took us off Bretton-Woods. I gather the Fed was raising interest rates, but not enough to slow an economy with that level of rising inflation. Wage price controls were considered, depending on your politics and probably the time of day, socialism or war-time measures. B-W was a good post-WWII idea that helped the post-war recovery, but as in the 1930s, gold standards never work as well in practice as they do in theory.

The 1973 oil shock was a real shock. Oil prices rose slowly thanks to future hedging and inventory. Gas prices didn't rise all of a sudden. They crept up, but availability became spotty. People got nervous and topped up more often, kind of like toilet paper more recently, and for similar reasons. People wanted a stash of their own rather than trusting the supply chain. (Should I mention Watergate here? It wasn't an economic thing, but it contributed to the sense of something being wrong. People had different sensibilities back then.)

The US had only started importing oil in 1968 or 1969. Before then, petroleum was local. Then came the embargo. I remember the gas lines, the odd-even day rationing and the general shock to the American way of life. The suburbs had been booming through the 1960s, and now, in the early 1970s, one had to look for a green or yellow flag to buy gasoline. Old timers remembered WWII rationing, but the US was much more car dependent in the 1970s. If nothing else, people suddenly had to evaluate their use of gasoline, much as one now has to assess one's risk of catching COVID-19.

In some ways the economy was pretty crappy in the 1970s, but if you were working, it was probably a high point. I remember reading the Middletown books on the 1920s and 1930s. The working and business class lived in two separate worlds. The former eked out a precarious living. The latter had a much bigger buffer and more opportunities. There was a followup study in the 1970s, Middletown Families, that pointed out that the divide between the working class - whites only - and the business class seemed to have vanished. Many more people were getting decent pay, benefits, comfy housing and so on. We've gone back to the 1920s pattern. You can call it the exempt / non-exempt divide or the working / business class divide, but that old gap has returned.

You are right that the economic slowdown wasn't just about the price of oil. There was a lot going on, and I haven't mentioned the baby boom yet. There was a big difference between being a boomer before 1955 - that's the usual year cited - and after 1964. The baby boom was a surprise in the 1940s and it built slowly. By 1972, the boomers were starting to saturate the economy, so I'm guessing there was demographic pressure as well. I'll leave that to Peter Turchin, but we've seen a lot more immiseration and elite competition - his terms - since then.

↑ comment by quanticle · 2020-05-25T04:47:19.175Z · LW(p) · GW(p)

I gather the Fed was raising interest rates, but not enough to slow an economy with that level of rising inflation.

The Fed, at the time, was not raising interest rates because it was thought that the political cost of a recession caused by raising interest rates would be too high. Nixon favored keeping interest rates low. Ford was basically a caretaker government. Carter appointed Paul Volcker as chairman of the Federal Reserve, in 1979. Volcker immediately raised the Fed funds rate to 20% to curb inflation. In the process, however, he triggered a short but deep recession which contributed to Carter being a one-term President, thus proving the point.

comment by Elizabeth (pktechgirl) · 2021-12-07T06:46:14.322Z · LW(p) · GW(p)

I did a lot of writing at the start of covid, most of which was eventually eclipsed by new information (thank God). This is one of a few pieces I wrote during that time I refer to frequently, in my own thinking and in conversation with others. The fact even very exogenous-looking changes to the economy are driven by economic fuckery behind the scenes was very clarifying for me in examing the economy as a whole.

comment by quanticle · 2020-05-23T15:10:37.234Z · LW(p) · GW(p)

My best guess is that something was going wrong in the US and world economy well before 1971, but the market was not being allowed to adjust.

The problem that made the Bretton Woods system unsustainable was the fiscal expansion caused by the US having to pay for the Vietnam War and the Great Society programs. From the linked article:

The Federal Reserve shifted its stance in the mid-1960s away from monetary orthodoxy in response to the growing influence of Keynesian economics in the Kennedy and Johnson administrations, with its emphasis on the primary objective of full employment and the belief that the Fed could manage the Phillips Curve trade-off between inflation and unemployment (Meltzer 2010).

Increasing US monetary growth led to rising inflation, which spread to the rest of the world through growing US balance of payments deficits. This led to growing balance of payments surpluses in Germany and other countries. The German monetary authorities (and other surplus countries) attempted to sterilise the inflows but were eventually unsuccessful, leading to growing inflationary pressure (Darby et al. 1983).

After the devaluation of sterling in November 1967, pressure mounted against the dollar via the London gold market. In the face of this pressure, the Gold Pool was disbanded on 17 March 1968 and a two-tier arrangement put in its place. In the following three years, the US put considerable pressure on other monetary authorities to refrain from converting their dollars into gold.

The decision to suspend gold convertibility by President Richard Nixon on 15 August 1971 was triggered by French and British intentions to convert dollars into gold in early August. The US decision to suspend gold convertibility ended a key aspect of the Bretton Woods system. The remaining part of the System, the adjustable peg disappeared by March 1973.

comment by Tim Liptrot (rockthecasbah) · 2020-06-01T15:40:45.200Z · LW(p) · GW(p)

Carbon Democracy by Timothy Mitchell provides another piece of the puzzle. The international oil companies took big hits to their margins as oil producers nationalized in the early 70's. Blaming the crisis on Arab politics allowed them to distract from the obscene margins they had previously been making. So they had an incentive to obfuscate what was really happening at OPEC, and the Saudi's at the time had no lobbyists to represent them in Washington.

comment by jmh · 2020-05-25T22:50:03.656Z · LW(p) · GW(p)

this recession will be different, because (among other things) we will simultaneously have a labor shortage and a lot of people out of work. That’s really weird, and there’s almost no historical precedent

Labor shortage and recession. It strikes me that perhaps WWII offers a similar setting. Massive labor shortage since many men were off fighting. A recession setting by a lot of metrics from a consumer demand and supply perspective -- so lots of rationing and the like.

Maybe some insights from analysis of those times?

comment by Sherrinford · 2020-05-23T13:39:14.879Z · LW(p) · GW(p)

May I ask how you define "labor shortage"? I think an economist would interpret this as firms looking for workers but being unable to get them (for the current wage). Is that really what is currently happening?

comment by jmh · 2020-05-23T16:25:05.062Z · LW(p) · GW(p)

I am pretty sure that the price of all goods started to fall relative to gold after the USA moved to a pure fiat money regime. If so do the gold price of oil itself informative or should one look to the relative price of oil (in what ever money units) to other goods or baskets of other goods.

Put a bit different, how was oil performing in the inflationary world?

comment by Sherrinford · 2020-05-23T13:47:05.603Z · LW(p) · GW(p)

In "neoclassical synthesis" terms, an oil shock is an aggregate-supply (AS) shock. If the aggregate-demand (AD) curve does not move, then an AS curve implies lower real GDP and a higher price level, whereas an AD shock that causes a recession implies lower real GDP and a lower price level. This is very simplistic, but may be helpful in structuring thoughts.

Also, maybe this is helpful information:

"All but one of the 11 postwar recessions" in the USA "were associated with an increase in the price of oil..."(exception: 1960).

11 of the 12 major oil price shocks that Hamilton identifies were accompanied by U.S. recessions (exception: "2003 oil price increase associated with the Venezuelan unrest and second Persian Gulf War.")

(Hamilton, 2011, Historical Oil Shocks, NBER working paper 16790)

But of course this alone doesn't say much about causality or effects.