Toward a Broader Conception of Adverse Selection

post by Ricki Heicklen (bayesshammai) · 2024-03-14T22:40:57.920Z · LW · GW · 61 commentsThis is a link post for https://bayesshammai.substack.com/p/conditional-on-getting-to-trade-your

Contents

Beware availability Alice’s Restaurant vs Bob’s Burgers The Parking Spot The Suspiciously Empty Subway Car The Thanksgiving Leftovers Beware models based on average values The Laffy Taffys MoviePass Beware market orders The Field Beware sophisticated opponents The Juggling Contest The Bedroom Allocation Beware beating the entire market The Wheelbarrow Auction The Wheelbarrow Auction, part 2 Beware the stock market Widgets, Inc None 61 comments

“I refuse to join any club that would have me as a member” -Marx[1]

Adverse Selection is the phenomenon in which information asymmetries in non-cooperative environments make trading dangerous. It has traditionally been understood to describe financial markets in which buyers and sellers systematically differ, such as a market for used cars in which sellers have the information advantage, where resulting feedback loops can lead to market collapses.

In this post, I make the case that adverse selection effects appear in many everyday contexts beyond specialized markets or strictly financial exchanges. I argue that modeling many of our decisions as taking place in competitive environments analogous to financial markets will help us notice instances of adverse selection that we otherwise wouldn’t.

The strong version of my central thesis is that conditional on getting to trade[2], your trade wasn’t all that great. Any time you make a trade, you should be asking yourself “what do others know that I don’t?” This does not mean that your trade is necessarily net bad, just that it is worse than it would have naively seemed before conditioning on having gotten to do the trade. The opportunity to trade is evidence that somebody else—in some cases, everybody else—passed over the decision to take that trade, or actively chose to take the other side of it.

This post is the first in a sequence on adverse selection, laying out my definition of the concept via a list of examples. The second post will discuss what factors determine the degree to which adverse selection is present in a given environment, and heuristics to detect them. The third will explore steps we can take to protect ourselves against adverse selection, as individuals and as a collective. The fourth will compare competitive and cooperative environments, the fifth will discuss a related claim that ambiguity obscures defection, and the sixth will connect to the concept of Goodharting and what levers of control we have over it.

Beware availability

When some options are taken and others are not, there may be a good reason for the difference in availability, even if that reason is not immediately obvious to you.

Alice’s Restaurant vs Bob’s Burgers

You’re on a road trip and passing through the exotic city of Teaneck, New Jersey, and decide to grab dinner at 7pm. The town has two diners: Alice’s Restaurant and Bob’s Burgers. From the outside, they look the same. Their menus are equally appealing. Since they seem tied on all other fronts, you default to alphabetical order, and go into Alice’s Restaurant. It’s packed to the brim, and you try to reserve a table, but they don’t have any openings for the next hour. So you go to Bob’s Burgers, order some food, and take a bite. The food is mediocre.

All else being equal, bad restaurants are more likely to have open tables than good restaurants. Alice's Restaurant and Bob's Burgers might look identical to you from the outside, but if all the tables at Alice's Restaurant are full and the tables at Bob's Burgers are open, that's evidence that Alice's Restaurant is better quality—and you'd rather eat there. Unfortunately for you, all the tables there are full, so you can't. The trades you get to do (eating at Bob's) are worse than the ones you don't (eating at Alice's).

That doesn't mean that eating at Bob's is worse than going hungry. It might still be worth buying food there instead of not at all. But next time, you might want to consider going at a less busy time, or making a reservation in advance.

The Parking Spot

Now that you’ve finished dinner, you continue on your road trip. Next stop: New York City. You begin the search for parking, and every spot seems to be taken. Each time you think you see a spot, there turns out to be a fire hydrant right next to it. You finally find an open spot in a convenient location, so you grab it. The next morning, you return and find a ticket on your car—apparently, Alternate Side Parking rules are in effect, something the locals all knew.

Without a story for why a parking spot in New York City hasn’t been taken, an opening should set off your alarms. My personal strategy to handle this is to drive around until I see someone pulling out of a spot—and then ask them why they’re leaving it, since parking spots are coveted resources not easily given up. Usually it’s because they have somewhere to be, and I can park comfortably knowing why the spot was free, but this has saved me from a ticket more than once when locals were pulling out only because Alternate Side Parking rules were about to go into effect.

The Suspiciously Empty Subway Car

Okay, to heck with cars, you decide to take the subway this time. You’re on the platform, and the train pulls into the station. Almost all of the subway cars are packed, but you notice one that is entirely empty. You’ll be able to get a seat! You step onto that car. The air conditioning is broken, and someone has defecated on the floor.

If it seems too good to be true, it might be because other subway riders know something you don’t. There’s a reason those seats are available—nobody else wants to be in that car. Unless you really don’t mind the heat and smell, you would have been better off boarding the busier car, and waiting for a seat to open at the next stop.

The Thanksgiving Leftovers

It’s the Sunday after Thanksgiving, and dinner is leftovers. You recall that your family’s Thanksgiving meal was delicious, so you’re excited to eat more of it. You get to the table, and find that you won’t be abel to get any meat—the only food left is Uncle Cain’s soggy fruit salad. All of the yummy food has disappeared over the weekend.

The best food at the Thanksgiving meal all got gobbled up on Thanksgiving. Of the leftovers, the better ones were eaten earlier in the weekend. The later you show up to Sunday night dinner, the worse the available options will be.

Beware models based on average values

If you model the world as providing you with a random sample, you’ll expect to get a better deal than if you correctly account for the fact that others have behaved and will behave in their own interest.

The Laffy Taffys

Laffy Taffys come in four flavors, three of which you really like. Your friend Drew is across the room next to the Laffy Taffy bowl, and you ask him to throw you a Laffy Taffy. (You don’t want to ask him for too big a favor, so you don’t specify flavor—you figure you’re 75% to get a good one anyway.) He reaches into the bowl and grabs a Laffy Taffy and tosses it to you. It’s Banana.

The mistake here is assuming that the Laffy Taffy is equally likely to be any of the four flavors. Laffy Taffys come in bags with equal distributions of the four flavors. If Drew drew from a brand new bag, you’d be 25% to get each of Sour Apple, Grape, Strawberry, or Banana. But he’s drawing from a bowl that people have been continuously taking Laffy Taffys out of. That means that you’re more than 25% to end up with Banana. (This is true even if there’s zero correlation between others’ preferences and your own, because you are one of the people who has been snacking on them.)

Ever wonder why the grapes at the end of the bowl are all squishy? It’s not only because they’ve been under the others (do grapes weigh enough for this to make a difference?). It’s also because the good ones get taken.

MoviePass

A typical moviegoer goes to the movie theaters less than once a month. The average price for a movie ticket is about $9. Here’s a business idea: charge users $10 a month for a service that gives them unlimited free tickets. What could go wrong?

Lowe dreaded the company's power users, those high-volume MoviePass customers who were taking advantage of the low monthly price, constantly going to the movies, and effectively cleaning the company out. According to the Motion Picture Association of America, the average moviegoer goes to the movies five times a year. The power users would go to the movies every day.

MoviePass users are selected for seeing a lot of movies. If MoviePass makes a business plan that models users as average people, it will lose a lot of money. Conditional on someone wanting to buy MoviePass, MoviePass probably should not want them as a customer.

Beware market orders

If you submit a market order (an order to buy or sell at the market's current best available price), you may get filled at a price that will make you unhappy.

The Field

You want to invest in real estate, so you go to your field-owning friend Ephron and submit a market order for his field.

You: I would like to buy your field.

Ephron: My man, it is all yours. Take it.

You: No, I want to pay dollars for it. I will pay whatever it costs. Which is how much, by the way?

Ephron: Oh, I guess, if I had to put a price on it, hrm, maybe $400 million? What’s $400 million between friends?

You: *gulp* Wow, that’s… a lot. I sure hope property value in this neighborhood rises over the next few thousand years. *hands over $400 million*

Ephrn: Thanks!

By giving Ephrn the option to sell the field to you at any price, you are opening yourself up to unlimited risk. He’s not going to choose a price that’s less than its true value, but he may choose a price that is more, potentially a lot more. Market orders are especially dangerous in illiquid markets, where there isn’t competition between providers. In this transaction, there was only one seller, so he got to set the price at whatever he wanted.

Never, ever, submit a market order in a competitive environment. You’re strictly better off submitting an IOC (immediate-or-cancel) limit order, i.e. an order which specifies the price above/below which you would not buy/sell.

I don't think this comes at the cost of much additional effort—I'm not advocating for calculating the exact EV, I'm claiming you are better off giving some limit, any limit (like, 2x, or even 10x, the price) than placing a true market order. This is pretty minimal extra effort for protecting you against various mistakes that will expose you to being adversely selected against—e.g. trading illiquid stock WDGT instead of the liquid stock WDGTS, in which you're not going to get filled at fair, you're going to get filled adversely at far higher prices in a market you did not intend to participate in and know nothing about.

If you’re worried about anchoring your counterparty to too high a number, as you might in the case of submitting a limit order with a high limit for a field purchase, you can write down your limit price and then still ask your counterparty to name a price, committing to only transact if it’s less than or equal to what you wrote down.

That said, I concede there are various situations, in particular cooperative interpersonal ones, where minimizing friction and signaling trust are valuable. It's probably pretty safe to say to a friend "can you grab me a banana from the store" (instead of "can you grab me a banana if and only if it costs less than $10") or "can you book a Lyft for me, I'll pay you back" (instead of "can you book a Lyft for me and I'll pay you back up to $500"). But even when you think you're in a cooperative environment, committing a potentially unbounded value ("we will reimburse travel costs") can result in counterparties optimizing on things they care about (comfort, convenience, the thrill of riding in a private jet) at the expense of your budget.

Beware sophisticated opponents

Know who you’re up against, what each of you are optimizing for (how correlated are your preferences?), and why they are taking their side of the trade.

The Juggling Contest

Your quantitative trading firm is holding its annual juggling tournament. Cost to enter is $18, winner takes all. You know you’re far better at juggling than most of your coworkers, so you sign up. As it turns out, only a few of your coworkers signed up, including Fortune, who used to be in the lucrative professional juggling world before leaving to pursue her lifelong passion of providing moderate liquidity to US Equities markets. You come in second place.

When signing up to compete in a zero-sum contest, assume your opponents are the best of the pool of possible competitors. They, too, had to run the mental exercise of “would I win my firm’s juggling contest?” You should have a story for why, despite that, you still think you’re likely to win.

You don’t have a way of knowing how good every single person at your firm is at juggling, so you need some algorithm for deciding whether you should compete. Say you have some juggling Elo score. One possible algorithm is “compete if and only if your Elo score is greater than or equal to 1600.”

Now, assume every person at the firm runs this algorithm to determine whether to compete. Here’s a strategy that dominates it: “Compete if and only if your Elo score is greater than or equal to 1601.” Why? Well, strategies A (>=1600) and B (>=1601) discriminate only in the event that your score is 1600. If everyone else follows strategy A, switching to strategy B either won’t affect whether you participate, or will cause you to not participate if your score is exactly 1600. In a world where all others use strategy A, you should prefer to not participate if your score is exactly 1600 (since at best, you tie in expectation). So if everyone is using A, you should switch from A to B. Your quantitative trading coworkers are also rational, so they will make the same switch.

Strategy A can only beat B if you have reason to believe that other people have lower thresholds than 1600 (in which case inclusion for 1600 may be positive). But someone in the pool has the lowest threshold, and that person would strictly improve by raising their threshold until it exceeds the second lowest participant’s. The person with the lowest threshold is making a mistake.[3] You should have a story for why you think that person isn’t you.

The Bedroom Allocation

You’re moving into a two-bedroom apartment with your roommate Grant. Grant was the one to find the apartment, and he gave you a virtual tour over zoom while he was there. You both like the apartment, so you put down a deposit. Now it’s time to decide on bedrooms, and Grant asks your preferences—if you both prefer the same room, you’ll rock-paper-scissors for it. Both rooms looked equally good to you on the zoom call, so you tell him that you’re indifferent. Grant chooses a room, and lo and behold, you find upon moving in that your room has less closet space and worse flooring. You feel a little crummy about the new arrangement.

Grant had information that you didn’t have, since he was able to see the room more clearly on his visit. Given the information gap, is there anything you could have done differently?

Here’s a strategy: instead of expressing indifference, you could have flipped a coin and chosen a room preference at random. This would have given you a 50% chance of selecting the better room (in which case you rock-paper-scissors), and a 50% chance of selecting the worse room. In all, that gives you a 25% chance of getting the better room. By leaving it up to Grant, you gave yourself a 0% chance of getting the better room.

Of course, there are a bunch of assumptions baked into this: that you and Grant have correlated preferences (generally true, but not always), that you prefer to maximize your own utility as opposed to the sum of both of your utilities, that you wouldn’t pay substantial social costs in the roommate dynamic as a result of doing something insane and cutthroat by normal-people-standards, et cetera. But there are many cases in which these assumptions do hold, so keeping a coin on you in case of emergency might pay dividends.

Beware beating the entire market

If you are in a liquid market and nevertheless you get to do a trade, you should wonder why nobody else wanted it.

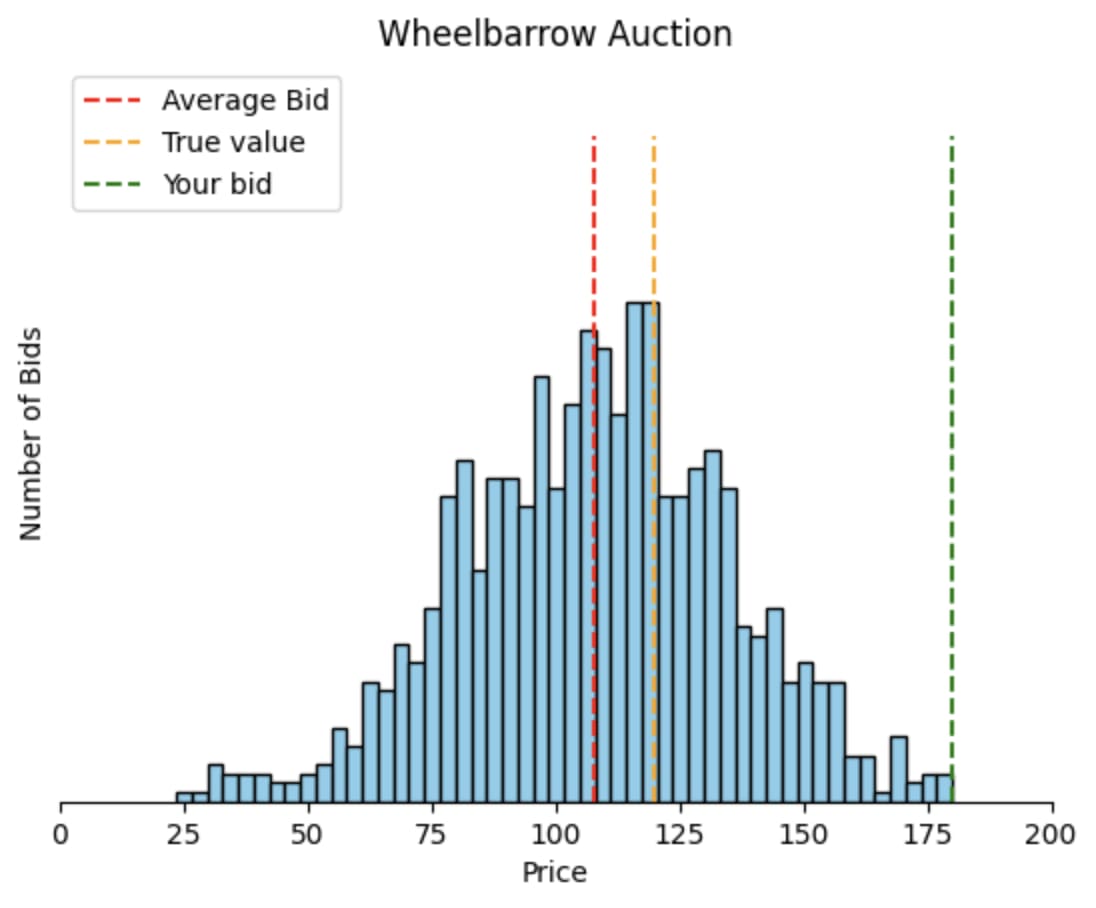

The Wheelbarrow Auction

This is an illustration of the winner’s curse.

At the town fair, a wheelbarrow is up for auction. You think the fair price of the wheelbarrow is around $200 (with some uncertainty), so you submit a bid for $180. You find out that you won the auction—everyone else submitted bids in the range of $25-$175, so your bid is the highest. After paying and taking your new acquisition home, you discover that the wheelbarrow is less sturdy than you’d estimated, and is probably worth more like $120. You check online, and indeed it retails for $120. You would have been better off buying it online.

Conditional on having won the auction, you outbid every single other participant. You are at the extreme tail of bids. The price you bid ($180) is a combination of your model of the wheelbarrow's price ($200, with some uncertainty) and the amount of edge you ask for to account for the winner's curse (10%, or $20).

If you are the winner, it means everybody else either models the price as lower, or asks for greater edge (i.e., adjusts down by a larger factor—in this case, I modeled everyone as adjusting down 10%, but adding noise to the adjustment factor is a better model that does not change the underlying effect), or some blend of the two.

If it's just because they're asking for a lot more edge, your bid could still be profitable in expectation. But it's likely some combination of the two, and the fact that their price models are all (or almost all) lower than yours should cause you to update that the true value of the wheelbarrow is lower than you'd previously estimated.

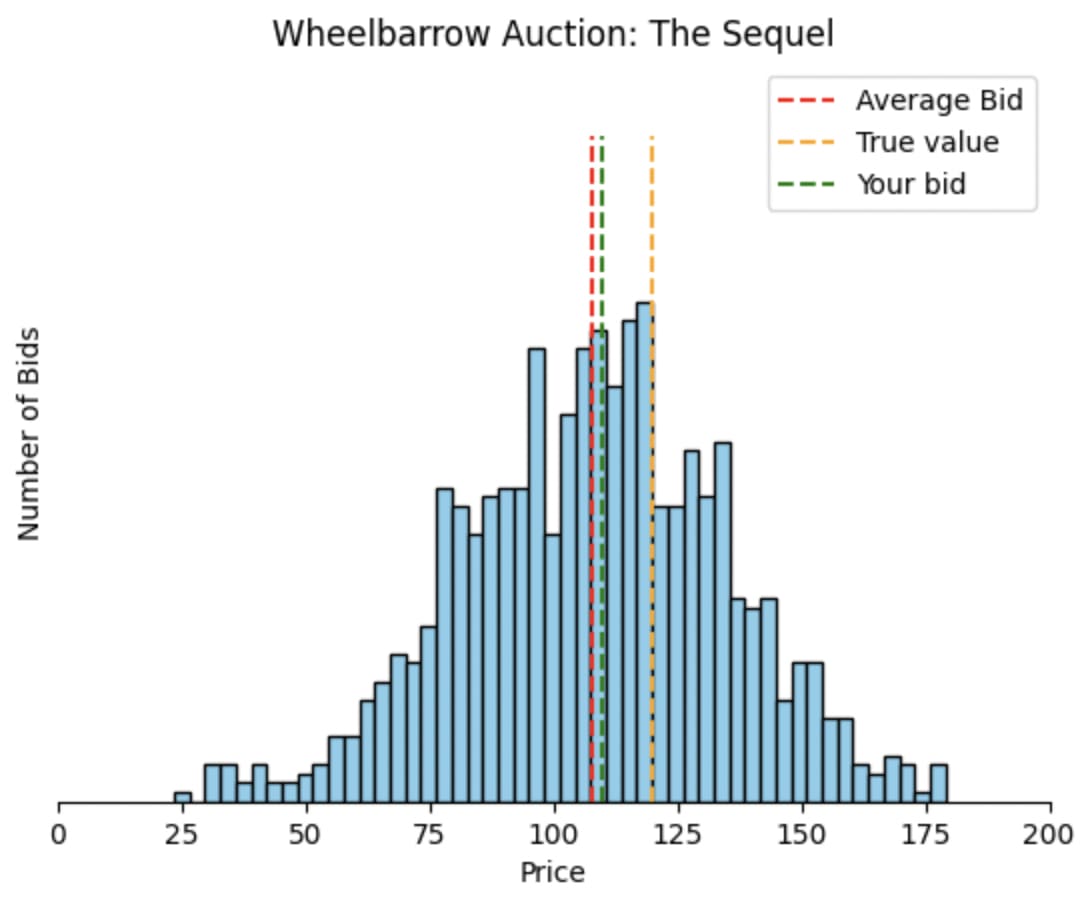

The Wheelbarrow Auction, part 2

At the town fair, a wheelbarrow is up for auction. You think the fair price of the wheelbarrow is around $120 (with some uncertainty), so you submit a bid for $108. You find out that you didn’t win—the winning bidder ends up being some schmuck who bid $180. You don’t exchange any money or wheelbarrows. When you get home, you check online out of curiosity, and indeed the item retails for $120. Your estimate was great, your bid was reasonable, and you exchanged nothing as a result, reaping a profit of zero dollars and zero cents.

In the previous example, your model was bad, you overestimated the true value, and as a result you lost money. In this example, your model was good—but you don’t profit, because you don’t end up winning the auction. There's an asymmetry between your profits when your model is correct and your losses when it is incorrect.

(Your model could also be bad in the downwards direction, and you think the wheelbarrow is worth a lot less, e.g. $25. In this case, you also don’t win the wheelbarrow, so your profit is $0.)

If the pool of bidders were much smaller, or their models were systematically biased downwards, or if they were more risk averse and asked for much more edge and as a result the worlds in which you outbid them but still profit outweigh worlds where you overshot, or if all the bidders agreed to collude and stuck to their agreement, or if you have sufficient reason to believe your model is extremely accurate (and theirs are not), you can still make money in an auction of this form. But your strong prior should be that you will not.

Beware the stock market

Only send orders that you would be happy with conditional on getting filled.

Widgets, Inc

Your local Widgets factory is rumored to have an upcoming merger. If the merger goes through, the stock will be worth $100. If it doesn’t, it’ll tank down to $0. Historically, you know that 80% of rumored mergers end up going through, so you believe that stock in Widgets Inc. should be worth $80.

As a result, you put out two orders in the market for WDGTS: a bid to buy the stock for $79 and an offer to sell the stock at $81. Both of these orders are good to your best estimate of the stock’s true value: if somebody traded with you at random, you’d make a dollar in expectation (either you buy stock worth $80 for a price of $79, or you sell stock worth $80 at a price of $81).

But other people are not trading with you at random—conditional on somebody trading with you, they believe it is profitable for them to do so. They will only buy from you for a price of $81 if their model says the stock is worth more than $81. Maybe they’ve read the Widgets Inc. prospectus, maybe they factored in demand for widgets this season, maybe they just tried to estimate the percentage of rumored mergers that end up going through, but they used a different historical dataset from yours and got 85%, and as a result believe the deal is 85% to go through.

If you know that they think the deal is 85% to go through, you should probably update your model in light of theirs. You should now think the deal is somewhere between 80% and 85% to go through. It might be 82.5%, it might be 80.1%, it might be 84.9%. For any of these, though, your $81 sale is worse than if the probability were truly 80%, your original best estimate. Once you know that, you should expect to make less than $1 in expected profit and reconsider what trades you want to do.

But, importantly, you only find out that they think your model is wrong once they trade with you—they don’t want to tell you if they could just make money off you instead! In worlds where Widgets stock is really worth more than $80, traders are more likely to buy from you. In worlds where Widgets stock is really worth less than $80, traders are more likely to sell to you. Conditional on one of your orders getting filled, your model of the world shifts in the direction that makes your trade less profitable than your old model would have predicted.

If someone buys from you for $81, you should not think “Great, I just made a dollar in expectation, I’m going to try to do the same trade again and see if someone else will also buy for $81!” You should think, “I wonder what they know that I don’t—it’s probably worth more than $80.”

- ^

Groucho Marx, specifically.

- ^

I will use the word “trade” expansively throughout to include any decision, agreement, plan, exchange, or the like that takes place in a competitive environment.

- ^

Alternatively, they’re paying money in expectation for the thrill of competitive juggling. That’s a fine utility function for them to have (people trade money for enjoyment all the time), and if you think others are doing this, there’s your story for why you should participate. Or you might be the juggling enjoyer—by all means, pay dollars to toss balls in the air for sport. This is normal and fine and a story (the most charitable story) for why casinos are in business.

61 comments

Comments sorted by top scores.

comment by Ricki Heicklen (bayesshammai) · 2024-03-16T00:21:52.148Z · LW(p) · GW(p)

In response to various [LW(p) · GW(p)] comments [LW(p) · GW(p)], I've edited this post to change the title, clarify my fundamental thesis and some terminology choices, and provide explanations for each example. I apologize if this makes some of the existing comments confusing; for posterity, the original version is here.

The high level changes:

- I changed the title from "Conditional on Getting to Trade, Your Trade Wasn’t All That Great" to "Toward a Broader Conception of Adverse Selection," since I think the former was distracting from the substance of the piece and led to people believing I think trades cannot be positive sum. Thanks in particular to @Thomas Kwa [LW · GW] for the gentle advice to change it.

- I added in an introductory section defining adverse selection, motivating the piece, clarifying some misconceptions, and providing a roadmap for the next posts in the sequence.

- I reordered the examples and added section headers. The divisions aren't perfect, there's overlap between them, but hopefully this adds some clarity.

- Because of the reordering, some of the comments referring to examples by number might not make sense. The original numbering was:

- 1: The Subway Seat

- 2: The Juggling Contest

- 3: The Bedroom Allocation

- 4: The Thanksgiving Leftovers

- 5: The Wheelbarrow Auction

- 6: The Wheelbarrow Auction pt 2

- 7: The Laffy Taffys

- 8: The Field

- 9: The Parking Spot

- 10: MoviePass

- 11: Widgets Inc.

- Because of the reordering, some of the comments referring to examples by number might not make sense. The original numbering was:

- I explained each section with 1-2 sentences, and added explanations for ~all of the examples.

- I added the example "Alice’s Restaurant vs Bob’s Burgers," adapted from a comment I wrote.

- I included various strategies for combating adverse selection in specific scenarios. I feel conflicted about this, since I'm worried the strategies will distract from the examples and also be redundant with a lot of the content in the second post, but I think this was the right call to help motivate why paying attention to these effects can be useful.

- I changed a couple of the names

- I added a few footnotes

I refuse to remove the Karl/Groucho Marx joke.

comment by quanticle · 2024-03-15T01:25:22.249Z · LW(p) · GW(p)

I don't think the Widgets Inc. example is a good one. Michael Lewis has a good counterpoint in The Big Short, which I will quote at length:

The alarmingly named Avant! Corporation was a good example. He [Michael Burry] had found it searching for the word "accepted" in news stories. He knew, standing at the edge of the playing field, he needed to find unorthodox ways to tilt it to his advantage, and that usually meant finding situations the world might not be fully aware of. "I wasn't looking for a news report of a scam or fraud per se," he said. "That would have been too backward-looking, and I was looking to get in front of something. I was looking for something happening in the courts that might lead to an investment thesis." A court had accepted a plea from a software company called the Avant! Corporation. Avant! had been accused of stealing from a competitor the software code that was the whole foundation of Avant!'s business. The company had $100 million cash in the bank, was still generating $100 million a year of free cash flow -- and had a market value of only $250 million! Michael Burry started digging; by the time he was done, he knew more about the Avant! Corporation than any man on earth. He was able to see that even if the executives went to jail (as they did) and the fines were paid (as they were), Avant! would be worth a lot more than the market then assumed. Most of its engineers were Chinese nationals on work visas, thus trapped -- there was no risk that anyone would quit before the lights were out. To make money on Avant!'s stock, however, he'd probably have to stomach short-term losses, as investors puked up shares in horrified response to negative publicity.

Burry bought his first shares of Avant! in June 2001 at $12 a share. Avant!'s management then appeared on the cover of Business Week, under the headline, "Does Crime Pay?" The stock plunged; Burry bought more. Avant!'s management went to jail. The stock fell some more. Mike Burry kept on buying it -- all the way down to $2 a share. He became Avant!'s single largest shareholder; he pressed management for changes. "With [the former CEO's] criminal aura no longer a part of operating management," he wrote to the new bosses, "Avant! has a chance to demonstrate its concern for shareholders." In August, in another e-mail, he wrote, "Avant! still makes me feel I'm sleeping with the village slut. No matter how well my needs are met, I doubt I'll ever brag about it. The 'creep' factor is off the charts. I half think that if I pushed Avant! too hard I'd end up being terrorized by the Chinese mafia." Four months later, Avant! got taken over for $22 a share.

Why should Michael Burry have assumed that he had more insight about Avant! Corporation than the people trading with him? When all of those other traders exited Avant!, driving its share price to $2, Burry stayed in. Would you have? Or would you have thought, "I wonder what that trader selling Avant! for $2 knows that I don't?"

Replies from: thomas-kwa, interstice↑ comment by Thomas Kwa (thomas-kwa) · 2024-03-15T05:20:54.814Z · LW(p) · GW(p)

Or would you have thought, "I wonder what that trader selling Avant! for $2 knows that I don't?"

The correct move is to think this, but correctly conclude you have the information advantage and keep buying. Adverse selection is extremely prevalent in public markets so you need to always be thinking about it, and as a professional trader you can and must model it well enough to not be scared off of good trades.

Replies from: quanticle↑ comment by quanticle · 2024-03-15T14:28:54.198Z · LW(p) · GW(p)

That point is contradicted by the wheelbarrow examples in the OP, which seem to imply that either you'll be the greater fool or you'll be outbid by the greater fool. Why wasn't Burry outbid by a fool who thought that Avant! was worth $40 a share?

This is why I disagree with the OP; like you, I believe that it's possible to gain from informed trading, even in a market filled with adverse selection.

Replies from: thomas-kwa, CronoDAS↑ comment by Thomas Kwa (thomas-kwa) · 2024-03-15T18:21:31.879Z · LW(p) · GW(p)

OP was a professional trader and definitely (98%) agrees with us. I think the (edit: former) title is pretty misleading and gives people the impression that all trades are bad though.

↑ comment by interstice · 2024-03-15T14:23:54.652Z · LW(p) · GW(p)

Why should Michael Burry have assumed that he had more insight about Avant! Corporation than the people trading with him?

Because he did a lot of research and "knew more about the Avant! Corporation than any man on earth"? If you have good reason to think that you're the one with an information advantage trades like this can be rational. Of course it's always possible to be wrong about that, but there are enough irrational traders out there that it's not ruled out. Also note that it's not actually needed that your counterparties are irrational on average, it's enough that there are irrational traders somewhere in the broader ecosystem, as they can "subsidize" moderately-informed trading by others(which you can take advantage of in individual cases)

Replies from: quanticle↑ comment by quanticle · 2024-03-15T23:00:56.440Z · LW(p) · GW(p)

The second wheelbarrow example has a protagonist who knows the true value of the wheelbarrow, but still loses out:

At the town fair, a wheelbarrow is up for auction. You think the fair price of the wheelbarrow is around $120 (with some uncertainty), so you submit a bid for $108. You find out that you didn’t win—the winning bidder ends up being some schmuck who bid $180. You don’t exchange any money or wheelbarrows. When you get home, you check online out of curiosity, and indeed the item retails for $120. Your estimate was great, your bid was reasonable, and you exchanged nothing as a result, reaping a profit of zero dollars and zero cents.

But, in my example, Burry wasn't outbid by "some schmuck" who thought that Avant! was worth vastly more than it ended up being worth. Burry was able to guess not just the true value of Avant!, but also the value that other market participants placed on Avant!, enabling him to buy up shares at a discount compared to what the company ended up selling for.

The implied question in my post was, "How do you know if you're Michael Burry, or the trader selling Avant! shares for $2?"

comment by gwern · 2024-03-14T23:49:45.858Z · LW(p) · GW(p)

Counterpoint: actually, you're wrong, because most trades I make IRL leave me with a lot of consumer surplus, and in reality, conditional on me making a trade, it was pretty good.

The fact that you have to reach for exotic scenarios either involving government failures like subways or doing limit orders in highly efficient markets for financial speculation on liquid but volatile assets (not exactly an everyday 'trade' I hope you'll concede) or contests or auctions by naive non-auction goers who don't even know to account for winner's curse or getting stuff for free should make you rethink what you are claiming about "most trades you make aren't all that great".

If your point was true, it should be as simple as "you go into the grocery store to buy a gallon of milk. You are filled with deep remorse and shame when you get home and look at the receipt and think about how much you spent in gas to boot. You look in your freezer for comfort. You are filled with deep remorse and shame when you are reminded how much you paid for the ice cream. With little choice, you pull out a spoon you bought years ago - and are filled with deep remorse and shame &etc &etc". You wouldn't need to invoke all these weird hypotheticals like "you ask your friend Drew to sell you under the table a cheap limited share of his cow's monthly milk production in ice cream tickets through your company redeemable in NYC but only in an office which can be reached by an express subway (which runs on alternate Tuesdays)"...

Replies from: bayesshammai, interstice, habryka4, bayesshammai, OldManNick↑ comment by Ricki Heicklen (bayesshammai) · 2024-03-15T00:46:19.275Z · LW(p) · GW(p)

I don't claim here that all trades you get to do are bad. I claim that they're worse than they might naively seem without accounting for adverse selection, i.e. for the fact that your opportunity to get something depends on nobody else wanting it (as in the case of the subway seat or the parking spot) or somebody else actively wanting the other side of the trade (as in the case of the zero-sum bedroom selection or the juggling contest).

I'm surprised that these are exotic scenarios to you. I regularly take the subway. I might not be understanding the relevance of subways as an example of "government failure," but I'll rephrase the example without needing to invoke a government resource:

1. The Restaurant Seat: You’re in a food court at dinnertime. Almost all of the restaurants are full to the brim, and don't have any tables available, but you notice one that is entirely empty. You’ll be able to get a table! You enter the restaurant, order your food, and take a bite. The food is mediocre.

Bad restaurants are more likely to have open tables than good restaurants. Alice's Restaurant and Bob's Burgers might look identical to you from the outside, but if all the tables at Alice's Restaurant are full and the tables at Bob's Burgers are open, that's evidence that Alice's Restaurant is better quality—and you'd rather eat there. Unfortunately for you, all the tables there are full, so you can't. The trades you get to do (eating at Bob's) are worse than the ones you don't (eating at Alice's).

That doesn't mean that eating at Bob's is worse than going hungry. It might still be worth buying food there instead of not at all. But, if a week ago you had had the opportunity to make a reservation at either one (before Alice's filled up), you would have been better off flipping a coin and reserving one at random than waiting to slot into whichever is available.

Does this help clarify the confusion? If so, I'll edit in this example, so as to not have the government goods degrading element distract from the core idea.

Replies from: TsviBT↑ comment by TsviBT · 2024-03-15T01:49:29.789Z · LW(p) · GW(p)

Bad restaurants are more likely to have open tables than good restaurants.

That seems dependent on it being difficult to scale the specific skill that went into putting together the experience at the good restaurant. Things that are more scalable, like small consumer products, can be selected to be especially good trades (the bad ones don't get popular and inexpensive).

Replies from: Augustin Portier↑ comment by TeaTieAndHat (Augustin Portier) · 2024-03-15T16:44:29.495Z · LW(p) · GW(p)

I agree. Another way to say that is that if there’s competition for the good you want (because it’s in some way or other in limited supply—seats in the subway, shares in a specific company, pieces of candy of the flavor you like, …— and you win the competition too easily, you have to check you aren’t being screwed. But if the good is mass-produced to the point where you‘re not clearly competing with others for it, then there’s no reason to wonder why others are letting you win?

↑ comment by interstice · 2024-03-15T02:43:22.142Z · LW(p) · GW(p)

An amended slogan that more accurately captures the phenomenon the post is trying to point to would be "Conditional on your trade seemingly not creating value for your counterparty, your trade likely wasn't all that good".

Replies from: nathan-helm-burger↑ comment by Nathan Helm-Burger (nathan-helm-burger) · 2024-03-15T17:24:06.563Z · LW(p) · GW(p)

Yes! The real moral of this story is that trades which seem like win-win are a better bet, since you understand what the other party is gaining from them. Trades which seem too-good-to-be-true and purely win-lose in your favor should strike you as suspicious. You should only engage in such trades when you are confident you have an information advantage.

I think this important point is obscured by a number of bad examples lumping in other, less related phenomena that have different 'solutions'. The unifying theme might be, 'make sure you have enough information to determine that the trade is good before going through with it.' I still think that there are different patterns here that deserve to be categorized separately.

↑ comment by habryka (habryka4) · 2024-03-15T00:01:22.214Z · LW(p) · GW(p)

I think this post is just trying to be a set of examples of adverse selection, not really some kind of argument that there is tons of adverse selection everywhere. Lists of examples seem useful, even if they are about phenomena that are not universally present, or require specific environmental circumstances to come together in the right way.

Replies from: None, gwern↑ comment by [deleted] · 2024-03-16T00:38:48.148Z · LW(p) · GW(p)

I don't think any of these examples are examples of adverse selection because they generate separating equilibria prior to the transaction without any types dropping out of the market, so there's no social inefficiency.

Insurance markets are difficult (in the standard adverse selection telling) because insurers aren't able to tell which customers are high risk vs low risk, and so offer prices for the average of the two, leading to the low-risk types dropping out because the price is more than they're willing to pay. I think this formal explanation is good https://www.kellogg.northwestern.edu/faculty/georgiadis/Teaching/Ec515_Module14.pdf

I think this post makes an important point, that it's important to take conditional expectations, where one is conditioned on being able to make a trade, but none of this is adverse selection, which is a specific type of dynamic Bayesian game that leads to socially inefficient outcomes which isn't a property of dynamic bayesian games in general.

↑ comment by gwern · 2024-03-15T00:08:50.496Z · LW(p) · GW(p)

But the framing here is completely wrong...

But OK, let's leave aside the title and attempt to imply anything about 99% of trades out there, or the basically Marxist take on all exchanges being exploitation and obsession with showing how you are being tricked or ripped off. The examples are still very bad and confused! Like, these examples are not even all about adverse selection, and several of them are just wrong in portraying the hypothetical as a bad thing.

The first one about subways, isn't even about adverse selection to begin with. A reminder of what "Adverse selection" is:

In economics, insurance, and risk management, adverse selection is a market situation where buyers and sellers have different information. The result is the unequal distribution of benefits to both parties, with the party having the key information benefiting more.

In the subway example, there is no different information: it's about how governments do rationing and make markets clear by letting the goods degrade until the utility is destroyed because of lack of appetite for setting clearing prices like surge prices or fare enforcement; that's not 'adverse selection' at all, any more than freeways reaching an equilibrium of misery where they are so slow that people avoid them is 'adverse selection'. (If you think it's 'adverse selection', explain what "buyers and sellers have different information" means in the context of lack of congestion pricing in transport...?)

#3 and #4 are not adverse selection either (still no difference in information), and are fundamentally wrong in portraying it as a bad outcome: the outcomes are not bad, but neutral or good - OP gives no reason to think that the outcomes would have been better if 'you' had gotten the good room or to eat whichever dish. (In fact, presumptively, those are the desirable outcomes: if 'you' cared so much, why did you leave it up to Bob; and why did you not eat the dish yourself, but someone hungrier did?)

#6 doesn't demonstrate anything because no trade happened, so it can't show anything about your surplus from trades that do happen.

And the Wall Street efficient market examples are true (finally, an actual adverse selection example!), but relevant to vanishingly few people who are also extremely aware of it and spend a lot of effort dealing with it, generally successfully; and people who do auctions more than occasionally generally do not have any problem with winner's curses, and auctions are widely & intensively used in many fields by experts. And so on.

Replies from: habryka4, habryka4, wowsuch↑ comment by habryka (habryka4) · 2024-03-15T01:43:29.172Z · LW(p) · GW(p)

But OK, let's leave aside the title and attempt to imply anything about 99% of trades out there, or the basically Marxist take on all exchanges being exploitation and obsession with showing how you are being tricked or ripped off.

My guess is you are pattern-matching this post and author to something that I am like 99% confident doesn't match. I am extremely confident the author does not think remotely anything like "all exchanges [are] exploitation" or has a particular obsession with being tricked or ripped off (besides a broad fascination with adverse selection in a broad sense).

Replies from: Benito↑ comment by Ben Pace (Benito) · 2024-03-15T01:59:30.302Z · LW(p) · GW(p)

(And in case anyone was led astray: the Marx quote at the start is from Groucho, not Karl.)

Replies from: jmh↑ comment by jmh · 2024-03-15T16:27:35.548Z · LW(p) · GW(p)

I thought it an odd quote for Karl but didn't give much thought after that. However, with this information I have to wonder if the choice to obscure the actual person being quoted was not intnetional to make some type of point related to the post.

Replies from: Benito↑ comment by Ben Pace (Benito) · 2024-03-15T18:48:23.092Z · LW(p) · GW(p)

I think it is pretty obviously a joke :P

Replies from: jmh↑ comment by jmh · 2024-03-16T03:46:40.224Z · LW(p) · GW(p)

Equally obvious that it went right over my head.

Still, seems like the aobe reference to marxist views on market trades seems to illustrate another way information asymmetry/advers selection plays out. I was just wondering if that was the intent when the first name was placed in the footnote rather than in the attribute for the quote.

But I have been accused of being humor challenged before ;-) -- or perhaps I should say demonstrated my humor disability?

↑ comment by habryka (habryka4) · 2024-03-15T00:23:42.750Z · LW(p) · GW(p)

I think all of them follow a pattern of "there is a naive baseline expectation where you treat other people's maps as a blackbox that suggest a deal is good, and a more sophisticated expectation that involves modeling the details of other people's maps that suggests its bad" and highlights some heuristics that you could have used to figure this out in advance (in the subway example, a fully empty car does indeed seem a bit too good to be true, in the juggling example you do really need to think about who is going to sign up, in the bedroom example you want to avoid giving the other person a choice even if both options look equally good to you, in the Thanksgiving example you needed to model which foods get eaten first and how correlated your preferences are with the ones of other people, etc.).

This feels like a relatively natural category to me. It's not like an earth-shattering unintuitive category, but I dispute that it doesn't carve reality at an important joint.

Replies from: gwern↑ comment by gwern · 2024-03-15T00:32:25.395Z · LW(p) · GW(p)

I think all of them...that suggests its bad

They don't. As I already explained, these examples are bad because the outcomes are not all bad, in addition to not reflecting the same causal patterns or being driven by adverse selection. The only consistent thing here is a Marxian paranoia that everyone else is naive and being ripped off in trades. Which is a common cognitive bias in denying gains to trade. The subway car is simply an equilibrium. You cannot tell if 'you' are better off or worse off in any car, so it is not the case that 'the deal is bad' The room and food examples actually imply the best outcome happened, as the room and food went to those who valued it more and so ate it sooner (it's not about correlation of preferences, it's about intensity); the deal was good there. And the Laffy Taffy example explicitly doesn't involve anything like that but is pure chance (so it can't involve "other people's maps" or 'adverse selection').

Replies from: CronoDAS↑ comment by CronoDAS · 2024-03-15T05:21:00.728Z · LW(p) · GW(p)

I think you missed the point of the Laffy Taffy example. He got the flavor he didn't like because he'd been systematically eating the ones he did like while leaving the flavor he didn't like in the bowl. (Or his friend wasn't actually picking at random.)

↑ comment by wowsuch · 2024-03-15T00:33:55.645Z · LW(p) · GW(p)

I think you might be slightly misunderstanding the intention of the subway example (1.) - the "market" described is one of commuters for seats, and the example is noting that if some subway seats appear underpriced -- i.e. commuters are choosing to cram together in fewer cars rather than equalizing their density over all available subway cars -- then those commuters likely know something about the unused seats that you don't know.

↑ comment by Ricki Heicklen (bayesshammai) · 2024-03-15T03:39:04.200Z · LW(p) · GW(p)

The fact that you have to reach for exotic scenarios ... [such as] auctions by naive non-auction goers who don't even know to account for winner's curse or getting stuff for free should make you rethink what you are claiming about "most trades you make aren't all that great".

The thing I'm describing here is winner's curse—my point is that the winning bidder (in example #5) overpays relative to the true value, while the median bidder (in example #6) neither profits nor loses. (A bidder whose model is mistaken such that they substantially underbid also profits $0). That is, there's an asymmetry between your PnL when your model is correct (#6) and when your model is incorrect (#5).

Some auction goers know about winner's curse; they likely make more conservative bids to protect against this. Some auction goers don't. The person winning the auction is more likely to not be thinking hard about winner's curse, or to have a sufficiently wrong pricing model to counteract the size of their adjustment in light of it.

The point is: conditional on winning the auction, you outbid every other person. You are at the extreme end of bids. The price you bid ($180) is a combination of your model of the wheelbarrow's price ($200, with some uncertainty) and the amount of edge you ask for on account of winner's curse concerns (10%, or $20). If you are the winner, it means everybody else either models the price as lower, or asks for greater edge, or (most likely) some blend of the two. If it's just because they're asking for more edge, your bid may still be profitable. But it's likely some combination of the two, and their price models all (or almost all) being lower than yours should cause you to update that the true value of the wheelbarrow is lower than you'd previously estimated.

Replies from: jmh↑ comment by jmh · 2024-03-15T16:36:28.047Z · LW(p) · GW(p)

Probably worth including that the winner's curse will also tend to be a feature when the object to be bought is a one time, one customer type setting.

Or would you agree that under your view, the market clearing price of a Walrasian auctioneer the price is also too high in some way? After all, it's pretty clear from the simple S & D graph that most of the buyers could have, in theory at least and likely in reality if they could directly communicate, bough whatever they bough at a price lower than the market clearing price; S slopes upwards and includes the producers required rate of return.

Replies from: bayesshammai↑ comment by Ricki Heicklen (bayesshammai) · 2024-03-26T23:20:53.289Z · LW(p) · GW(p)

Probably worth including that the winner's curse will also tend to be a feature when the object to be bought is a one time, one customer type setting.

I don't think the winner's curse is limited to this; e.g., I think if the top five bidders win in an auction for vacation tickets (not knowing the value of the vacation package in advance), the effect still exists. It also doesn't need to be a one time thing, or a unique good.

Or would you agree that under your view, the market clearing price of a Walrasian auctioneer the price is also too high in some way? After all, it's pretty clear from the simple S & D graph that most of the buyers could have, in theory at least and likely in reality if they could directly communicate, bough whatever they bough at a price lower than the market clearing price; S slopes upwards and includes the producers required rate of return.

I don't think the clearing price in such an auction is skewed high (if it were, you could profit in expectation by consistently selling, and this should correct the effect). I do think adverse selection concerns should enter your calculation even when submitting orders to two sided auctions like this one (e.g. any US stock market opening/closing auction), because your orders are still getting filled by the market as a whole, but I agree the dynamic does not have the directional bias of the auction I describe here.

↑ comment by Alok Singh (OldManNick) · 2024-03-14T23:53:52.138Z · LW(p) · GW(p)

I think there’s an implicit element of scale or one offness. For buying milk you have multiple samples as to good price. Even if any is contrived, the bulk still capture something real

Replies from: gwern↑ comment by gwern · 2024-03-14T23:57:06.421Z · LW(p) · GW(p)

For buying milk you have multiple samples as to good price. Even if any is contrived, the bulk still capture something real

No, the bulk don't, because I buy milk a lot more often than I go on Wall Street and try to get cute with limit orders or manufacturing options or straddles on speculative merger/takeover targets or sign up to MoviePass or park while ignorant in NYC. The bulk of my life is buying milk, not speculating on Widgets Inc. And if I did those enough times to come anywhere near the number of times I've bought milk, so that 'the bulk' could potentially be any of those things, I would also not be doing it nearly as badly as OP postulates I would. (Because I would be, say, a market-maker like Jane Street, which makes a lot of money off doing that sort of thing.)

Replies from: bayesshammai↑ comment by Ricki Heicklen (bayesshammai) · 2024-03-15T10:06:28.943Z · LW(p) · GW(p)

... I would also not be doing it nearly as badly as OP postulates I would. (Because I would be, say, a market-maker like Jane Street, which makes a lot of money off doing that sort of thing.)

I'm not sure I follow. Is the argument here that Jane Street is good enough at market-making that they are not vulnerable to adverse selection? i.e. that the dynamic in example #11 (Widgets stock) wouldn't apply to them?

comment by TeaTieAndHat (Augustin Portier) · 2024-03-15T16:34:33.960Z · LW(p) · GW(p)

Not sure this was the right structure for this post? The point you’re trying to make ("If someone’s trading with you and you can’t think why it would be in their interest to do that, it’s probably not a good trade for you"?) is interesting, and it’s the kind of argument where examples are welcome, but in this case, there’s something with giving just examples and no explanation of them that doesn’t quite work, and allows us to misunderstand the point/not pinpoint exactly what’s being said?

Replies from: nathan-helm-burger↑ comment by Nathan Helm-Burger (nathan-helm-burger) · 2024-03-15T17:29:53.933Z · LW(p) · GW(p)

Yes, thank you! I totally agree and was looking for others that did also. I think this post is confusing several different sorts of failures due to inadequate-information-leading-to-poor-trades. I think the most valuable point is that win-win trades (where you can see what both parties stand to gain) are inherently more trustworthy than win-lose trades which seem 'too good to be true' and you can't identify what the other party gains. In such situations you need to be really confident you have a strong information advantage in order to believe you are actually getting an implausibly good deal which disadvantages the other party.

Also I say the same here: https://www.lesswrong.com/posts/vyAZyYh3qsqcJwwPn/conditional-on-getting-to-trade-your-trade-might-not-have?commentId=bA34GydjFBaXs9rZa [LW(p) · GW(p)]

comment by Proph3t (metaproph3t) · 2024-04-10T12:31:33.843Z · LW(p) · GW(p)

If too much people pay attention to adverse selection, I'd argue that there's an opposite effect: advantageous selection.

Imagine a world where every venture capitalist only invests in 'hot' rounds. Like this post advocates, they become wary when they're easily able to trade their cash for a company's equity. In this world, the market is inefficient. Supposing you have the cash to keep your portfolio companies alive (e.g., you're SoftBank), you'd be much better off only investing in the companies that other investors don't want to touch. This is because even though the hot startups are on average better startups (because of adverse selection), the low prices you pay for the not-hot startups should more than make up for it. Warren Buffet famously recommends "to be fearful when others are greedy and to be greedy only when others are fearful." And it's a rule of markets that in order to make outsized returns, you need to be both right and contrarian.

The rule I apply is considering the quality of the average market participant's information. Back to your Alice's Restaurant vs. Bob's Burgers example, it'd matter a lot whether the typical eater is a local or a tourist. If it looks like most eaters are locals, they likely have very good information on both places: almost all of them have likely tried both multiple times. But if they're all tourists, people may have just gone to the restaurant because they saw others there. In effect, there's a speculative bubble in Alice's food. So you're probably better going off the beaten path: although Bob's burgers is ceteris paribus of lower quality, the extra benefits (e.g., better service, chef can pay attention to crafting you an excellent burger) will ceteris paribus make up for it!

comment by jefftk (jkaufman) · 2024-03-17T11:21:48.564Z · LW(p) · GW(p)

A common experience in parenting is that a little kid will strongly prefer to play with toys that other kids are playing with, even when there are lots of others sitting around totally available. Conditional on another kid having chosen this toy out of all the options it's probably a better toy!

comment by habryka (habryka4) · 2024-04-09T20:56:02.698Z · LW(p) · GW(p)

Promoted to curated: Adverse selections seems like a really useful lens to throw at lots of different things in the world, and I can't currently think of another post on the internet that gets the concept across as well as this one.

I generally really like starting of a sequence like this using lots of concrete examples, instead of abstract definitions.

I do think there is something tricky about adverse selection in that it is the kind of thing that does often invite a kind of magical thinking or serve as a semantic stopsign [LW · GW] for people trying to analyze a situation. People modeling you, or people modeling groups that you are part of, results in tricky and loopy situations, and I've often seen people arrive at confident wrong conclusions based on analysis in this space (though this post, mostly as a list of examples doesn't fall into that error mode, but I find myself curious how future posts in the sequence might handle those cases).

comment by Jonas Hallgren · 2024-03-15T07:30:11.484Z · LW(p) · GW(p)

Alright, quite a ba(y)sed point there, very nice. My lazy ass is looking for a heuristic here. It seems like the more the EMH is true in a situation/amount of optimisation pressure applied the more you should expect to be disappointed with a trade.

But what is a good heuristic for how much worse it will be? Maybe one just has to think about the counterfactual option each time?

Replies from: bayesshammai↑ comment by Ricki Heicklen (bayesshammai) · 2024-03-15T10:13:22.740Z · LW(p) · GW(p)

It seems like the more the EMH is true in a situation/amount of optimisation pressure applied the more you should expect to be disappointed with a trade.

Yes, this is exactly right—post #2 in the sequence is about what environmental factors increase or decrease the prevalence of adverse selection, and ways to improve trading (and everyday decision making) in light of it. Stay tuned :)

comment by Saul Munn (saul-munn) · 2024-03-17T16:11:39.288Z · LW(p) · GW(p)

I really enjoyed this — thank you for writing. I also think the updated version is a lot better than the previous version, and I appreciate the work you put in to update it. I'm really, really looking forward to the other posts in this sequence.

I'd also really enjoy a post that's on this exact topic, but one that I'd feel comfortable sending to my mom or something, cf "Broad adverse selection (for poets)."

comment by Shankar Sivarajan (shankar-sivarajan) · 2024-03-15T17:59:38.612Z · LW(p) · GW(p)

More aphoristically: "Never give a sucker an even break."

comment by Shankar Sivarajan (shankar-sivarajan) · 2024-03-15T17:52:43.481Z · LW(p) · GW(p)

Re 5 and 6, that's why most normal purchases aren't conducted via auctions: if there's little variability in the product, it's not rare or hard to find, and it's been sold enough that the information asymmetry is negligible, just stick a price tag on it.

comment by aphyer · 2024-03-15T13:48:59.274Z · LW(p) · GW(p)

I did not understand #8 at all. I am confident that this is not because I don't understand the general point. Does anyone have an explanation of #8?

Replies from: thomas-kwa, nathan-helm-burger↑ comment by Thomas Kwa (thomas-kwa) · 2024-03-15T17:49:15.897Z · LW(p) · GW(p)

I think habryka's explanation [LW(p) · GW(p)] of this post's idea of adverse selection is basically correct:

I think all of them follow a pattern of "there is a naive baseline expectation where you treat other people's maps as a blackbox that suggest a deal is good, and a more sophisticated expectation that involves modeling the details of other people's maps that suggests its bad"

In example #8, you naively think that a market order will clear at slightly more than the going rate for a field, which it will in a normal competitive market. But in this case, you let your counterparty decide the price, and they're incentivized to make it maximally bad for you.

My guess is that some later post in the sequence will argue why this broad definition of adverse selection makes sense.

↑ comment by Nathan Helm-Burger (nathan-helm-burger) · 2024-03-15T17:31:44.988Z · LW(p) · GW(p)

Yeah, my explanation is that the author is confused and has put together a set of examples which don't cleave reality at the joints. Thus, many of the examples just don't hang together as making the same point.

See TeaTieAndHat's comment here, and my response: https://www.lesswrong.com/posts/vyAZyYh3qsqcJwwPn/conditional-on-getting-to-trade-your-trade-might-not-have?commentId=pfiZEQ8GmdRJje4x3 [LW(p) · GW(p)]

comment by quiet_NaN · 2024-04-10T03:49:19.527Z · LW(p) · GW(p)

Not everyone is out to get you [LW · GW].

If your BATNA to winning the bid on that wheelbarrow auction is to order it for 120$ of Amazon with free overnight shipping, then winning the auction for 180$ is net negative for you.

But if your BATNA is to carry bags of sand on your back all summer, then 180$ for a wheelbarrow is a bloody bargain.

Assuming a toy model where dating preferences follow a global preference ordering ('hotness'), then any person showing any interest in dating you is proof that you can likely do better.[1] But if you follow that rule, you can practically never date anyone (because you are only sampling the field of partners), which leaves a lot of utility on the table because relationships can be net positive for all participants even if they do not precisely match their market values.

If you want to buy stock to make money from speculation then you need to worry that almost everyone you trade with is better informed than you and you will end up net negative. On the other hand, if you buy stock as a long term investment (tracking some index or whatever) then you probably care a lot less about overpaying one percent.

I think that Zvi mentions a few legitimate examples of things which are out to get you, and their advice to avoid ones with unlimited cost potential is certainly sound.

If I buy toilet paper in the supermarket, I am paying more than the market price. If I wanted, I could figure out what toilet paper costs in bulk, find a supplier and buy a lifetime supply of toilet paper, likely saving a few 100$ in the process. I am not doing this because these amounts of savings over a lifetime are just not worth the hassle. Instead, I trust that competition between discounters mean that their markup is less than an order of magnitude and cheerfully pay their price.

- ^

Don't ask me if that is part of the reason why flirting is about avoiding the creation of common knowledge. I am just some nerd, why would I know?

comment by Review Bot · 2024-03-16T20:48:22.103Z · LW(p) · GW(p)

The LessWrong Review [? · GW] runs every year to select the posts that have most stood the test of time. This post is not yet eligible for review, but will be at the end of 2025. The top fifty or so posts are featured prominently on the site throughout the year.

Hopefully, the review is better than karma at judging enduring value. If we have accurate prediction markets on the review results, maybe we can have better incentives on LessWrong today. Will this post make the top fifty?

comment by [deleted] · 2024-03-16T00:21:49.753Z · LW(p) · GW(p)

These examples all seem like efficient market or winners' curse examples, not varieties of adverse selection, and in equilibrium, we shouldn't see any inefficiency in the examples.

Adverse selection is such a large problem because a seller (or buyer) can't update to know what type they're facing (e.g a restaurant that sells good food vs bad food) and so offers a price that only one a subset of types would take, meaning there's a subset of the market that gets doesn't get served despite mutually beneficial transactions being possible.

In all of these examples, it's possible to update from the signal - e.g. the empty parking spot, the restaurant with the short line - and adjust what you're willing to pay for the goods.

I think these examples make the important point that one should indeed update on signals, but this is different to adverse selection because there's a signal to update on, whereas in adverse selection cases you aren't getting separating equilibria unless some types drop out of the market.

comment by TsviBT · 2024-03-15T00:32:13.289Z · LW(p) · GW(p)

Bruh. Banana Laffy Taffy is the best. Happy to trade away non-banana to receive banana, 1:1.

Replies from: gwern↑ comment by gwern · 2024-03-15T00:36:48.274Z · LW(p) · GW(p)

Personally, I hate Banana Laffy Taffy (it has that awful chemical Cavendish taste), but since you're voluntarily offering to trade me for mine, you must be offering me a bad deal! I wonder what TsviBT knows that I don't know?! I can't risk accepting any Laffy Taffy deal below 2:1.

Replies from: CronoDAS, quiet_NaN↑ comment by CronoDAS · 2024-03-15T05:41:38.679Z · LW(p) · GW(p)

(yes I know you've being ironic)

Well, trade does have a more zero-sum character when both sides of the trade have the same preferences, but if you can credibly claim to have different preferences, you're also in a better position to convince the person on the other side of the trade that you're not trying to offer them a bad deal. (For example, if you're selling stock because you want to spend the money, you don't care if you disagree with someone about what the stock will be worth in the future; you just want to sell it for the best offer you can get right now.)

Replies from: Seth Herd↑ comment by Seth Herd · 2024-03-17T19:57:07.918Z · LW(p) · GW(p)

You don't need to have different preferences to make mutually beneficial trades. Human preferences tend to be roughly unbounded but sublinear - more of the same good isn't as important to us. So if I have a lot of money and you have a lot of ripe oranges, we can both benefit greatly by trading even if we both have the same love of oranges and money.

Replies from: CronoDAS↑ comment by quiet_NaN · 2024-04-10T04:12:12.703Z · LW(p) · GW(p)

(sorry for thread necromancy)

Meta: I kind of wonder about the moderation score of gwern's comment. Karma -5, Agreement -10. So someone saw that comment at -4 and thought 'this is still rated too high'.

FWIW, I do not think his comment was bad. A bit tongue in cheek, perhaps, but I think his comment engages with the subject matter of the post more deeply than the parent comment.

Or some subset of people voting on LW either really like Banana Taffy or really hate gwern, or both.

comment by Alok Singh (OldManNick) · 2024-03-14T23:52:29.902Z · LW(p) · GW(p)

reminded me of https://en.wikipedia.org/wiki/Winner%27s_curse

lol laffy taffy is too real banana sucks

comment by rain8dome9 · 2024-04-10T20:31:35.296Z · LW(p) · GW(p)

Relevant quote from Dragonfired by J. Zachary Pike. "Brokers make money by knowing key information; they make fortunes by ensuring that other brokers remain unaware or unsure of the same information until after critical trades."

comment by Dzoldzaya · 2024-04-10T20:00:06.221Z · LW(p) · GW(p)

MoviePass users are selected for seeing a lot of movies. If MoviePass makes a business plan that models users as average people, it will lose a lot of money. Conditional on someone wanting to buy MoviePass, MoviePass probably should not want them as a customer.

I'm going to nitpick here and note that the marginal cost to the cinema of allowing in an extra customer is often close to zero, seeing as most films don't sell out. It may even be positive, if they spend money on popcorn and drinks, and invite their friends who don't have a pass. It seems from that article that the failure in the business model was partly that MoviePass was just badly managed, partly that people were abusing the system in various ways by scalping/ selling tickets/ getting hundreds of people using the same service. I checked my local cinema chain and they started running an 'Unlimited' service over a decade ago, and it's still in use, so I think it remains a valid model.

Correction: I understand the MoviePass model now and the adverse selection argument makes more sense. Cinemas with a subscription model can work even with a high proportion of power users, but that's because the externalities (popcorn, drinks, inviting friends) accrue to the cinema.

↑ comment by Jalex S (jalex-stark-1) · 2024-04-13T16:07:13.004Z · LW(p) · GW(p)

MoviePass was paying full price for every ticket.

Replies from: Dzoldzayacomment by clone of saturn · 2024-03-15T01:35:44.909Z · LW(p) · GW(p)

I use eBay somewhat regularly, and I've found that most of the time I get what I expected at a reasonable price. So I find the theory that I should always regret participation in any auction somewhat dubious.

comment by Shankar Sivarajan (shankar-sivarajan) · 2024-03-15T17:37:56.102Z · LW(p) · GW(p)

(3) seems meaningfully different from your other examples. That's a case where they're the same to you, and one is better to Bob, so it's good that he gets the one he prefers: that's just standard envy-free division. If you make a mistake with the information you have, that's on you; there's nothing wrong with the setup.